Where Are the Good Investments Now?

- Jack Bogle, Who Revolutionized the Way Millions of Americans Save and Invest, Dies at Age 89

- Why Trouble in China is Hitting Your 401(k)

- Why China's Currency Has Been Knocking Down U.S. Stocks

- Jack Bogle Explains How the Index Fund Won With Investors

- What Happens If the Social Security Trust Fund Runs Out in 2034?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

In 2015, Brian Rogers will step down as manager of the $30 billion T. Rowe Price Equity income fund, which he has led since 1985. Over the past 15 years, Equity Income has outperformed 67% of other mutual funds investing in large companies that are out of favor with investors, according to Morningstar.

Money assistant managing editor Pat Regnier spoke to Rogers in early July; this edited interview appeared in the August 2014 issue of the magazine. The S&P 500's level and valuation, as measured by the price-earnings ratio, are roughly the same today.

Q: Where are the good investments now?

A: Neither the stock nor the bond market is inexpensive right now. So it’s probably a time to be risk-sensitive and risk-aware. Equities are not overpriced the way they were in 1999, but in the context of history, the S&P 500 trading at 16 times this year’s earnings is an expensive multiple. And there are pockets within the equity market, whether it’s biotech or some of the social-networking-type companies, where investors ought to be concerned about high valuations.

On the bond side, the 10-year Treasury is yielding only 2.6%. [Note: Yields are 2.5% as of August 4.] It’s fair to say the bond market has surprised a lot of people. If I had been a fixed-income strategist on the first of January, I would probably be unemployed right now, because I was convinced rates would move up and prices would fall, but instead rates moved down. [Bond prices move in the opposite direction to that of interest rates.]

Q: What happened there?

A: The bond market has rallied because of concern about the durability of the economic recovery. At the same time, the equity market looked right past those weak growth numbers. So it feels like the two markets are at odds. I suspect that bonds are the more extended and overpriced.

The Fed seems to be getting more comfortable with the economy’s prospects; the debate over raising rates will intensify.

Q: What should a person do in this situation?

A: When everything is expensive, you have to be prepared to not make as much. That’s the issue for investors. If you earn 2.6% on bonds, and equities return 7% or 8% instead of the 10% of the past, that doesn’t feel great, but it’s really not all that bad.

Q: What do you mean by “be prepared to not make as much”? Is that just a psychological adjustment, or do I have to change my strategy?

A: There is a psychological adjustment, but also a lifestyle affordability adjustment. If you’re a retiree and the old game was getting a 4% to 6% fixed-income return on your nest egg, you’re in a different position today. If you maintain the same risk profile, you will be getting about 2.5%.

Q: So I might have to rethink how much I can safely draw from savings.

A: Absolutely, yes.

Q: You manage your firm’s Equity Income Fund, and you’re a value investor, meaning you look for stocks that are cheap relative to earnings. What’s this high-priced market like for you?

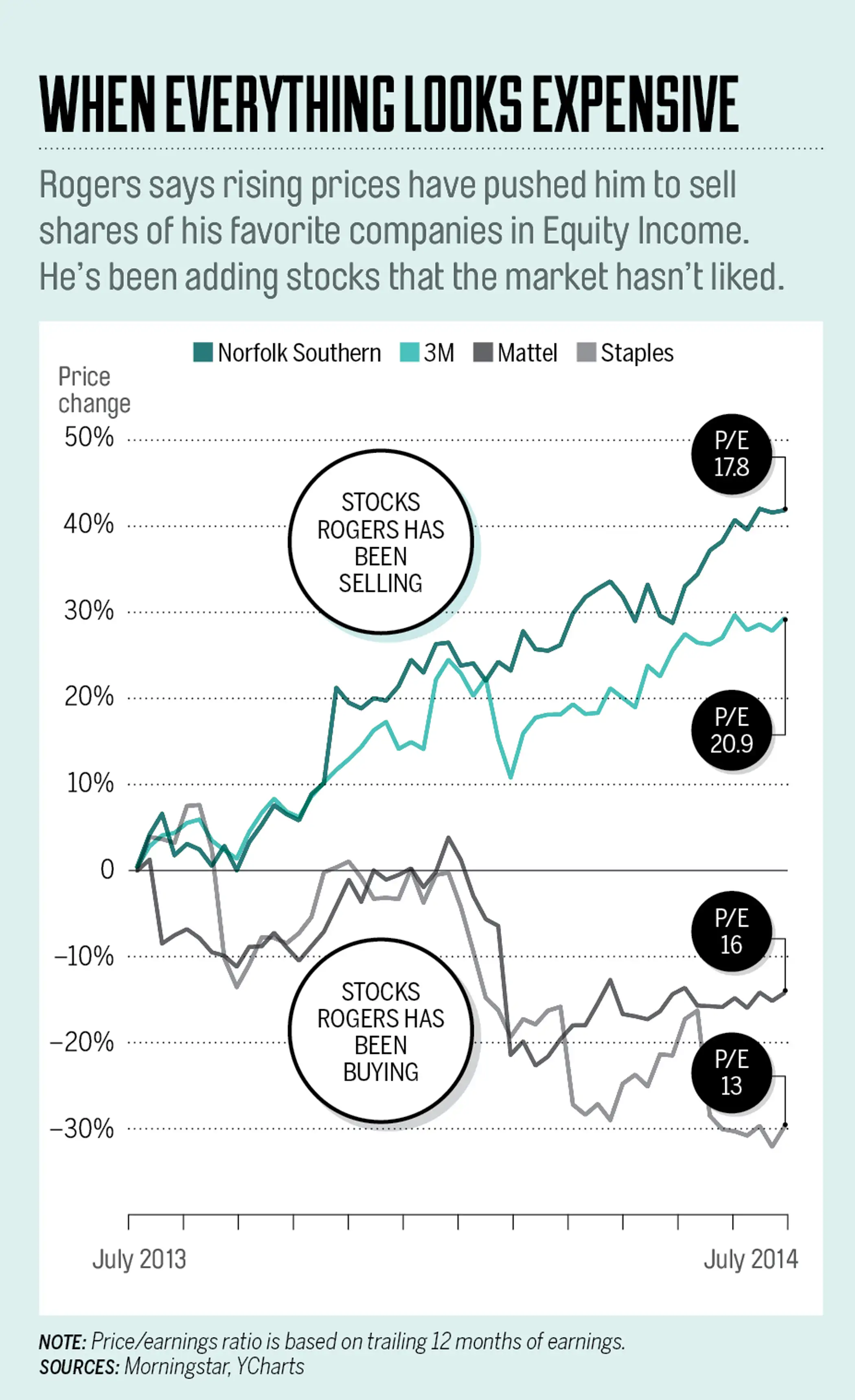

A: It’s simply harder to find things to invest in. And it’s easier to find things to sell or to trim. Great companies like 3M and Norfolk Southern, which we’ve had investments in, now look relatively expensive, and we’ve been selling.

Q: So what stocks look attractive now?

A: We look for laggards and emphasize quality. In terms of laggards, a company that we have a pretty big investment in is Mattel. It’s out of favor because the Fisher-Price and Barbie lines have been challenged, but I’ve been through this so many times with Mattel over the years, and they always seem to be able to execute fairly well. You get almost a 4% dividend yield, good cash flow, and strong financials.

Another laggard is Staples. It’s been a very disappointing stock recently [see graphic]. But a 4.4% yield [4.3% as of August 4]. Staples has a strong commitment to the dividend, so it’s almost like a fixed-income security where something good might happen someday.

In terms of quality-oriented stocks, I think General Electric is cheap right now. You have a 3.3% dividend yield. They’ve raised the dividend probably four times in the last three years.

Q: Why do you focus so much on dividends?

A: Dividends are a way for us to assess the relative value of a stock. For example, with Norfolk Southern having gone from $70 to $100, its dividend yield compared to its normal yield has diminished dramatically. [All else being equal, when a stock’s price rises, its dividend yield falls.] So its yield appeal has diminished.

Investors have flocked to dividend stocks to replace low-yielding bonds. Won’t those stocks get hurt when rates and yields do rise?

Very-high-dividend stocks that are basically fixed-income surrogates—AT&T and Verizon in my fund—will probably suffer if rates rise appreciably. But other companies have both decent yields and dividend growth. It’s less clear to me that those would suffer.

Q: About 20% of your fund is in financial services. Are you worried about risk building up in banks?

A: Banks and the financial system are in pretty good shape. Credit quality is improving. Banks have raised a lot of capital. When they stop paying multibillion-dollar fines, they’ll be able to rebuild capital even more. What takes us down next time will probably not be what took us down in 2008. It’ll be something else.

Q: Lots of investors are shifting to index funds and ETFs. Why buy an actively managed fund?

A: We’re not religious on active vs. index. Indexing is low-cost. It will rarely disappoint you. On the active side, many people want to try a bit harder. Our fees are reasonable, so we look better than many active managers.

Q: The performance of Equity Income has been similar to that of an S&P 500 index fund. So what’s the appeal?

A: Our case is a strong investment organization, a dividend focus that might get you a little more income, and sensitivity to market risk.

Q: You’ll step down as fund manager in 2015. How are you preparing?

A: I’ve done this transition before with John Linehan, the new manager. I used to manage another fund he took over in 2003. I don’t have to teach John much. I think our investors will be happy. I hope not too happy to see me go. Just happy enough.