3 Ways the Stock Market Could Tank, According to Experts

- The Best Performing Stock of This Bull Market Is Up Almost 39,000% — and You've Probably Never Heard of It

- Worried About a Stock Market Crash? 5 Ways to Keep Your Money Safe

- This One Indicator Has Predicted Every Recession Since 1960—and It's Flashing a Warning

- 3 Easy Ways to Build a Killer Investment Portfolio

- 7 Investing Moves You Need to Make by December 31

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

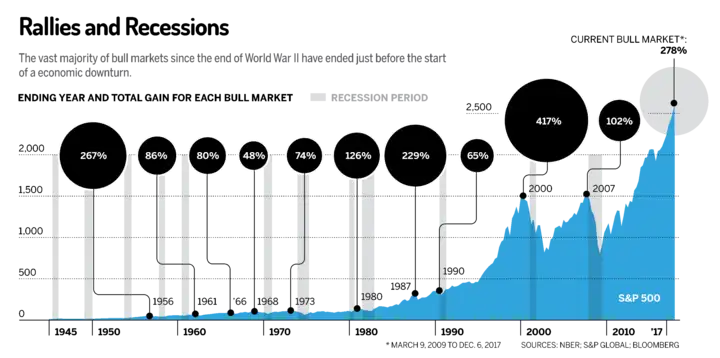

It’s said that bull markets don’t die of old age, which explains why this market keeps chugging along despite being more than twice as old as the average rally. But if that’s true, what do bull markets die of?

Up until a few years ago, many investors thought this bull would be gored by the same force that weighed on the global economy in the aftermath of the financial crisis: deflation. Deflation is that rare circumstance in which the economy can’t seem to gain any traction, and prices and sentiment keep slipping. “That’s the type of market you saw in the 1930s, when there was a total loss of confidence,” says James Stack, president of InvesTech Research and a market historian.

Today, however, investor confidence and the economy have healed sufficiently that market watchers are now expecting a different—and more predictable—denouement to history’s second-oldest rally.

“The economy has evolved into a more traditional expansion like the ones last seen at market tops in the 1960s and 1970s,” says Stack. And absent a major bubble forming in a large sector of the economy—like housing in 2007 or tech stocks in the late 1990s—conventional wisdom says this bull will end in one of these three predictable ways.

Scenario #1: The Economy Did It

“Bull markets don’t die of old age, they die of fright,” says Sam Stovall, chief investment strategist with the investment research firm CFRA and author of The Seven Rules of Wall Street. And what bull markets fear most isn’t the shock of war or political crisis, but recessions.

Two-thirds of all bull markets since World War II have ended in anticipation of an economic contraction. Still other downturns that didn’t precede official recessions, like the 1966 bear market, were at least triggered by the fear of a slowdown that came close.

If that’s the case, you might assume that Wall Street has little to worry about now, since most traditional indicators are signaling that the economy is doing just fine and isn’t likely to shrink in the next year or two.

Take housing starts. Historically, real estate construction has been a terrific indicator of the economy because it takes months to construct a new home. And homebuilders are reluctant to break ground if they fear the economy may slump several months down the road.

Every recession since 1960 was preceded by a double-digit decline in housing starts, according to Stovall. Yet in October housing starts rose by double digits—13.7%, to be exact—indicating that construction firms aren’t betting on a slowdown in the economy in 2018.

What’s more, “we’ve seen some of the best manufacturing numbers in recent months, and corporate profits are still climbing,” says John Lynch, chief investment strategist for LPL Financial. He notes that historically the economy tends to slip into recession two years after corporate earnings have peaked.

Why You Should (Still) Worry

While few economists are predicting a recession anytime soon, you have to remember that the stock market is a forward-looking indicator, meaning stock slides precede recessions or slowdowns—not the other way around.

And often it can take months after a selloff before the economy begins to slide. The average bear market, in fact, has typically begun 7½ months prior to the start of an official recession, according to CFRA.

Sometimes the lag time is even greater. The 2000–2002 bear market began a full year before the economy officially slid into a recession.

“By definition, bull markets peak when bullish optimism is very high,” says Stack. And in many cases it’s hard to know a recession is looming until it’s almost here.

There's another concern. “The economy typically slips into a recession four years after the first Federal Reserve rate hike,” says Lynch. (For the record, Lynch’s firm, LPL, does not believe a bear market is imminent and thinks stocks will rise 8% to 10% in 2018.)

However, because the Fed has been so slow to raise rates, people forget that the central bank actually started lifting rates in late 2015. Four years after that would put a possible recession start date in late 2019. And if stocks foreshadow recessions up to a year before, that means a bear could be lurking at the end of 2018.

How You Can Hedge Your Bets

Favor high-quality stocks.

Don’t assume the next downturn will automatically be a bear market—or a big bear such as the 2007–2009 meltdown or the 2000–2002 tech wreck, where more than half the market’s value was erased.

If the next downturn is a pullback (a 5% to 10% decline) or a correction (10% to 20% fall in prices), it may take only two to four months for stock prices to climb their way back, if history is any guide, Stovall says.

So rather than undoing your entire investment, focus on ways you can stay invested while protecting yourself a bit more.

High-quality stocks are a good place to look if you’re worried about the economy. “When the seas get rough, sailors prefer a better-made boat,” says Stovall. They particularly gravitate to shares of companies with little debt, healthy balance sheets, and strong competitive advantages that can withstand stormy economies.

Not only do high-quality shares hold up better in a downturn, they also tend to outperform in the latter stages of a bull market (speculative shares of lower-quality companies, by contrast, tend to thrive at the start of new bull markets).

On our Money 50 list of recommended exchange-traded funds, there’s the PowerShares S&P 500 High Quality ETF (SPHQ).

Another way to get at quality is to look for companies with a strong track record of being able to make and grow their dividend payments through thick and thin for more than a quarter-century, such as those shares found in the S&P Dividend Aristocrats Index, says Stovall.

You can gain exposure to those names through the SPDR S&P 500 Dividend ETF (SDY) on our Money 50 recommended list. An added bonus: This fund keeps more than a third of its assets in defensive sectors such as consumer staples, health care, and utilities, which don’t require a strong economy to thrive.

Scenario #2: The Fed Did It

“Bull markets don’t die of old age. Sometimes, they get murdered,” says Terri Spath, chief investment officer for Sierra Investment Management. “I hate to point the finger, but I think it will be the Fed.”

How is that likely to happen—given that inflation remains historically low and given that the Federal Reserve has been lifting rates at a snail’s pace over the past two years?

Simple: Central bankers at the Fed have publicly stated that they believe there will be around two or three more rate hikes in 2018, bringing the so-called Federal funds rate, which banks charge one another on overnight loans, to around 2% or so next year.

But as Floyd Tyler, president and chief investment officer of Preserver Partners, tells Money, a downturn might be spurred simply if the Fed becomes a bit more aggressive than expected—“maybe four or five rate hikes.”

Why You Should Worry

A policy misstep that triggers a bear would be nothing new. The markets have a knack for testing newly installed Fed chairmen.

It happened to Alan Greenspan, who became chairman in August 1987, at the end of an economic cycle. The Greenspan-led Fed proceeded to raise interest rates just before the October 1987 crash. Similarly, Ben Bernanke assumed the Fed chairmanship in 2006 toward the end of another economic cycle as the central bank was hiking rates—and just before the 2007–2009 bear market.

Fed governor Jerome Powell, who is President Drumpf’s nominee to replace Janet Yellen, would similarly be stepping into his role in the latter stages of a business cycle while the Fed is already raising rates.

Spath says the Fed doesn’t even have to make a big error—for instance, by raising rates too aggressively—to spook the markets. Simply raising rates unexpectedly or communicating their intentions poorly “could create volatility as rates rise.”

To be sure, many bulls argue that historically the Fed got into trouble only by raising short-term rates above 4%. Today the Federal funds rate is less than 2%. So the Fed has a long way to go to derail this market.

But Spath warns that it’s risky to assume that rates have to get all the way back to the levels at which they used to spook investors. “Inflation is lower and GDP growth is lower and yields are lower,” she says. So why couldn’t a lower-than-average Fed funds rate scare the market this time?

How You Can Hedge Your Bets

Favor ballast over bounce when it comes to your stocks. In a market that starts getting choppy, “it’s important to carry a portfolio that has ballast. So don’t ignore the more stodgy sectors, like consumer staples,” which aren’t sexy but offer diversification in difficult times, says Stack.

There’s another reason to focus on these so-called Steady Eddies. While shares of boring companies that get left behind in bull markets tend to fall less in down markets, they also do better over very long periods of time.

“In the past 20 years, you would have increased your compound annual growth rate from 7.4% up to 8.2% by switching to low-volatility stocks while at the same time reducing your portfolio’s annual volatility by 30%,” Stovall says.

For exposure to steady blue-chip U.S. stocks, look at the iShares Edge Min Vol USA ETF (USMV). For exposure to small-company stocks, consider the SPDR SSGA U.S. Small Cap Low Volatility Index ETF (SMLY). And for exposure to international equities, go with iShares Edge MSCI Min Vol EAFE ETF (EFAV).

Scenario #3: The Market Has a Wile E. Coyote Moment

Bull markets don’t die of old age. But sometimes “they act like a cartoon character who’s run off a cliff. Once they realize there’s nothing supporting them, they start to drop,” says Jack Ablin, chief investment officer for BMO Private Bank.

On Wall Street there’s a formal name for this phenomenon. It’s called a “Minsky moment,” named after the late economist Hyman Minsky, who studied boom-and-bust cycles in the financial markets and argued how unstable bull markets can be after a long run.

A Minsky moment was blamed in part for the global financial crisis, when investors took on ever more debt to make speculative investments in houses and mortgage securities without worry until it eventually reached a tipping point when every investor did start to worry.

The bulls would argue that there’s little chance of a similar Minsky moment today because this economy lacks the level of imbalances and excesses witnessed during the financial crisis years. But before you grow too confident, be careful.

Why You Should Worry

The economy is by no means in a mania like the housing craze in 2007 or the dotcom craze in 1999, but there are plenty of economic imbalances.

For instance, American consumers have $1.021 trillion in revolving debt (such as credit card balances) outstanding, which is the most ever. This beats the previous record of $1.02 trillion set in April 2008, at the height of the mortgage meltdown.

American investors have also taken out a record $550 billion in “margin debt” to juice their stock market portfolios. The use of borrowed money to buy stocks is nothing new. But history shows that when investors get hopped up on debt to buy stocks, that’s usually a sign of a market top.

In 2000, for instance, margin debt as a percentage of GDP was 2.8%, a record then. Today, that ratio has risen to 2.99%.

A Minsky moment, though, needs another factor to get investors to notice that there’s nothing supporting the rally. And that realization could be anything from rising fear brought about by a geopolitical event or the bursting of an unrelated bubble elsewhere in the economy. Does Bitcoin come to mind?

How You Can Hedge Your Bets

Make sure your foundation is strong. In a full-blown Minsky moment, the bottom tends to fall out from under the market. That means minor tweaks around the edges of your portfolio may not be enough to offer you much protection.

“Investors need to make sure their asset allocation is set appropriately, not just for the next five to six quarters but for the next five to six years,” says Ablin.

He points out that “in the last four or five years, stocks have become the new bonds.” Ablin is referring to the fact that investors have grown so comfortable with the stock market lately that they’ve been swapping out their staid, low-yielding bonds with faster-growing and higher-yielding stocks.

But if you want to prepare for a possible turn in the market, you have to reassess those moves—and get around to rebalancing your portfolio back to a more conservative mix.

If you started out with a moderate 60% stock/40% bond portfolio five years ago and failed to rebalance since then, you’d now have a much more aggressive 75% stock/25% bond portfolio. Plus, the bull market is more vulnerable now to a Minsky moment than it was half a decade ago.

To be sure, Rob Arnott, chairman of Research Affiliates, notes that “the temptation in a bull market is to buy more."

But toward the end of a bull, less is more.