Is Vanguard 500 Index Fund Still Worth Owning?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

The case for building your portfolio around low-cost, passively run funds is irrefutable now, but when the first index mutual fund for individual investors launched 40 years ago, the notion was blasphemous. In fact, Vanguard 500 attracted so little money initially that it wasn't even able to purchase all 500 stocks in the Standard & Poor's index. Fast-forward four decades: Investors have more than $4.7 trillion riding on index mutual and exchange-traded funds. But with hundreds of other index options now available, is the granddaddy still better than all its progeny?

The Ultimate Disrupter

Long before ETFs, Vanguard 500 made the case for index investing

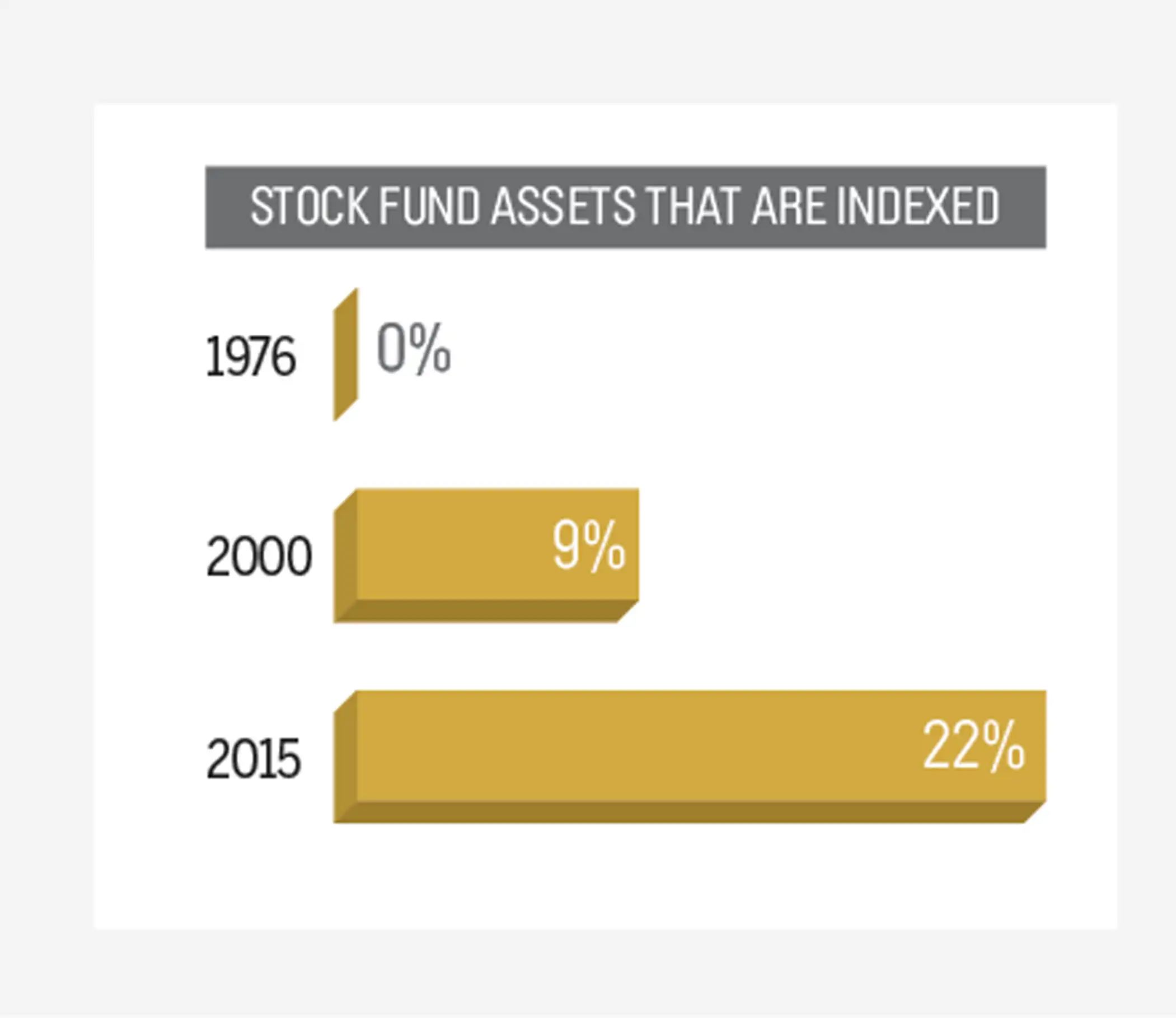

Until August 1976, fund investors had no choice but to go with actively managed portfolios, often paying commissions of 8.5%. But with the launch of this groundbreaking fund, Vanguard founder Jack Bogle "gave us an entirely new philosophy," says Rick Ferri, founder of Portfolio Solutions. And a profitable one. If you invested $10,000 from the get-go, you would have nearly $600,000, almost $100,000 more than in a typical blue-chip fund. Not bad for a fund initially ridiculed for just trying to match the market, not beat it.

Even in the difficult past decade, Vanguard 500 proved its mettle. Its 7.1% annual return outpaced 78% of large-stock funds. No wonder $438 billion is invested in Vanguard funds that track the S&P 500 index.

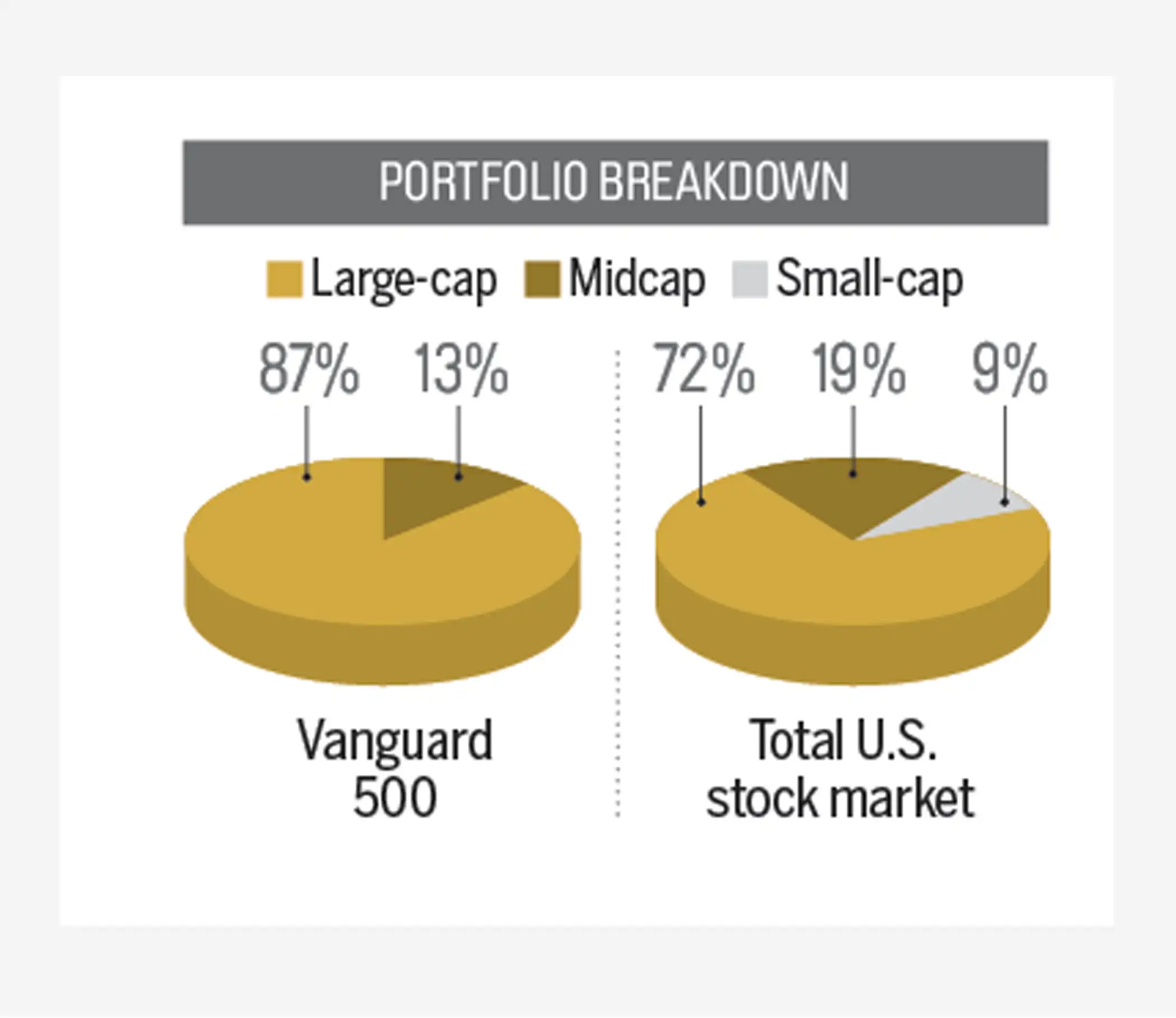

A Small Problem

Though the fund mirrors the broad market, it's missing smaller stocks

There's no arguing Vanguard 500's merits—Warren Buffett name-checked it for where he wants most of his fortune invested after he dies. But there are now broader index funds that track the total U.S. market, including small-company shares. "That you can buy an extra 3,000 stocks, for the same cost, makes diversification sense," says Ferri.

Planner Allan Roth, founder of Wealth Logic, also prefers total market funds, but he notes the choice may not be yours. Research firm BrightScope says 8,750 401(k)s offer Vanguard 500, vs. 2,100 teeing up Vanguard Total Stock Market Index.

Don't worry. You can supplement 500 using Vanguard Extended Market Index or a small-stock fund in your IRA or taxable account, Roth says.

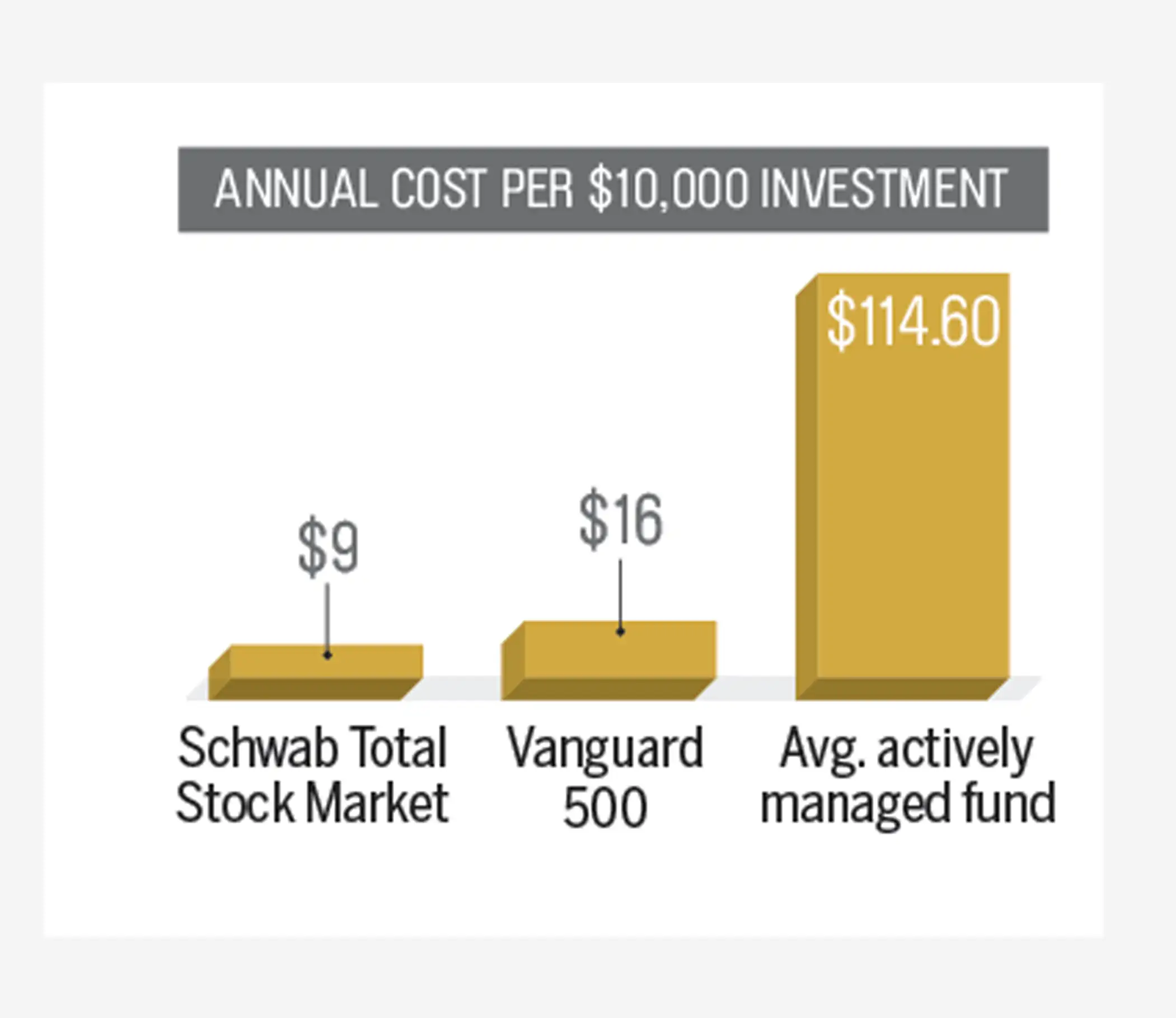

Penny-Wise

The fund is no longer the cheapest, but switching may not be worth it.

In an environment where returns are expected to be modest, pinching pennies makes sense—within reason. Vanguard 500's basic shares charge a low 0.16%. Yet there are cheaper options, including the ETF version of Vanguard Total Stock Market (0.05%) and Schwab Total Market (0.09%).

With new money, keep things simple by focusing on the lowest-cost broad market index option at your fund firm or brokerage, says Ben Johnson, Morningstar's director of global ETF research. But if you've owned Vanguard 500 for years in a taxable account, hang on. Triggering capital gains taxes on the better-than-average growth you've enjoyed in this fund is hardly worth the few bucks a year you would save in investment management fees.