The Trouble With Taking a Lump Sum Pension Payout

- Congress Wants to Make Your 401(k) More Like a Pension. Here's the Problem With That

- The Scary Truth Behind That E*Trade Super Bowl Retirement Commercial

- Meet Richard Thaler, the Man Who Just Won the Nobel Prize for Helping You Save for Retirement

- There Are Now More Crypto Coins Than U.S Stocks

- The Best Time to Buy Bitcoin, Explained in One Chart

Congratulations! You're one of the shrinking number of Americans who have earned the right to a pension—guaranteed income for life for you and maybe for your spouse as well. Just make sure you don't give it up too easily.

That's a real risk. Up to half of companies with pension plans, say experts, give workers the option of taking their pension as a lump sum. On top of that, 47% of corporate plans, including those from Boeing and Hewlett-Packard, either have just made or will soon make pension buyout offers to vested former employees, benefits firm Aon Hewitt reported earlier this year. Driving those offers are IRS rules expected to make buyouts less favorable for employers within a year or so.

Lump-sum checks, often in the hundreds of thousands of dollars, are tempting. Fifty-eight percent of employees take buyouts, and the share taking the lump-sum option at retirement is likely higher, says Aon Hewitt consultant Ari Jacobs.

Pension industry experts and consumer advocates, however, say that for most workers the traditional pension is a better deal. So before you decide, think this over:

When to Take Steady Payments

If you or your spouse is in good health and has a family history of longevity, lean toward taking the monthly pension. The advantages: The money lasts for life. If you make it to age 90—and 28% of 65-year-olds do—you'll still be getting that check. And, in exchange for smaller benefits, your spouse can continue to receive half or often all of those monthly payments after your death. So if you're a man and your wife survives you—on average, she will—she'll get cash for life too. One downside: Unlike Social Security, most private pensions don't adjust for inflation, so your purchasing power will diminish over time.

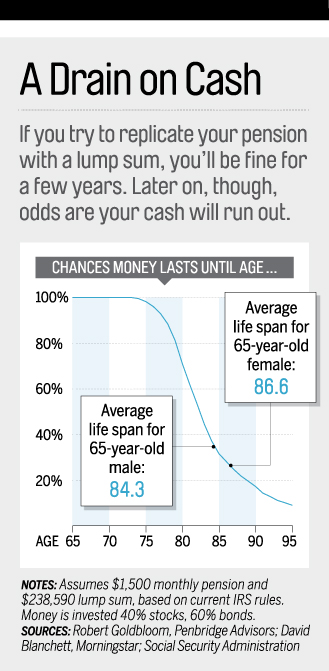

Now, you could invest the lump sum (set by a complex IRS formula) and use it to fund a monthly stipend. But even if you're the next Warren Buffett, you'd likely get less each month than you would from a pension. Say you're due $1,500 a month, or $1,295 if you opt for a 100% survivor's benefit. If you took the roughly $240,000 you'd receive instead and sought to have it last a 65-year-old's average life span of about 20 years (see chart), you'd pay yourself only $1,213, calculates David Blanchett, Morningstar's director of retirement research. And this strategy would have only an 80% chance of success. To be safe, you'd have to cut your allowance to $1,000 a month—or $855 to last until you're 90.

Why is the lump-sum income so low? Flying solo, you have to make sure your money lasts a full 20 or 25 years. But in a group plan, a lot of people will live shorter lives, so less money has to be reserved for them. The result is more generous monthly payouts for everyone, says Robert Goldbloom, a principal at pension consultant Penbridge Advisors. "People who don't live as long subsidize those who live longer," he says. That makes pensions a particularly good deal for women, given that they generally live longer than men.

When to Take the Lump Sum

If you're in poor health and don't have to provide for a spouse, the math favors the lump sum. Given a life expectancy of a decade or less, you'd have more than enough to duplicate a pension. In the above example, you could pay yourself $1,500 a month over 10 years, not invest a dime, and still have $60,000 left over.

A lump sum also makes sense if you have no cash in the bank or investments you can tap for emergencies. You could keep part of that money in the bank for urgent needs, and live off the rest.

Should you be lucky enough to live comfortably off other sources of income, you could take the money and invest it aggressively to maximize a possible inheritance for your beneficiaries.

Finally, take into account your pension plan's health. Most private-sector plans with at least 26 workers are backstopped by the Pension Benefit Guaranty Corp.—up to about $5,000 a month for a single-employer plan, but far less for a multi-employer plan. Check on your plan's "funded status"—a measure of its assets and liabilities. If the number, which the plan has to report to you annually, is falling toward 80%, that's worrisome; you might take the bird in the hand if you'd lose much of your benefits from a failed plan.

In any case, your best bet is to roll the money into a traditional IRA; otherwise, you'll get a big tax bill. Smaller withdrawals from the IRA, on the other hand, will likely be taxed at a lower rate.