Why You Shouldn't Fear a Fed Rate Hike

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Conventional wisdom says that if the Federal Reserve goes ahead and lifts rates this week, investors will view that as one more impediment to global growth, which could lead to yet more selling on Wall Street.

But even if the Fed hikes rates later for the first time in more than nine years, it may not be the end of the world, especially for investors with a time horizon longer than a few days.

Why?

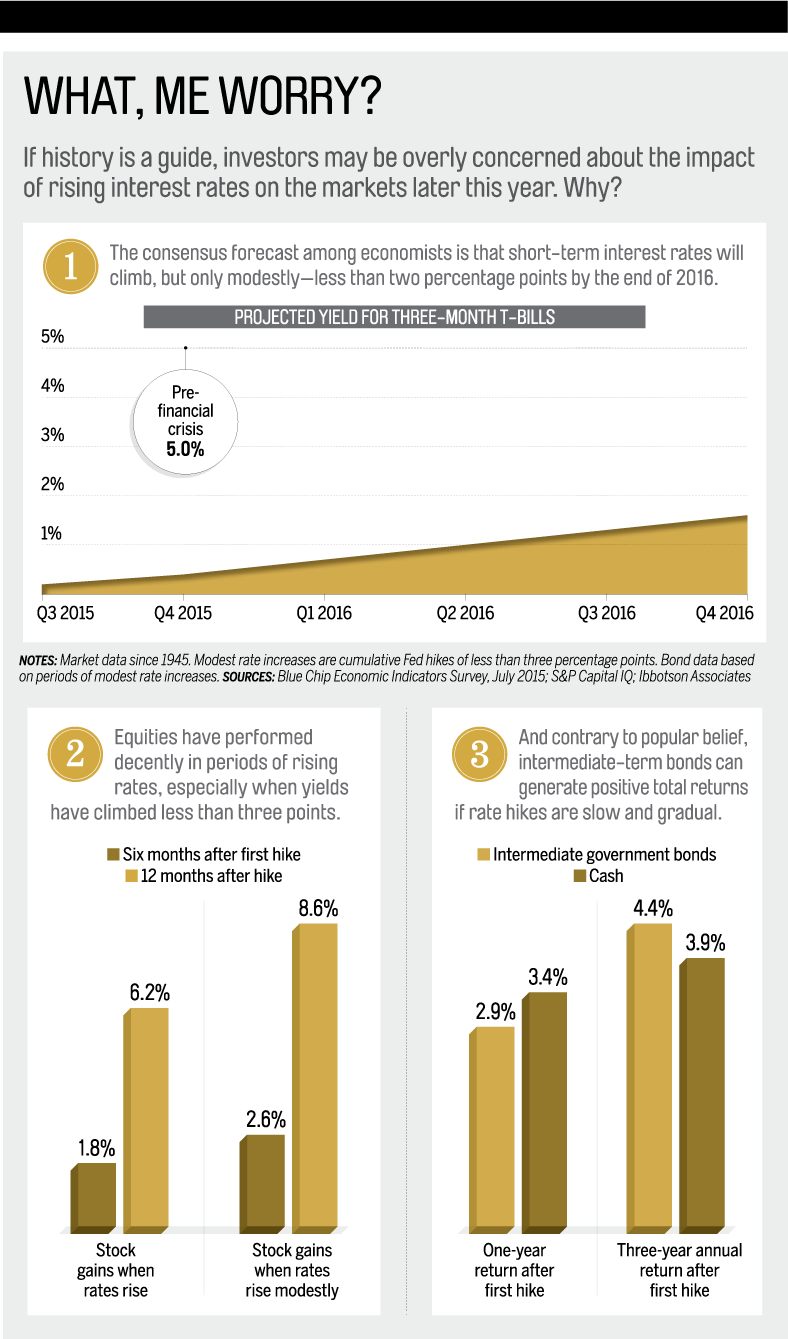

Should the Fed feel the need to begin the process of "normalizing" rates, there's a growing belief that the coming rate hikes will be slow and slight.

Policymakers who are planning to vote for a rate hike this week clearly believe the economy is strong enough to withstand a slight uptick in the Federal funds rate (which is what banks charge one another on overnight loans). But they also recognize that a quick and precipitous climb isn't warranted, as wage growth and inflation remain muted.

Read Next: What's At Stake If the Fed Raises Interest Rates This Week

In July, Fed vice chairman Stanley Fischer warned that inflation is too low and "we need to get it back up to 2%." To achieve that, the Fed's stated goal is to push rates up slowly over years, not months. That suggests the Federal funds rate may remain below 2% at the end of 2016 — three percentage points less than before the financial crisis.

Another reason for Fed chair Janet Yellen to go slow: The recent stock market sell-off and the slowing global economy which have complicated matters — and led to a chorus of warnings that the Fed should leave rates alone.

"Moderately rising interest rates are not bad news for stocks," says Chris Cook, president of Beacon Capital Management. "It means the economy is doing better." Indeed, in past periods of slight rate increases since World War II, the S&P 500 has generated decent returns.

Nor is it disastrous for fixed income, even though bond prices fall when rates rise. "The majority of your total return comes from the yield, not price changes," says Cook. "If we don't have steep rate increases — and it looks as if that's not likely — then your rising income payouts will soon make up for any price drops."

Regardless of what the Fed does, here are steps to prepare your portfolio for uncertain times:

YOUR BEST STOCK MOVES

• Seek higher-grade companies

Financially questionable businesses benefited from low rates in a couple of ways.

Cheap capital encouraged investors to speculate in lower-quality names. Moreover, companies that must borrow heavily enjoyed cheap rates. As yields rise, though, highly indebted businesses will face headwinds. This gives an edge to companies with low debt and strong balance sheets, like those found in Power-Shares S&P 500 High Quality ETF .

Also, keep in mind that this is a mature rally in its seventh year, where growth "isn't expected to accelerate much," says Brad Sorensen, head of market and sector analysis for the Schwab Center for Financial Research. So now's the time to look for companies with a solid earnings outlook. Sorensen recommends focusing on places such as tech, where "there's potential for growth as companies reinvest in technology now that productivity has been flat," he says.

He also thinks health care — with the exception of small, speculative biotech stocks — looks promising, as it's a defensive sector where profits are growing faster than in the broad market. Where to find this mix? Money 50 fund Primecap Odyssey Growth has nearly two-thirds of its assets in health care and tech.

• Switch dividend gears

If you shifted into high-yielding stocks in recent years to boost your income, it's time for a new approach. Not only are those shares expensive, but high-yielding sectors like utilities are also likely to fall out of favor once bond rates rise, says Sorensen. Instead, go with companies that are financially strong enough to grow dividends over time.

• Don't retreat from the world

If the U.S. economy is so healthy, why bother going overseas? Here's why: In the eight most recent periods of rising rates, U.S. stocks lagged foreign developed-market shares 88% of the time and emerging-market equities 75% of the time. "U.S. stocks have had a great run since 2009, and we're now at a stage where we could see the passing of the baton to other markets," says Dan Morris, global investment strategist for TIAA-CREF.

YOUR BEST BOND MOVES

• Come out of the bunker

If in anticipation of rising rates you shifted into short-term bond funds, consider a return to a core, intermediate-term fund such as Money 50 pick Vanguard Total Bond Market Index .

For starters, Total Bond's 2.4% yield is 1.2 points higher than the payout for Vanguard Short-Term Bond Index. "With moderately rising rates, what matters is having a yield cushion to absorb the price drop," says James Kochan, chief fixed-income strategist at Wells Fargo Advantage Funds. Short-term funds paying 1% offer little defense.

Moreover, while short-term debt is affected by Fed hikes, longer-term bonds dance to the beat of the market. Since U.S. bonds already pay more than most foreign-government debt, global demand for longer-term U.S. debt should remain strong. That is likely to keep longer-term rates from rising too much as rising prices mean lower yields.

Be careful not to go too far out. Kochan recommends funds with durations of five to seven years. Duration measures an investment's sensitivity to rate changes. A one-point rise in rates translates to a 5% price decline for a fund with a five-year duration. Vanguard Total Bond Market's duration is 5.6 years. Beyond seven years, your fund's yield may not be able to offset price declines for several years.

• Reach for yield carefully

The returns for high-yield corporate bonds are driven more by the economic outlook than by interest rate changes. And since the Fed is about to hike rates because of the strength of the economy, the 5.4% yield of Money 50 fund Fidelity High Income may be enticing.

Remember that these bonds exhibit stocklike volatility in times of market stress. So if you carve out a 10% allocation, take it from your stock portfolio, not fixed income. Fidelity High Income lost nearly 24% in 2008, while an index of high-grade bonds rose 5%.