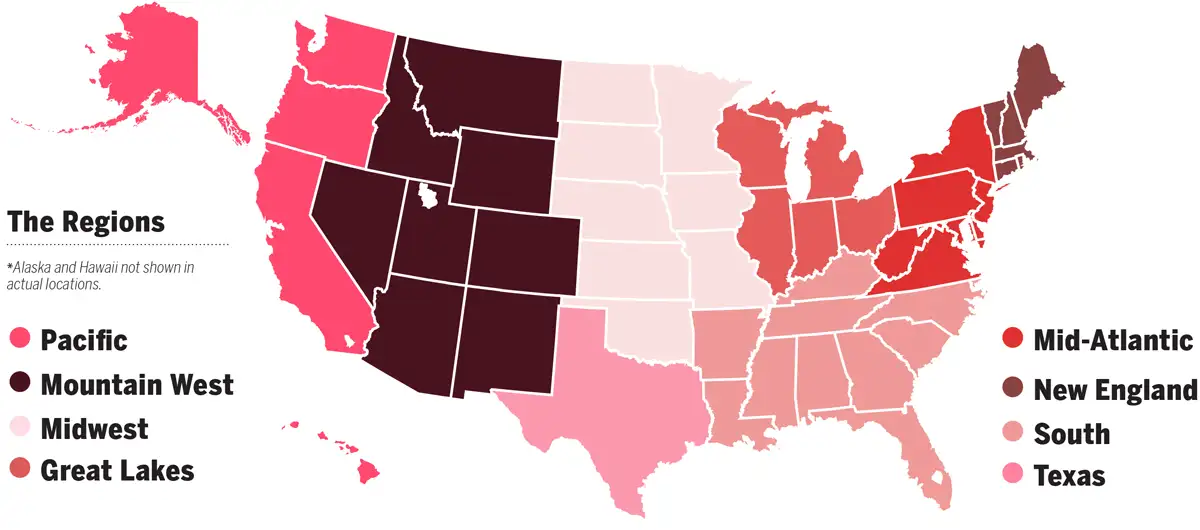

This Is the Best Bank in Every U.S. Region Right Now

As the Internet has changed so many of our daily tasks, so too has it altered the way we bank.

Americans are busier, clock longer hours, and work remotely more than ever before, and the ways we access our cash have evolved with our lifestyles. Although traditional aspects like customer service and branch locations still matter, bank customers today demand optimal online and mobile experiences too, says Rob Rubin, director at bank consultancy firm Novantas and creator of account shopping website FindABetterBank.com.

"Convenience is always the leading driver," he says. "People care about digital features like mobile banking, mobile check deposit, and peer-to-peer transactions."

Our research confirms this: 68% of Americans rated online banking as "very important" in a recent survey conducted for Money by market research firm Morning Consult. That's a larger share than for 20 other services or features, behind only customer service and fraud protection.

To find the banks that are mixing modern-day convenience with quality products, Money analyzed accounts at more than 175 financial institutions for our annual ranking. We've named winners by region and by type of bank—online, credit union, and big bank—as well as highlighting individual accounts. For the regional category, we focused on free checking and savings accounts, with competitive ATM fees. We also sought above-average customer service, based on J.D. Power's 2018 ratings.

Of course, we know few people are jumping at the prospect of switching banks. Rubin of Novantas says fewer people than ever are doing so: 7% of households with checking accounts will switch banks this year, down from about 14% in 2010. Digital benefits mean it's no longer necessary to change banks even after a long-distance move, and those same digital connections can make it a pain to break up with your bank.

In fact, visitors to FindABetterBank.com report negative experiences as the most common reason for switching banks, Rubin says. And more than half of you told Morning Consult that you're currently pleased with your bank.

Yet it can pay—literally—to be more proactive. Banks are reintroducing free checking accounts, but other fees are ticking up. On the plus side, interest rates on savings accounts are rising for the first time in a decade, says Brian Karimzad, founder of MagnifyMoney, a financial product comparison website.

"It's really changed the equation in terms of where you want to park your money," Karimzad says.

Read on to find the accounts with which you can dodge fees, grow your savings, and bank with digital ease.

Banner Bank

Why it wins: Banner offers multiple checking accounts that have low, easy-to-waive monthly fees or are free altogether. The bank doesn't charge fees for withdrawing from an out-of-network ATM and even offers unlimited refunds on the fees charged by ATM owners—a rarity among traditional banks. Banner is also J.D. Power's top-rated bank for customer service in the Northwest region.

Caveat: There's little not to like, especially after Banner raised the interest rate on its basic savings account to 0.1%. Yet the savings account does require a $100 minimum balance to waive a small monthly fee.

Where you can find it: Calif., Idaho, Ore., Wash.

Key account: Connected Checking

Monthly service fee: $0

Outside ATM fee: $0

Washington Federal

Why it wins: Washington Federal offers a checking account with no monthly or ATM fees. And you can avoid surcharges from ATM owners by sticking with one of 32,000 ATMs in the MoneyPass network the bank participates in. Washington Federal's overdraft fee is below average, at $25, and interest on its savings account is above average, at 0.1%.

Caveat: Depending on which state you live in, the bank's 236 branches may not be convenient.

Where you can find it: Ariz., Idaho, Nev., N.M., Ore., Texas, Utah, Wash.

Key account: Basic Checking

Monthly service fee: $0

Outside ATM fee: $0

Finalist: If you live in Montana, Wyoming, or Colorado, check out Glacier Bank. Its Easy Interest checking account is free and pays 0.01% interest.

First National Bank of Omaha

Why it wins: With no minimum deposit required and no monthly fees, First National Bank of Omaha is an easy pick. It also offers free out-of-network ATM transactions and a robust national network of ATMs (so you can avoid ATM surcharges). And the bank is a regional winner in J.D. Power's 2018 customer service ratings. One other perk: First National offers a refund of one overdraft fee every 12 months.

Caveat: You may be a long drive from any of the bank's roughly 100 branches.

Where you can find it: Colo., Ill., Iowa, Kans., Neb., S.D., Texas

Key account: First National Checking

Monthly service fee: $0

Outside ATM fee: $0

Huntington

Why it wins: Huntington is a perennial top performer in J.D. Power's customer service surveys. The basic checking account is free, and if you maintain $5,000 in your account, the bank will waive the monthly fees on an account that earns a bit of interest and refunds five out-of-network ATMs. With both accounts, you'll get free overdraft protection and a 24-hour grace period to deposit cash and avoid overdrawing.

Caveat: To avoid a high $3 out-of-network fee, you'll have to use one of the bank's 1,800 ATMs.

Where you can find it: Fla., Ill., Ind., Ky., Mich., Ohio, Pa., W.Va., Wis.

Key account: Huntington 5 Checking

Monthly service fee: $5, waived with a $5,000 combined balance

Interest: 0.15%

Northwest

Why it wins: You can't do much better than free ATMs and free checking and savings accounts. Plus, if you keep at least $1,000 in your checking account, Northwest will waive the fee on its interest-bearing option. The cherry on top? J.D. Power names it a regional winner for customer service.

Caveat: The bank is in only two states in this region (plus Ohio), with 162 branches and 10 drive-thru locations.

Where you can find it: N.Y., Ohio, Pa.

Key account: MyNorthwest Checking

Monthly service fee: $0

Outside ATM fee: $0

Finalist: TD Bank has a wide footprint on the East Coast and strong customer service scores. While high, the $15 monthly fee on the Convenience Checking account can be waived with a $100 minimum daily balance.

NBT

Why it wins: NBT has a free online checking account that pays a bit of interest and an out-of-network ATM fee that's well below average in the region.

Caveat: Apart from New York State, NBT is mainly in major cities. If you live in eastern Massachusetts, Rockland Trust has more branches and a reputation for outstanding customer service.

Where you can find it: Maine, Mass., N.H., N.Y., Pa., Vt.

Key account: eChecking (must be opened online, but you can still bank at a branch)

Monthly service fee: $0

Outside ATM fee: $1.25

Renasant

Why it wins: If you meet the requirements for the Rewards Checking account, which includes e-statements, 10 debit card transactions a month, and a direct deposit or online bill pay, you'll get $25 in ATM rebates and earn an interest rate that tops most banks' savings accounts.

Caveat: If you don't meet the requirements, you can still get a free checking account, but you'll be hit with $2.50 out-of-network ATM fees.

Where you can find it: Ala., Fla., Ga., Miss., Tenn.

Key account: Rewards Checking

Monthly service fee: $0

Outside ATM fee: $2.50, with up to $25 refunded if requirements met

Finalist: If you live in Arkansas, North Carolina, or South Carolina, Bank OZK is a strong option, with free checking and low out-of-network ATM fees.

Frost

Why it wins: Frost is a runaway champion in J.D. Power's customer service rating for Texas. It should be easy to avoid the $2 out-of-network ATM fee with more than 1,200 ATMs across the state, and the 0.2% interest on its savings account was among the highest we saw in Texas.

Caveat: If you like to travel or are often out of state, there's no way to avoid or get refunds of ATM fees.

Where you can find it: Texas

Key account: Frost Personal Checking

Monthly service fee: $8, waived with $100 direct deposit, $1,000 daily balance, or $5,000 combined balance

Outside ATM fee: $2

Money partnered with FindABetterBank.com to produce this year's Best Banks rankings. FindABetterBank.com provided account terms for more than 175 financial institutions, and our team reviewed account minimums and qualifications, ATM fees, overdraft fees, and interest rates. When selecting finalists, priority was given to checking and savings accounts with no or easily waived monthly fees, free ATMs, and higher interest rates. In naming free accounts, we assumed customers would be okay with receiving e-statements to avoid a monthly fee. When available, we weighed customer service ratings from J.D. Power's 2018 U.S. Retail Banking Satisfaction Study. Money's edit team independently fact-checked information in August and September.