#3: Invest Like a Cheapskate

Flip open a newspaper or turn on CNBC, and there’s no shortage of experts telling you how to be a better investor. The thought of dramatically improving your investment returns may seem tantalizing. After all, $100,000 becomes a million bucks in just over 20 years if it grows 12% a year. At 7%, you’re looking at a 35-year wait.

Here’s the problem: Attempting to be George Soros and failing is worse than not trying at all. It can set you back years. Just ask hedge fund investors. Over the past decade their portfolios returned just 2.6% a year, less than half the gains of a 60% stock/ 40% bond strategy, Wall Street’s equivalent of a dry turkey sandwich. Even in the financial crash, the average hedge fund did no better than a 60/40 portfolio.

What to Do

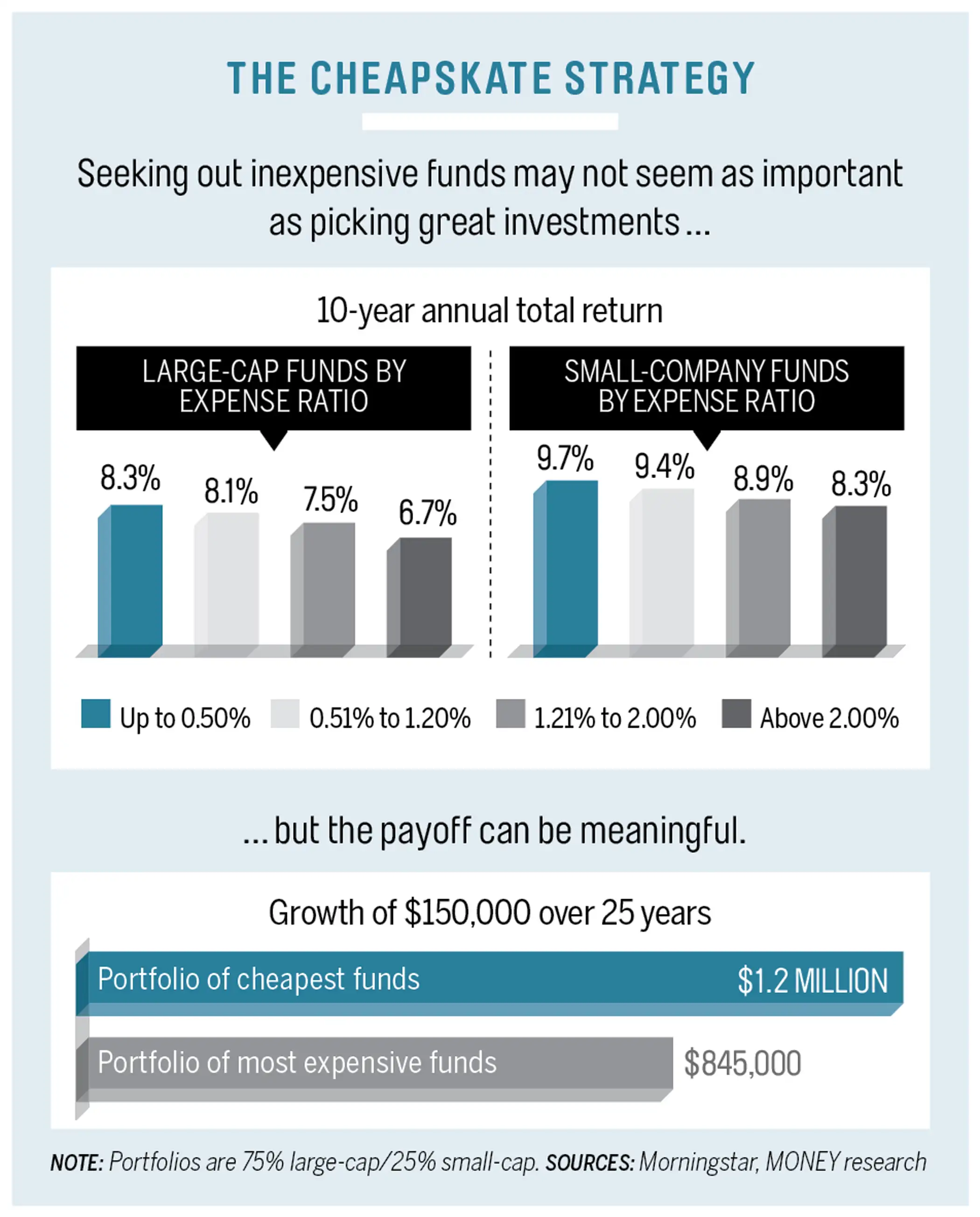

Keep costs below average. One reason sophisticated strategies fail is they’re expensive. Even the average actively managed stock fund charges 1.26% of assets a year. This comes directly from your returns. So it’s not surprising (as the chart at right shows) that the lower a fund’s expenses are, the more likely it is to produce bigger gains. Even shaving one point off your overall expenses—through funds like Schwab Total Stock Market Index (SWTSX), which charges just 0.09%—can be the difference between hitting your target and falling short.

Play the averages. History shows that one way to boost your returns without adding undue risk and costs is to increase exposure to so-called value stocks. These are shares of overlooked companies trading at discounts. Not only do value stocks beat shares of fast-growth companies by around 1.4 percentage points a year over the long run, but these stocks also outperformed in 73% of the rolling 10-year periods since 1979.

If you own a total stock market fund, you’re evenly split between value and growth. With new money, add funds like Vanguard Windsor II (VWNFX) until value gets to around 60% to 65% of your equities, says financial planner Ronald Rogé.

Strive to lose less than average in downturns—but in a smart way. While investors focus on scoring gains in bull markets, minimizing losses in bears is just as important, says Greg Schultz, a principal at Asset Allocation Advisors in Walnut Creek, Calif.

Don’t assume you can accomplish this by fleeing stocks. From 2003 through 2013, U.S. equity funds rose 8.2% a year. But investors saw gains of just 6.5%, largely because they bailed out in the crash and stayed on the sidelines too long, missing the rebound.

Here’s a better approach: Seed your portfolio with funds that have a knack for investing well, even in lousy markets.

Morningstar measures how funds have performed compared with their peers in months in which stocks have lost value. Among the best blue-chip funds on this score over the past five and 10 years is Parnassus Core Equity (PRBLX), which has beaten the S&P by 2.5 points a year over the past decade. The fund doesn’t set out to be conservative, says Morningstar senior analyst Laura Lallos. But smart stock and sector moves, plus a 75% stake in dividend-paying stocks have helped. For smaller stocks there’s Weitz Hickory (WEHIX), which is on the Money 50 list of recommended mutual and exchange-traded funds.