What Couples Nearing Retirement Need to Do Now

When you were in your twenties and thirties, retirement probably seemed unimaginably distant. Now, if you and your spouse are in your late fifties or beyond, you are getting close to the point at which you can claim the rewards of a lifetime of saving and investing.

But there are still crucial decisions to make that can affect your happiness in the next few years and your financial security later in life. This is the time when your teamwork in saving and communicating can pay off in a retirement that is satisfying and meaningful for both of you.

Here are five key pointers:

Fine-tune your vision

In retirement, 75% of women but only 52% of men say they spend time socializing, according to TIAA; far more men than women engage in sports and outdoor activities (38% to 18%). Your priorities may lead you in different directions on where you want to reside. It’s time to find a compromise.

To get there, Michael Brady, president of Generosity Wealth Management in Boulder, asks clients questions such as “What does your average day in retirement look like?” and “Where do you see yourself spending the most time?” and writes their answers on a whiteboard. He circles all the similarities in the spouses’ answers. Maybe the wife wants to garden by the lake while the husband wants to visit museums in the city, but they both also plan to volunteer. Recognizing that commonality can help. “You get closer as you discuss this stuff,” Brady says.

Retirement may mean something very different to a longtime homemaker than to a worker leaving the office. Marge Howe, 86, raised nine children and helped her husband, Jim, with the family heating business. At retirement, she told him, “ ‘If you’re going to retire, I’m going to retire too, and I won’t cook,’ ” she recalls. The couple, who split their time between Cincinnati and the TOPS'L Beach & Racquet Resort in Miramar Beach, Fla., went out to eat a lot for several years before Marge took up cooking again.

Check your countdown clocks

On a personal level, spouses are often happiest if they retire within a couple of years of each other, financial advisers say. Still, retiring on the same schedule might not feel right if one of you is still enthusiastically taking on big challenges at work while the other is ready to bow out. Also, one spouse might retire several years before the other due to a difference in age, health issues, or a corporate downsizing; in some cases, an abrupt exit might require the still-working spouse to stay on the job longer.

A financial planner can calculate whether you can afford to retire now and how different your finances— including your nest egg and your Social Security benefits—would look if one or both of you delayed for a while. One consideration: Today’s boomer women are more likely than previous generations to collect Social Security on their own earnings records, a new study by Harvard economist Nicole Maestas found. Earnings are based on your 35 highest-earning years, so try to get to that number of years of paid work if you can.

Read more: Money’s Ultimate Retirement Guide for Couples also includes advice for duos in their 20s and 30s, their 40s, and their 50s. Plus, take our quiz to see if you and your spouse are on the same page.

Bridge the gap to Medicare

Early retirement may sound nice, but where will you get medical insurance and how much will it cost you until Medicare kicks in at age 65? A plan to rely on one spouse’s workplace coverage could go bad if that worker loses his or her job. Some 46% of retirees left the workforce earlier than expected, and of those, a quarter cited changes at their company as the reason, according to the Employee Benefit Research Institute. Coverage through the Obamacare marketplaces is a possibility, but a nonsmoking couple at age 60 would pay an average of almost $18,000 a year (before any subsidies) for popular silver plans, according to HealthPocket, a technology company that ranks health plans. If your spouse’s job situation isn’t rock-solid, maybe you should work to 65 too.

Tap a pension for protection

Deciding how to collect from a traditional pension plan is one of the biggest irrevocable decisions you may make. While these plans traditionally provide guaranteed monthly checks for life, some also offer a lump-sum payment. The company might prefer you take the lump sum. But if you and your spouse are in good health, the odds are you will benefit more from the income stream.

An income payout for only the worker’s life will give you the biggest check. By contrast, a joint-and-survivor benefit will be lower, but it will continue through the survivor’s lifetime.

Say you are entitled to $4,000 a month for the worker’s life only; that might drop to $3,600 with a 50% survivor annuity and $3,200 with 100% to the survivor, says Jonathan Guyton, a financial planner with Cornerstone Wealth Advisors in Edina, Minn. Lean toward the 100% option if the survivor would have only limited income beyond Social Security, he says.

Be savvy about Social Security

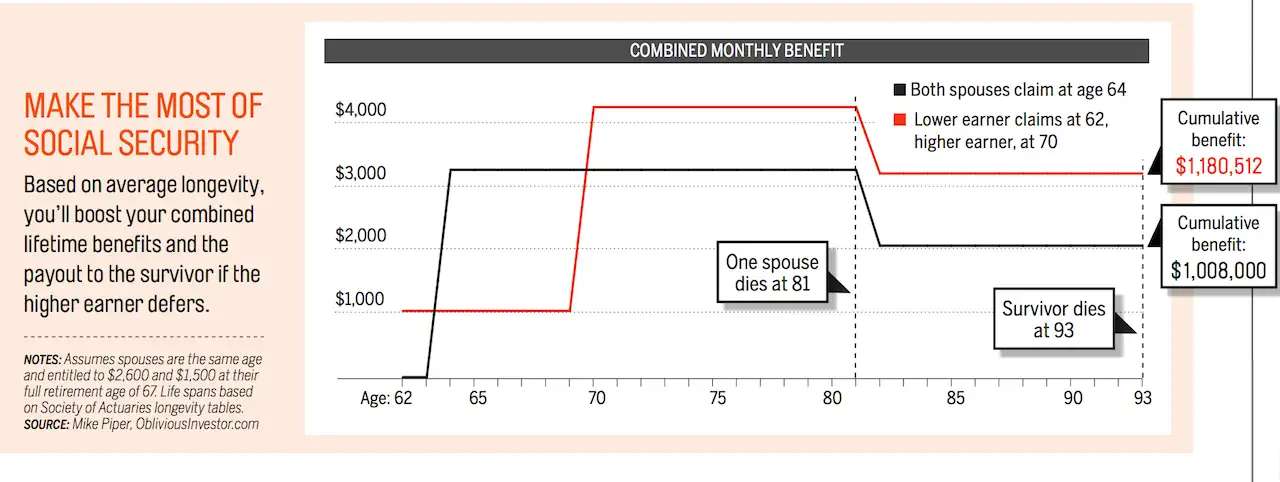

Each of you claims Social Security independently. But you should coordinate your timing in a way that is likely to provide the greatest combined benefit over your lifetimes. This is an especially important concern for women, since they are likely to live three to five years longer than men and more likely to collect a survivors benefit.

One of the best ways to keep income flowing late in life is for both spouses to delay claiming Social Security as long as possible, says Mike Piper, a CPA and the author of Social Security Made Simple. You can file for retirement benefits as early as age 62, but your payout rises some 6.5% to 8% a year for each year you delay up till age 70.

If it isn’t feasible for you to both delay claiming, the lower-earning spouse might file for benefits right away, while the higher earner waits till age 70. If the higher earner dies first, the increased benefits will go to the surviving spouse. This strategy, shown in the graphic above, works best if there’s a big difference in earnings.

You can compare the impact of different claiming scenarios based on your finances using an online calculator, such as SSAnalyze (free) or Social Security Solutions ($20 and up). After all the years of taxes, make the most of this bedrock program.