Saving for College vs. Saving for Retirement: Why the Conventional Wisdom Is Wrong

Financial advisers often tell parents that they should save for their own retirement first and their children’s college educations second. They support this advice with simplistic sound bites such as “You can borrow for college, but you can’t borrow for retirement.”

But I’ve done the math, and the experts are overstating the case. You end up with much more money in retirement if you set aside money for retirement and college when your kids are young than if you just put all your savings into retirement accounts.

Here’s why the experts are wrong:

First of all, you can borrow for retirement—through a reverse mortgage, although those have their downsides.

Secondly, just because you can borrow for your kids’ college (through federal Parent PLUS or private parent loans, for example) doesn’t mean you should. The interest rates on parent loans typically exceed what you’re likely to earn on savings, so paying for college out of savings is more financially advantageous to you in the long run.

Check out Money’s 2015-16 Best Colleges rankings

Here’s the savings strategy that results in the highest total retirement savings:

- Maximize the employer match on contributions to retirement plans, since that is free money.

- Build an emergency fund with at least three (but preferably six) months’ living expenses.

- Pay down all high-interest debts, such as credit cards.

- Save for the child’s college education in a 529 savings plan. If you can manage it, aim for saving enough to cover at least one-third of future college costs. For a child born this year, that means saving $250 a month from birth for future enrollment in a public four-year college.

- Save the rest in retirement plans. Again, if you can manage it, a good rule of thumb is to save a fifth of your income during your working career to pay for the last fifth of your life, in retirement.

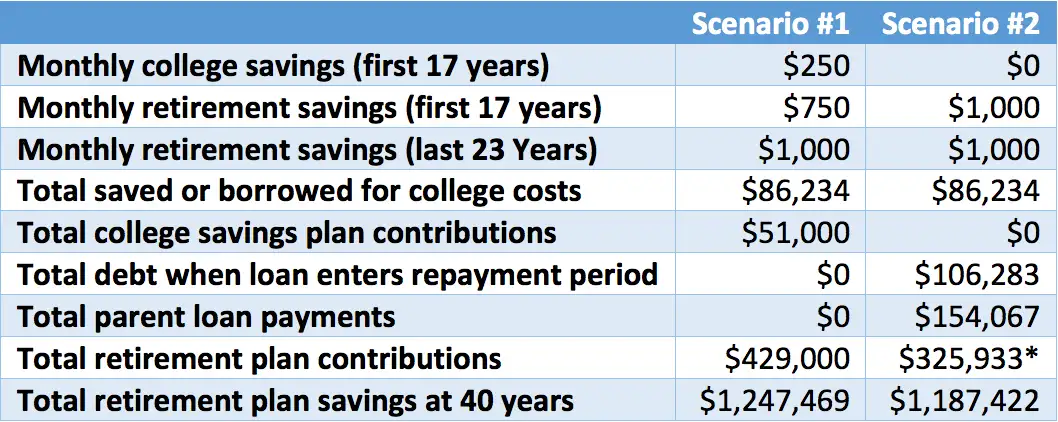

Here’s why this strategy pays off in the long run. Consider two scenarios in which parents save $1,000 per month for 40 years in tax-advantaged accounts. Assume an average annual net return on investment of 4.9% on college and retirement savings and an interest rate of 7.9% on the parent education loans.

- In the first scenario, the parents save $250 per month for college in a 529 savings plan for the first 17 years for college, and the rest for retirement.

- In the second scenario, the parents save the full $1,000 for retirement for all 40 years and plan on borrowing the amount they would otherwise have saved for college. However, the loan payments will be deducted from the amount the parents would have saved for retirement, for a total of 10 years starting six months after the student graduates from college.

The first scenario yields $79,690 in college savings at the end of the 17-year period. Assuming that the parents use about a quarter of the money each year the student is in school and that the remaining college savings balance continues to earn a return while the student is in school, this covers a total of $86,234 in college costs. At the end of the 40-year period, the parents have saved $1,247,469 for retirement.

In the second scenario, the parents also spend a total of $86,234 to pay for college, but they borrow the money instead of saving it. With monthly interest capitalization during the in-school and six-month grace period, this grows by 23% to $106,283 by the end of the grace period. Over the 10-year repayment term, the parents make a total of $154,067 in loan payments. At the end of the 40-year period, they have $1,187,422 for retirement. That’s $60,047 less than the retirement savings in the first scenario.

*This number reflects the years that the Scenario #2 parents were unable to contribute their full $1,000 a month toward retirement because they were making loan payments ($480,000 - $154,067 = $325,933).

The only time borrowing for college costs is financially beneficial is when the interest rates on parent loans are lower than the equivalent long-term earnings rate on your investments. But that just doesn’t happen very often. True, private lenders are advertising parent loans starting at about 2%, but those are variable rates that are likely to rise over the years.

In early July of 2015, some lenders were offering parents fixed rates as low as 5.1%, but according to Morningstar, the average 529 investor has been earning total returns of only about 4% , even during the recent bull market, in part because funds for older students are parked in safe, but very low-yielding, bonds. And while retirement savers have been earning higher returns—typically about 10% a year over the last five years, according to Vanguard—those returns are not guaranteed in the future, and can vary dramatically depending on your timing. During any 17-year period, the S&P 500 is likely to drop by at least 10% at least twice.

So the next time a financial expert compares airplane safety briefings (where the flight attendant tells parents who are sitting next to a child to put their own oxygen masks on first) with whether to save for college or retirement, remember that the flight attendant isn’t paying for your child’s college education.

Read next: Find Out How the Common App Has Changed This Year

Mark Kantrowitz is senior vice president and publisher of Edvisors.com. He writes extensively about financial aid, scholarships, and student loans.

For more advice on paying for college and our latest college rankings, check out the new Money College Planner.