These 12 Stocks Are the Best Values in 2019, According to Pros Who’ve Outsmarted the Market

- The Best Stocks for 2020, According to 3 Investing Pros Who Outsmarted the Market

- Investors in Active Mutual Funds May Get Surprise Tax Bills This Year. Here's Why

- Your Bond Fund May Be Riskier Than You Think

- Nervous About Stocks? There Are Great Opportunities in the Bond Market, According to Experts. Here's Where to Look

- If You Own a Mutual Fund, You Could Face an Unexpected Tax Bill This Year

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Not many stock pickers can beat the market—or even match it. But those who do often have some things in common: experience; a methodical, disciplined approach; and a knack for seeing value in places others have overlooked. That's why—assuming you're one of those investors who won't settle for the approach we usually recommend, an index fund—we think you might have something to learn from them.

With that in mind, we brought together managers of four such funds—two focused on the U.S. and two that look abroad—to better understand how they think. Below, you'll read about some of their favorite picks for 2019 (and beyond) and, perhaps more important, how they arrive at their decisions.

John Hancock Blue Chip Growth (JIBCX)

Manager: Larry Puglia

Expense Ratio: 0.84%

Minimum Investment: None

Since this fund's launch 13 years ago, manager Larry Puglia has always focused on the longer-term impact of a company's decisions, typically looking out at least five years. Because of this central tenet, consistent free cash flow has become one of his key valuation tools. It has proved to be "predictive of stock performance," Puglia says, since it's more difficult to manipulate than other numbers that companies report.

With this long-term mindset, he prefers to see company executives reinvest profits in their businesses by spending heavily on research and development, as opposed to making short-term efforts to boost the stock price, like drastically cutting costs to boost profit margins. Puglia says his commitment to R&D has only deepened in recent years, as the pace of technological disruption has increased. He has owned Amazon, for example, since 2005 because of its disruptive nature (it's not uncommon for Puglia to hold companies for decades).

Puglia's mindset often leads to big holdings in the information technology, consumer discretionary, and health care sectors. The strategy has worked for him, with John Hancock Blue Chip Growth outperforming the S&P 500 by four percentage points annually since the fund's 2005 inception.

AMAZON (AMZN)

Jeff Bezos's shop keeps coming out with new billion-dollar product lines, keeping Puglia invested. After launching Amazon Prime and cloud offering Amazon Web Services in the 2000s, the company has also recently added a lucrative advertising segment, Amazon Advertising, which has doubled its revenue to over $2 billion in the past 12 months. These side hustles are growing more rapidly than the core online store, says Puglia. As a result, he says, the company may be as much as 70% undervalued based on 2020 free cash flow expectations.

UNITEDHEALTH GROUP (UNH)

It's hard to imagine an insurance firm as a growth opportunity, but UnitedHealth has gone big in managing increasing costs for health care providers through data analytics. This business line, known as Optum, has become a 44% slice of UnitedHealth's revenue pie, and it's growing. Optum sales grew 11% over the past year, helping UnitedHealth Group increase earnings 13% as a whole. Despite a rise in stock price of nearly 140% in the past three years, Puglia says it's still underpriced.

VISA (V)

The provider of more than half of all credit, debit, and prepaid card purchases worldwide, according to The Nilson Report, Visa is well positioned to benefit as more countries shift away from cash. Plus, it's protected from competition owing to its scale. Even large payment systems, like PayPal, have chosen to partner with Visa—by making it easier for Visa customers to use debit cards on the systems' online platforms— rather than compete directly. That has enabled the California firm to grow at a "highteens rate," year after year, says Puglia.

Causeway Emerging Markets (CEMVX)

Managers: Arjun Jayaraman, MacDuff Kuhnert, Joe Gubler

Expense Ratio: 1.4%

Minimum Investment: $5,000

Emerging markets have seen better days. Between the Trump administration's trade war and rising U.S. interest rates, many smaller economies are looking for a reset. But those problems also create opportunity for value pickers, according to Arjun Jayaraman, co–portfolio manager at Causeway Emerging Markets Fund.

Jayaraman primarily uses a quantitative, data-driven approach, looking for strong balance sheets and growing earnings. He also seeks companies that have natural advantages, like a dominant product or a lack of competition in the marketplace. But when dealing with economies trapped in a trade war, for example, it's not always easy to detail the impact with numbers. For that reason, so-called qualitative measures—i.e., those involving human judgment—also play a role in his investing process.

Using this formula to assess businesses' intrinsic value, Jayaraman tries to buy shares in firms whose stock price has taken a hit, for one reason or another. The philosophy can lead him into areas that look troubled, like Turkey, for example, which has seen its currency tumble. "The valuation is so compelling," says Jayaraman, adding that the bet should work out if Turkey can circumvent its large debt load. This boldness has proved successful, with the fund returning 11% annually over the past decade, compared with 8.8% for the MSCI Emerging Markets Index.

ITAÚ (ITUB)

The holding company for a Brazilian bank of the same name could benefit if economic changes, including pension reform and privatization of government-controlled companies, are passed under newly elected far-right President Jair Bolsonaro. If efforts to stabilize Brazil's economy work, then banks should thrive,with more demand for loans and fewer borrowers defaulting. And Itaú is priced at 8.4 times its 2019 earnings, compared with 9.7, on average, for other Latin American banks, according to Jayaraman.

SAMSUNG ELECTRONICS (SSNLF)

The good news: While the U.S. accounts for roughly a third of Samsung sales, the company manufactures most of its popular phones and other gadgets outside China, so business has not been hampered by the U.S. trade war. The bad news: The stock has nonetheless fallen 16% over the past year owing to fears its memory business, which is sensitive to U.S. economic conditions, could falter if growth slows. Still, upcoming products, like a hotly anticipated foldable phone, and the already-cheap stock price, mean Samsung's upside outweighs its risks.

PTT (PUTRY)

Thailand avoided heavy borrowing in U.S. dollars when U.S. interest rates were near zero. As a result, its economy has remained strong at a time when rising rates have sapped spending power in other emerging nations. The thriving Thai economy's demand for energy has helped PTT, which both extracts oil and gas from the ground and markets it to Thai consumers. The stock, Jayaraman's fourth-largest holding as of October, also boasts a 4% dividend yield, compared with about 3%, on average, for other stocks in the MSCI Emerging Markets Index.

Parnassus Mid Cap (PARMX)

Managers: Lori Keith, Matthew Gershuny

Expense Ratio: 0.99%

Minimum Investment: $2,000

So-called socially responsible or ESG investing (ESG stands for environmental, social, and governance) has long remained something of a niche. Investors have been understandably skeptical of picking companies for their virtue rather than their business prowess, fearing that would mean sacrificing investment returns. But co-managers Lori Keith and Matthew Gershuny argue that their focus on corporate citizenship doesn't hurt and could actually boost performance in the long run, since companies that are socially irresponsible also tend to be risky as businesses.

Unlike many ESG funds, which simply screen out sin stocks, such as tobacco or gun companies, Parnassus also uses a qualitative approach, delving into firms' pay structures, morale, and the value they bring to their communities. Parnassus then determines which do-gooders are likely to show healthy profits. Without a competitive moat and strong growth prospects—typically over three years at least—Keith will pass on even the most virtuous name. The fund's returns have essentially matched those of the Russell Midcap Index over the past decade, although with less volatility—thanks in large part to the managers' focus on downside risk.

XYLEM (XYL)

Xylem helps municipalities provide clean water—a vital need given the number of people who lack access to filtered water is at 1.1 billion and growing. Working with treatment plants, Xylem stands to benefit as more and more aging infrastructure requires updates. Its fast-growing monitoring arm, which helps warn customers of leaks at plants, creates a consistent revenue stream. The upshot: Keith sees Xylem's overall sales growing 5% to 10% a year going forward, up from a recent pace of about 4%.

CADENCE DESIGN SYSTEMS (CDNS)

When a chipmaker develops a new product line incorporating machine learning or virtual reality, it utilizes Cadence Design Systems tools. This leaves Cadence on the cusp of some very exciting trends, especially since there could be as many as 1 trillion connected devices by 2035. Plus, Cadence and its closest competitor, Synopsys, run a virtual duopoly, producing, Keith says, the "widest moat business" that she invests in. And CDNS's high rate of diversity and inclusion, according to Parnassus research, boosts its ESG standing.

MOTOROLA SOLUTIONS (MSI)

PARMX's largest stake is in this developer of emergency radios for first responders. These radios provide service in the worst conditions— like hurricanes—and have to remain near 100% reliable. MSI's customers are public organizations, like local governments, and, unlike more fickle private companies, they tend to stick with the same vendors year in, year out, once they have proved themselves. Motorola—which spun off its cell phone line in 2011—has also improved its monthly service offerings, like cybersecurity protection, producing a recurring source of cash flow that accounts for 41% of revenue.

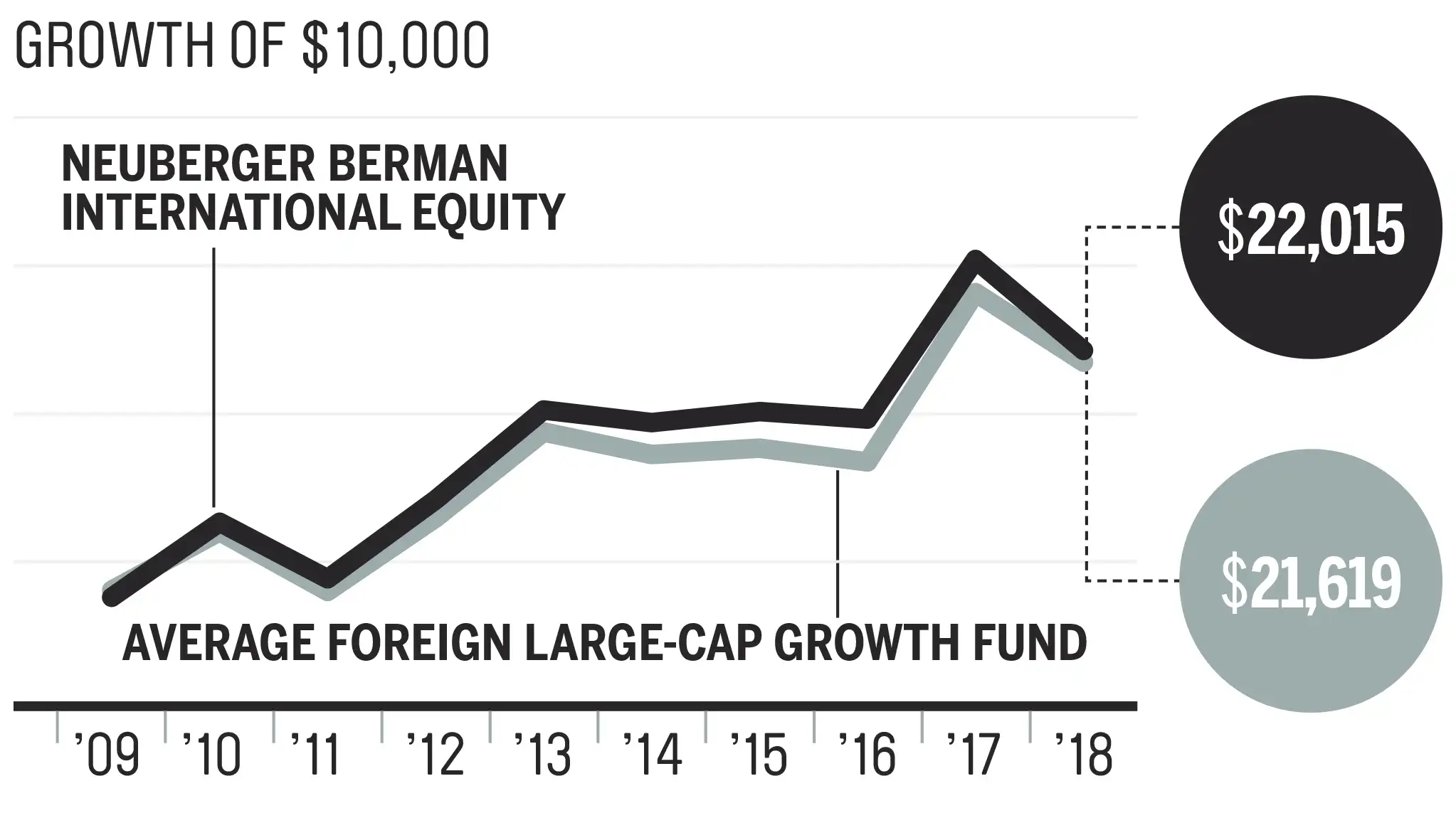

Neuberger Berman International Equity (NIQVX)

Manager: Benjamin Segal

Expense Ratio: 1.23%

Minimum Investment: $1,000

Owning international stocks in your portfolio is supposed to provide a buffer for when the U.S. economy stumbles. The problem is, many of the largest, best-known global stocks are just that— meaning they can be dragged down by a bad U.S. economy just like domestic ones. That's why Benjamin Segal, manager of the Neuberger Berman International Equity Fund for the past 13 years, looks for small, medium, and large companies that operate independent of U.S. economic fluctuations. If he invests in a small-cap English firm, for example, he's more certain it'll "be driven by the U.K. economy," Segal says.

Segal seeks out companies that have a history of returning cost of capital by at least 12% (the average in the portfolio is closer to 20%). They must also have low debt and an attractive stock price and prove good governance. These criteria tend to steer him to Europe and the U.K. and away from emerging markets in Asia. The focus on debt can also force Segal to avoid firms that grow rapidly through borrowing, so the fund can underperform during rising markets, then outperform in falling ones. Over the past 10 years, the fund's 8.5% average annual return has outpaced that of the MSCI EAFE Index, a benchmark for developed-country stocks, by about 1.5 percentage points a year.

TECAN GROUP (TCHBF)

There's an arms race in the pharmaceutical industry to develop new drugs at lower cost. But pharmaceutical firms can be loaded with debt—a result of high research and development costs—keeping Segal away. Tecan, a small Swiss business, doesn't itself make pharmaceuticals. Instead, it provides equipment that enables drug companies to automate testing of their new discoveries. Tecan's automated workflow equipment, used in testing HIV and hepatitis drugs, among others, is a market leader. As a result, Segal says, the company is on an "insensitive growth trajectory."

Alibaba sales topped $30 billion on 2018's Singles Day—China's answer to Black Friday.

ASML (ASML)

This Dutch firm helps semiconductor makers build ever-more complex and dynamic chips. It's the leader in extreme ultraviolet lithography, a process, set to be commercialized in 2019, that increases a chip's power a hundred times over what's available today. You can expect to begin seeing these chips in next-generation technologies, like automated cars and smart-home appliances. And ASML is in an envious spot, since no competitors match its technical leadership, according to Segal, and only a few even try, given the huge cost of developing new products.

ALIBABA (BABA)

Alibaba has become the Amazon, Netflix, and Snapchat of China, as the country shifts to a more consumer-centric economy. Alibaba's outlook has gotten a little murkier in the past year, thanks to the trade battle between Washington and China, which could slow Chinese growth. Still, with a 1.4 billion customer base and a government that backs this tech giant by reducing foreign competition within China's borders, Alibaba remains the sixth-largest holding in NIQVX's portfolio.