Here's the Right Way to Invest for Growth

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Moderator Paul J. Lim, assistant managing editor, Money: Why is dividend growth—focusing on companies that can increase their payouts year in and year out—so important?

Luciano Siracusano, chief investment strategist, WisdomTree Investments: Right now there are roughly 1,400 companies in the U.S. that pay regular cash dividends, and they pay out in total about $410 billion. The dividends are in effect the vegetables. They're the nutrients underneath the stock market that allow it to grow over time.

Over long periods, that American dividend stream has grown at roughly 5.5% per year. Over the last five years dividends in the S&P 500 have compounded about 13% per year. That's in a period where the S&P 500 returned 14.5% per year. So the lion's share of the equity return was driven by aggregate dividend growth.

PL: How has this dividend growth strategy performed historically?

LS: We're talking about the potential maybe to generate one or two percentage points above the S&P 500 over long holding periods, not in any one particular year. That advantage is why people start thinking about how this can be additive to their portfolio.

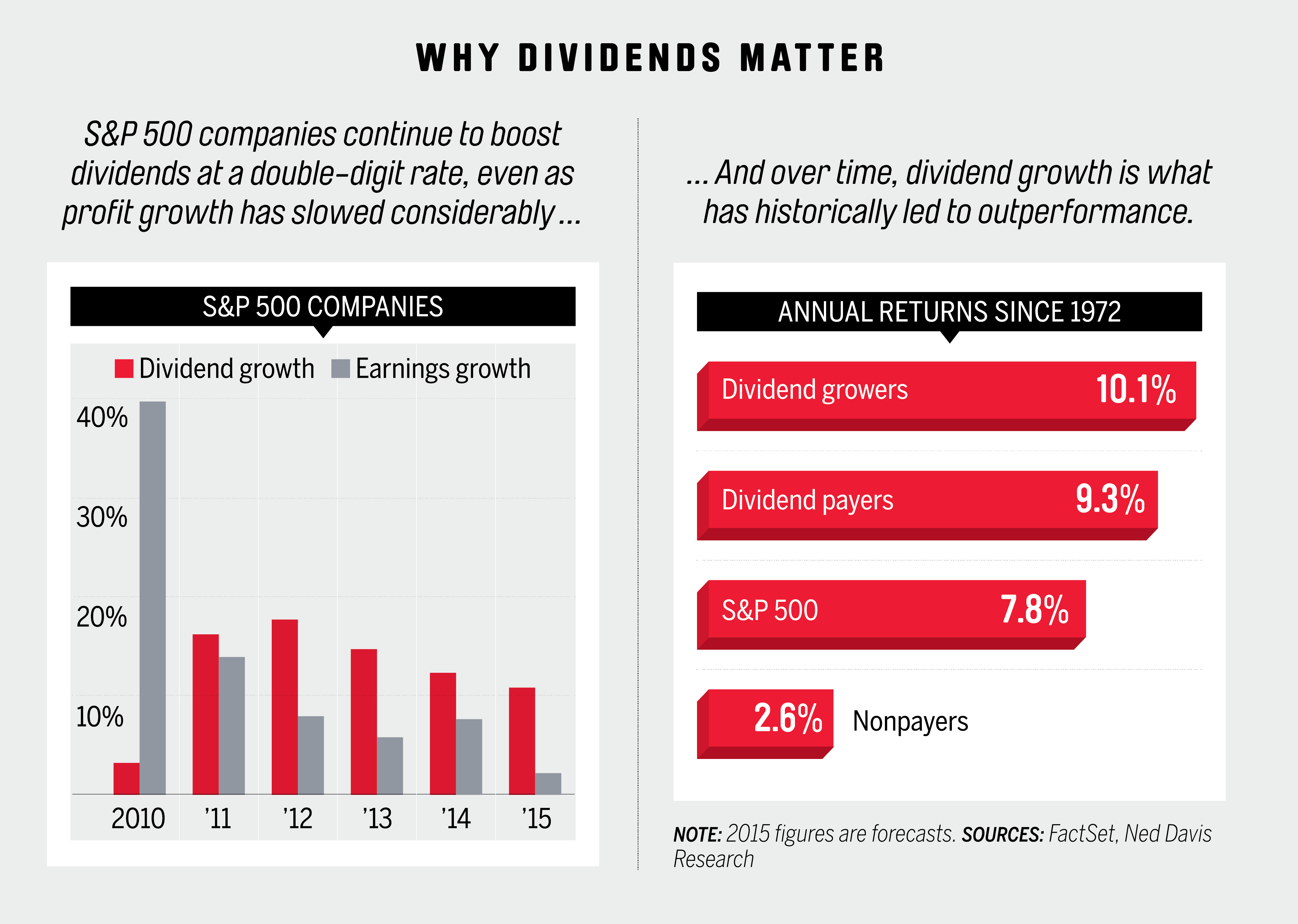

PL: Is today's environment—marked by slowing earnings growth and low yields that are expected to rise—a good one for dividend growth stocks?

Mark Freeman, chief investment officer, Westwood Holdings Group: The short answer is yes. It's really the latter point you touched on—the yield environment—that's a key point investors need to understand. In a rising-rate environment, the ability of a company to raise its dividends is a shock absorber, if you will, to offset some of the negative impact from higher interest rates.

PL: Before we get too far along in this discussion, we should note that dividend growth stocks are a different beast than the high-yielding dividend shares those seeking current income gravitate toward, right?

Christine Benz, director of personal finance, Morningstar: That's exactly right. It's a different strategy than one that is strictly yield focused. In particular a dividend growth strategy would tend to exclude utilities. It would tend to exclude some of the stodgy telecom services companies. Those companies typically would not be on the shopping list of a dividend growth investor.

PL: What sectors would be?

LS: If you're asking where are dividends growing the quickest, you'd probably look at tech. If you look back at the last seven years, you would be struck by how fast technology has grown the overall dividend stream.

PL: How do the dividend growers look compared with those high-dividend yielders when it comes to valuations?

MF: I think they're much more attractive. I would actually argue that if you look at stocks that only offer yield, they're priced very much like bonds [meaning they're very expensive].

CB: High yielders have also behaved like bonds in a lot of ways recently. When we've seen a few interest-rate-related tremors, we've seen long bonds go down in price, but we've also seen high-yielding utility stocks and REITs to some extent suffer as well.

PL: Christine, when we're talking about companies that can reliably increase their dividends over time, is this a back-of-the-envelope way of getting at high-quality names?

CB: I think it is. In fact, I was screening the universe of stocks we have on Morningstar.com, looking at companies that have had a history of dividend growth. They tend to look good from the standpoint of having financial stability and balance-sheet strength.

PL: Does the fact that a company is willing to increase its dividends speak to something else—perhaps management's confidence about future earnings growth?

MF: I think so. We talk almost on a daily basis with corporate management teams, and one of the things we constantly discuss with them is what their plan is for capital allocation. I do think when they make that commitment to dividends, it reflects not just their confidence in the company but also their outlook for earnings.

PL: Does this explain why we might be seeing more dividend growth opportunities in places like technology?

LS: There's definitely a connection between highly profitable companies and dividend growth over time.

You're in an environment now where earnings growth in corporate America is slowing but dividend growth continues to grow at a double-digit pace. That can't continue forever, but the double-digit dividend growth is giving you a window into what the corporate executives are thinking now. And the conclusion I draw is that the earnings lull we're in is temporary and that dividend growth is probably the better barometer to keep an eye on.

PL: Luciano, in your firm's Wisdom-Tree U.S. Dividend Growth Fund, the top holdings are found in traditional growth-oriented sectors, right?

LS: Yeah, the top weights now are consumer discretionary [roughly 20% of the portfolio], information technology [roughly 20%], and industrials.

PL: Mark, you're an active manager. Where are you finding opportunities for dividend growth?

MF: I would just echo Luciano's comments on tech. That is an area where we're seeing very strong growth and I think also a mentality shift by a lot of management teams.

The financial sector is another area, albeit one where you probably have to be a little bit more selective. And health care is another area where we continue to see growth.

PL: Health care has been on such a tear for four years. Are you able to find dividend growers at decent prices?

MF: Well, I'm never comfortable with price. I'd always like to have gotten in at a lower valuation, but the short answer is yes.

One stock I own in the Westwood Income Opportunity Fund is Becton Dickinson. If you look at it today, it's a bit expensive. But you always have to ask, What am I getting for that? We think we're getting sustainable earnings growth rates in the mid-teens, and that will be reflected in the dividend growth rate. As a matter of fact, Becton Dickinson over the last five years has a dividend growth rate of over 10%.

PL: Morningstar runs a newsletter specifically devoted to dividend strategies. Christine, are there any particular recommendations Morningstar DividendInvestor currently has with regard to dividend growth?

CB: I was looking at some of our highly rated stock picks with a history of dividend growth; four- or five-star ratings, meaning that our analysts currently think they're inexpensive; and a low "fair value uncertainty" rating. That means that the analysts feel they can do a pretty good job of predicting the company's future cash flows.

On the list were Baxter, Colgate-Palmolive, Exxon Mobil, Magellan Midstream, Nestlé, Procter & Gamble, Spectra Energy, and Wal-Mart.

In terms of funds, one that squares nicely with this thesis of dividend growth is the Vanguard Dividend Growth Fund. It is an actively managed fund that looks at a lot of the things my co-panelists look for. Also, it focuses on valuation as well as dividend growth. Another thing I like: It is a Vanguard fund, so it's got a nice, low expense ratio. That means that more of the income flows through to shareholders.

PL: Christine, once you settle on specific stocks or funds, where do you put those dividend growers in an overall portfolio?

CB: I've been working on what we call the bucket strategy for retirement planning. And that really means setting aside one to two years' worth of living expenses in cash, then maybe another three to eight years' worth of living expenses if you're retired in bonds, and then the rest you can have in stocks.

Certainly even high-quality stocks like dividend growth shares should be kept in the stock component. I would not use them as a substitute for bonds.

PL: We've been talking largely in the context of U.S. stocks. But dividend growth is a strategy that is applicable to a broader array of assets, right?

LS: Certainly in Europe and the international developed world, having a dividend growth strategy makes sense.

If you're thinking about the developed world and you're buying an index fund, it would likely be based off of the MSCI EAFE index. Well, a dividend growth strategy would try to identify companies with higher profitability in aggregate than the stocks in that index and then potentially the ability to grow dividends quicker.

PL: When you look back over time, how has dividend growth held up in down markets?

CB: Given where overall market valuations are right now, I think it's reasonable to start thinking about which parts of my portfolio would behave better in an equity market shock and which pieces might not do so well. I think the dividend growers would tend to do better.

LS: I wouldn't overstate it. If you have broad equity exposure and the market goes down 37%, these strategies are going to be going down 30%, 35%, but maybe even 40%.

Question from the audience: Christine mentioned four or five companies that Morningstar would recommend. I wonder if the two gentlemen could also identify three or four companies that they would recommend?

LS: Well, we don't do individual stock recommendations. But I would just say we monitor the entire market, and right now, of the 20 largest dividend payers in the U.S., 13 of them have raised their dividends since November, and five of them just raised it this quarter. Those five are Apple, Exxon Mobil [even though oil prices are down], Johnson & Johnson, Procter & Gamble, and Wells Fargo.

These increases are an important signal for the market that not a lot has changed at the corporate level in terms of dividend policy. If you want to just look at those five companies as proxies for their industries, those are the largest ones in their sectors.

MF: Just two others that I'd mention in addition to Becton Dickinson. Honey-well is attractive. That's a company that at least over the last several years has been able to grow its dividend quite strongly, and from an earnings outlook, we're also very favorable. Then if you're looking for something in the financials, Capital One is another name that we feel will do well over the next several years.

Audience: I've got a Roth, I've got a Simple IRA, and then I've got a TD Ameritrade account where I have some dividends. Every time we get a dividend, it's a taxable event. I was wondering how can I best compound my growth of dividends? Can I buy a dividend stock in the Roth IRA where it can grow tax-free?

CB: Roth accounts would be an ideal receptacle for anything with a dividend attached to it. Second choice would be a tax-deferred account such as a traditional IRA or 401(k). But definitely if you have a choice—and a lot of people don't in terms of which types of accounts they're using—you want to keep the dividend payers out of your taxable accounts.

LS: I would just add to that: If you can get a fund that focuses on qualified dividend payers, that might be a better avenue to go than funds that start to delve into real estate investment trusts and other companies where the income is being taxed at higher rates.

[In general, payouts from domestic stocks and certain foreign shares are capped at the maximum 20% federal qualified dividend tax rate. Most dividends thrown off by REITs, on the other hand, are treated as ordinary income, which means they're taxed at the maximum rate of 39.6%.]

CB: I suppose that's another feather in the cap for a dividend growth stock strategy in that it typically would exclude those nonqualified dividends.

Audience: I was just wondering if you set any limits to the amount of yield that you would go after? I noticed that some yields for REITs and so forth are 10%, 15%. Do you disqualify those automatically?

LS: I can only speak for what WisdomTree does. We have a screen where we're not going to include companies that have a payout ratio greater than one—meaning the dividends they pay out that year are greater than the earnings they generate. That's one way we deal with it.

The other way is we actually weight the securities in the index based on the aggregate amount of dividends they pay. Even if a company had a high dividend yield, we're not weighting by dividend yield. We're weighting by the absolute dollar value of the dividends that are actually being paid. That has a way of tilting the portfolio toward larger companies, and once you start looking at the larger businesses, it's very rare to find companies with dividend yields north of 4%.

Audience: Can you comment on developed-market vs. emerging-market dividends?

LS: Yeah, we actually calculated an index of emerging-market dividend payers. There are roughly 1,200 of them across the globe, so there are plenty to choose from, and if you look at the MSCI Emerging Markets index, about 90% of that is actually in dividend-paying securities.

I think there is a case to be made to have some emerging-market equity exposure, and certainly we have strategies that allow you to take advantage of the dividend-paying part of the emerging markets.

CB: I would just make a quick comment about narrowly focused strategies. The finer you slice things in terms of investments, the less you're likely to stick with it through a variety of market environments, and the worse investor outcomes you'll tend to get. So I think some sort of large diversified dividend growth fund looks really good.

PL: On that note, I want to thank all the panelists for a great discussion.

Adapted from "The Right Way to Invest for Growth," which appeared in the July 2015 issue of Money magazine.