4 Rules for Shacking Up in Retirement

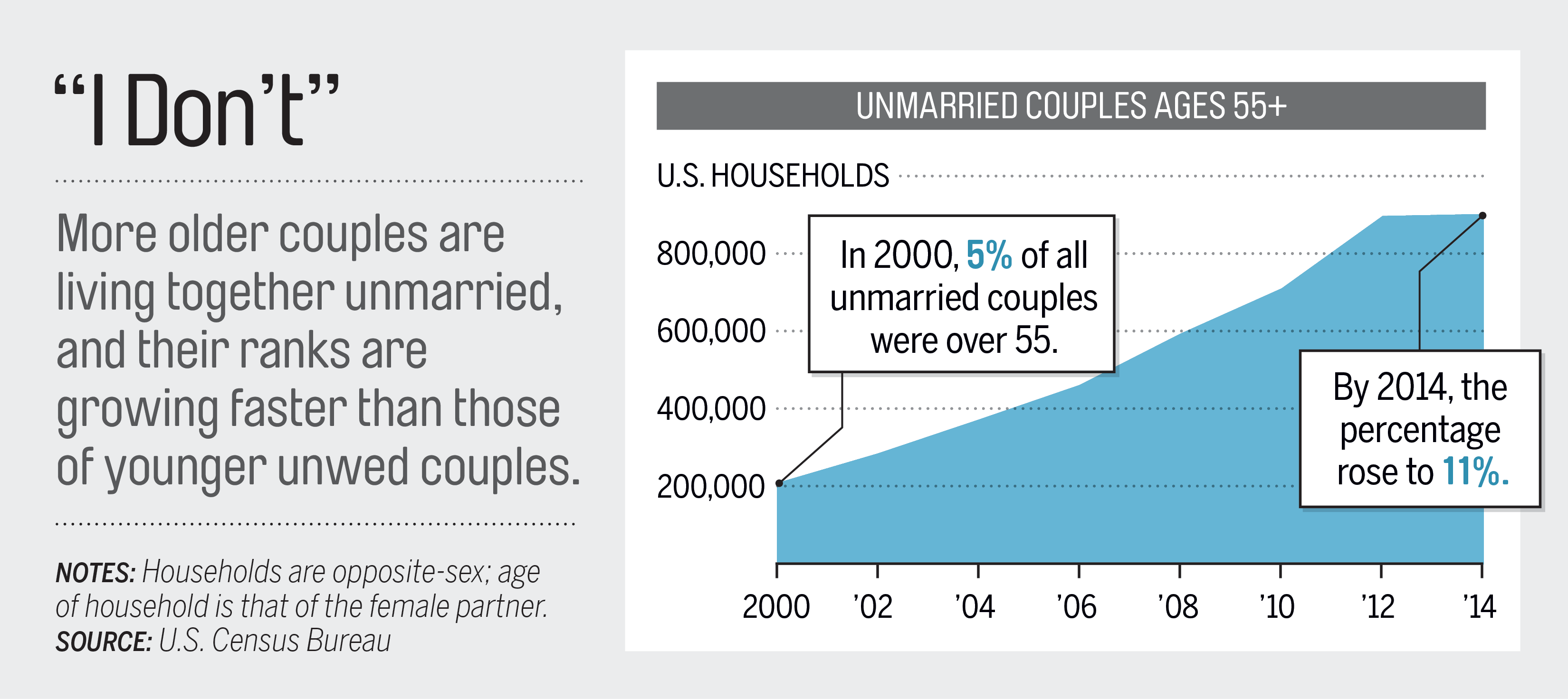

You're never too old to shack up. A growing number of grownup lovebirds are living together without benefit of marriage. In 2014, for example, 900,000 women ages 55 and over cohabited with a male partner, reports the Census Bureau, up from 372,000 10 years earlier. There are plenty of reasons to move in with, but not marry, your new partner, such as keeping Social Security benefits based on an earlier marriage, making sure your kids and grandkids remain your sole heirs, and just not wanting to tie yourself down.

But while staying single may simplify matters in some respects, living together in retirement can get complicated too, since each of you brings a family and a lifetime's worth of assets into the mix. When the refrigerator gives out, who buys the new one? If you get sick, who directs your care? Follow these tips to make your love shack a happy one.

Share the wealth...a little

Without a marriage, your finances won't officially merge. But you will have shared costs. Simplify daily spending by opening a joint account for regular, known expenses. And set up another account, suggests Minnesota planner Timothy LaPean, for unforeseen expenses—everything from that broken fridge to impulse-purchase $300 tickets to Paris. Keep most of your money separate, though, to protect it for yourself and your heirs, should you break up.

While splitting expenses with a partner may have been simple at age 22—it's easy when you're both broke—you and your current sweetheart may have vastly different finances. So will you vacation in Venice, Italy, or Venice, Fla.? Dine on filet mignon or grill hot dogs?

To guide how well you'll live and what each of you will contribute, ask yourselves this, says P. Jeffrey Christakos, a planner in Westfield, N.J.: Are you roommates or are you life partners? As roomies, you might live in a style the less well-off partner can afford, splitting shared expenses evenly and letting the wealthier partner spring for the occasional treat. If you're life partners, settle on a different split—say, 70/30—for joint expenses.

Set down roots

Moving into a house your new love owns can be great—until your sweetie dies and his or her kids show up to kick you out. Avoid this with what's known as a life estate, a legal document giving the non-owning partner the right to live in the home for the rest of his or her life, with the property ultimately going to the owner's heirs. Having an attorney draw one up will cost anywhere from a few hundred dollars to a few thousand, if part of a larger estate plan.

- Calculator: How will retirement impact my living expenses?

Buying a place? Title the property as tenants in common if you plan to leave your share to your children, or as joint tenants with right of survivorship to have your partner inherit your half.

Make a health care plan

While spouses can make medical decisions on each other's behalf, you have no such automatic right. So decide who's in charge of your health care: One another? Your kids? Fill out a health care power of attorney and a durable power of attorney so your designees can handle your affairs if you can't.

You may not be up for the financial and physical demands of caretaking, especially if you have already looked after a dying spouse. Decide how you will cover expenses and pay for extended care, and whether you need long-term-care insurance. Because you're not married, if one of you has to go on Medicaid, the other's assets don't have to go toward health care, though jointly owned property does.

Make the heirs apparent

Absent other plans, your spouse, if you were married, would be your primary heir. Not so for unwed couples. You may want to leave most of your estate to your children or other relatives. But you might also want to ensure that your beloved has resources to last the rest of his or her life. To do that, work with an estate-planning lawyer to create what's called a residual trust. "You can provide income for a surviving partner but keep your children or other heirs as your final beneficiaries," explains Mark Struthers, a financial planner in Chanhassen, Minn.

Disclose the outlines of your plan to your partner and your family, because surprises after your death will be upsetting, says New York City financial planner Karen Altfest: "It's enough to have grief without being angry too."