The 7 Retirement Moves Couples in their 50s Should Make Now

Many people head toward retirement as part of a couple. But that doesn't mean that spouses are working together as a team.

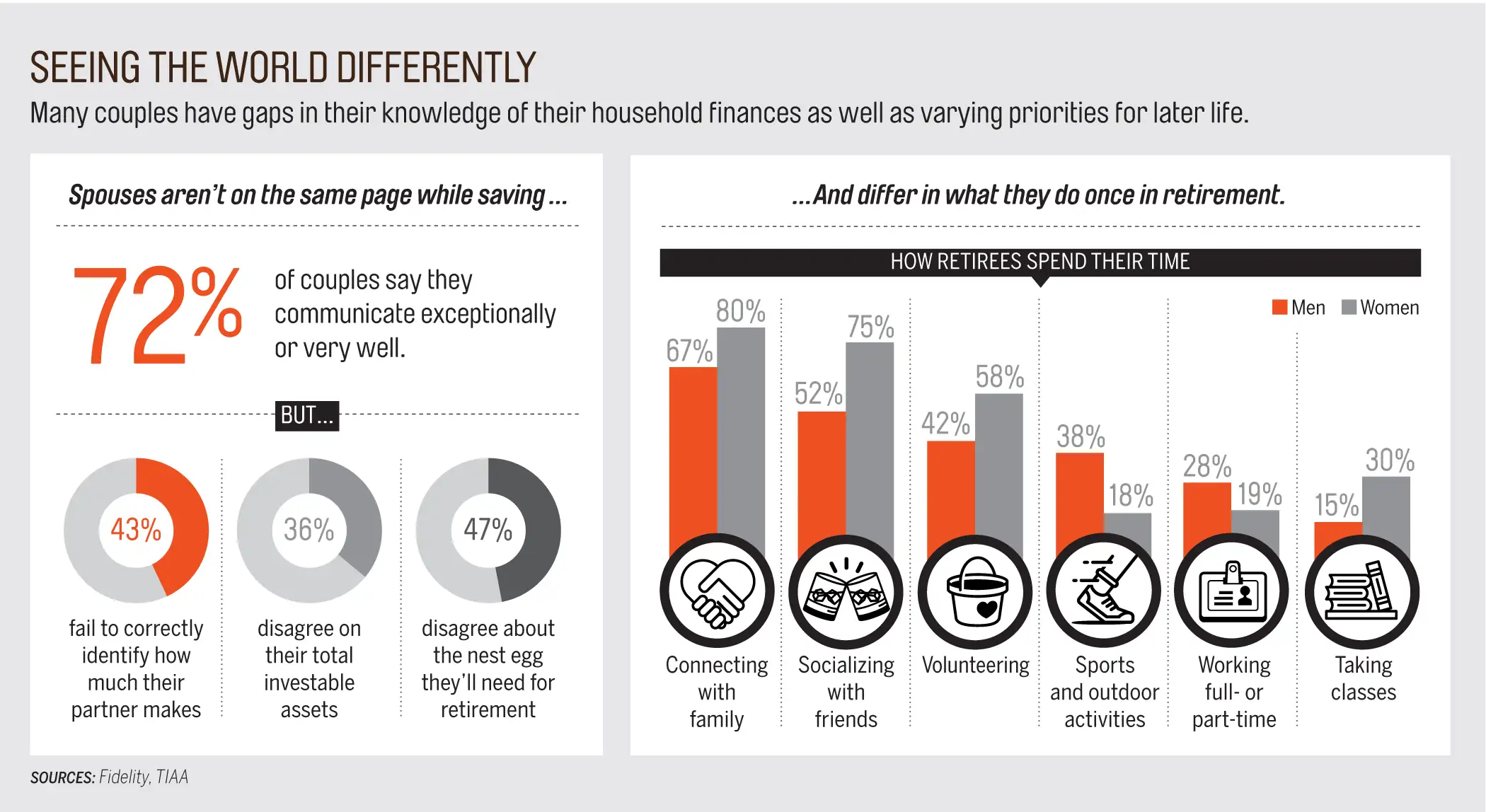

Only one-third of couples have even discussed retirement planning, according to a 2016 study by consultants Hearts & Wallets. Asked how much money they think they will need for retirement, 47% of couples disagree, Fidelity recently found. And men and women often have different interests in later life, with far more men than women engaging in sports and outdoor activities, and far more women than men getting together with friends and family, according to new TIAA research.

Getting on the same page about saving and planning for post-career life is critical for couples in their 50s, for whom retirement is suddenly not that far away. "Eighty percent of reaching your goal is defining what your goal is and having a plan for speed bumps that could derail you,"says Michael Brady, president of Generosity Wealth Management in Boulder.

Your fifties may provide an opportunity to turbocharge savings, as you’ve advanced in your careers and put the biggest money obligations to your children behind you. Or your finances may be pinched by new challenges, like a career setback or obligations to aging parents. If you are remarried, you may be recovering from the costs associated with your divorce. A lot is at stake.

Here are seven smart moves you can make at this stage of life that will help you transition comfortably to the next one.

Put a price tag on retirement

You may still be talking about whether you’ll stay right where you are or move to that beachfront condo you’ve been eyeing, but it’s time to get serious about some numbers. Vanguard has a tool that can help you rough out a retirement budget.

Plug those estimated expenses into an online calculator, such as T. Rowe Price’s version, to see if your savings are on track.

Play catch-up

When kids leave home, empty-nesters typically increase their 401(k) saving by less than 1% of pay, a recent Boston College study found. That may not be enough to get you where you want to go. So before you find new ways to use those dollars, bump up your saving by the amount you had been spending on tuition and room and board. The rules on catch-up contributions to retirement accounts can help. Starting at age 50, you can add an extra $6,000 a year to a 401(k), up to a $24,000 maximum; IRA investors can put in an extra $1,000, for a total of $6,500 a year.

Beth Weimer, 57, says neither she nor husband Russ, 56, "really planned well during our first marriages.” When they got together in their mid-forties, they made preparing for retirement a priority. Russ worked out a plan that could enable them to retire before age 60, assuming they set aside about 20% of their pay each year. “You have to have a shared vision,” says Beth.

Simplify and share

By now, you each may have accumulated multiple retirement and investment accounts, and despite your best intentions, one of you may be mostly out of the loop on financial matters. Twenty-four percent of partners worry that their mates wouldn’t be able to manage finances without them, and 18% say their mates are completely unengaged, according to a Hearts & Wallets survey Meanwhile, money skills peak around age 53, research shows, and they typically deteriorate as you age.

Do your spouse and your future self a favor by consolidating your money into fewer accounts at fewer firms. That will also make it easier to look at your overall mix of stocks, bonds, and other investments and decide—together—if it’s appropriate.

To see if your investment risk tolerance matches your spouse’s, you can both try this CalcXML tool. A typical allocation for a couple in their fifties might be 65% to 75% stocks and 25% to 35% bonds.

Read more: Money’s Ultimate Retirement Guide for Couples also includes advice for duos in their 20s and 30s, their 40s, and nearing retirement. Plus, take our quiz to see if you and your spouse are on the same page.

Close the bank of Mom and Dad

Adults ages 18 to 34 were slightly more likely to be living with their parents than with a spouse or partner in 2014, for the first time in 130 years, according to the Pew Research Center. And even for those who have flown the coop, you may still be helping with expenses. To keep your retirement saving from going off track, brainstorm with your child to come up with a plan toward financial independence.

“Set both short-term and longterm goals to make it more achievable,” says Kathleen Adams, a financial planner in Redondo Beach, Calif.

Perhaps your daughter will find a part-time or full-time job in three months, with an eye toward affording an apartment she can share in a year or two.

Don’t confuse retirement and holidays

You can use vacations to check out possible retirement locales. Keep in mind, though, that vacationing in a spot is different from actually living there. Loretta and Bruce Parker, now 71 and 75, had long thought they would retire to a lake house they owned an hour or so from their home in Rochester, N.Y. But when they finally moved there, they lasted just a few months. What had been a peaceful retreat during their working years turned into too much solitude

“When we tried to do it 24/7, it was deadly quiet for us,” Loretta says. So they instead moved to Bradenton, Fla., where they enjoy an active lifestyle that includes tennis, visits to the gym, and socializing with friends.

Weigh extreme action

One-third of workers age 55 or older have a nest egg of less than $25,000, according to a 2016 survey by the Employee Benefit Research Institute. If you’re behind the eight ball, downsizing—when done right—might make a big difference. You funnel a chunk of home-sale profit into savings, plus trim your monthly expenses. But make sure your total costs would drop significantly. Property taxes vary widely, notes Nancy Collamer, founder of MyLifestyleCareer.com, and that smaller condo might have a higher levy than your current house.

If you won’t be able to retire in your early or mid-sixties, make sure you’re in a job that will take you the distance. That might not be your current sales post, say, if it requires a lot of travel and late-night meals with clients. Make a move now, when you’re likely to be a more attractive candidate to employers than you will be in your sixties.

Stay in shape

Keeping physically fit will help you stay on the job and give you energy that will make you appealing to prospective employers, says Kerry Hannon, a career and retirement expert. Plus, you may face lower bills for drugs and health care as you head into retirement, and you’ll be able to be more active and adventurous.