These 3 Couples Plan to Retire Early. Here's How They're Making It Happen

Ready to chuck your day job for a mix of travel, volunteering, and golf? About half of Americans hang up their work clothes between ages 61 and 65, recent research shows.

But if your retirement vision starts even earlier, it will take some serious advance planning to map out your route. (Be sure to read Money's Comprehensive Guide to an Early Retirement.) The following three families, who are at different stages of their careers, each have a dream of retiring ahead of schedule. We asked experts to spell out the smartest moves they can make now to make those goals achievable.

Hilary Ross-Rojas, 30, and Willy Rojas, 32

Live in: Arlington, Va.

Occupations: Director at a market research firm and engineering student

Total income: $93,000

Financial assets: $121,000 ($71,000 in retirement accounts; $50,000 taxable)

Like many of her peers, Hilary Ross-Rojas hopscotched through several jobs in her twenties. But unlike most young workers, she immediately signed up for whatever retirement plans her employers offered—and quickly started socking away at least 15% of her paycheck. "I'm always thinking very, very far ahead," says Ross-Rojas, now 30.

By contrast, her husband, Willy Rojas, has until recently been largely focused on the present. At 20, Rojas, frustrated by the lack of job opportunities in his native Bolivia, dropped out of college there and immigrated to the Washington, D.C., area. After a decade of working as a remodeling contractor, he decided to return to school to study mechanical engineering. Rojas, now 32, spends his weekdays attending college in Richmond and commutes back to Arlington on the weekends. "I was just a student in my country," he says. "I didn't know much about investments."

Now that Rojas has been married to Ross-Rojas for almost four years, he too is beginning to think long-term when it comes to his finances. The couple are looking to retire in their fifties so they can spend more time traveling together and even live abroad, perhaps volunteering in the Peace Corps.

But Ross-Rojas wonders whether the late start that her husband is getting on his career has put them behind on saving. Moreover, the couple are thinking about early retirement before they have even started a family. "We know kids will change our savings strategy, but we don't know how yet," she says.

PROGRESS REPORT

Milwaukee financial planner Kevin Reardon says that the Rojases aren't behind at all. "You are light-years ahead of your peer group," he tells the young couple. For starters, it is better to plan for early retirement before having kids, not after. He also notes that neither spouse has student loans or other debts. The couple opted to buy a modest fixer-upper home three years ago, using Rojas's construction skills to increase the value via sweat equity. And they're frugal.

ADVICE

Max out on savings while you can.

"There are definitely hurdles coming," Reardon says. "Childcare, college … the best-laid plans can get thrown to the wind later on." For instance, the couple currently spend about $30,000 a year, but day-care costs alone for one child would set them back $15,000 annually.

Before that happens, the couple need to power save. After Rojas finishes school next year and gets a job, Reardon says, he should immediately max out his tax-advantaged savings. Assuming he starts doing that in 2019, he could amass more than $700,000 by 55, assuming 6% returns and no company match. That's in addition to the roughly $2 million that Ross-Rojas is on track to save on her own.

Optimize tax savings.

Rather than putting all 15% of her current pay into her 401(k), Ross-Rojas should invest just enough—4%—to get the full employer match. Then she should maximize contributions to Roth IRAs before adding more to her 401(k). Why? Roth contributions are funded with after-tax dollars, and with Rojas still in school, the couple are in a low tax bracket. Once Rojas starts working, their bracket will increase; at that point, they should both max out their 401(k)s. An added bonus: Roth IRA assets can be used for educational as well as retirement needs, preserving flexibility down the road.

Ross-Rojas also started funding a health savings account last year, which she should keep doing. "For my clients who retire in their fifties, funding health insurance is a huge issue," Reardon says. "Your HSA is potentially as important as the 401(k) in the future."

For Rojas's tuition payment, the couple can also make use of Virginia's state tax deduction of $4,000 per person on 529 contributions, says Reardon, since they will qualify for the tax break even if contributions are withdrawn almost immediately.

Simplify and automate accounts.

Ross-Rojas has an old 401(k) and four Roth IRAs. She should consolidate them into a single IRA, says Reardon, and invest in a target-date fund that's 80% in stocks. She also should set up automatic deposits into her IRA. "You've done an amazing job remembering to write those checks," he says. "But as you go along, life can get pretty busy."

Dial back on cash.

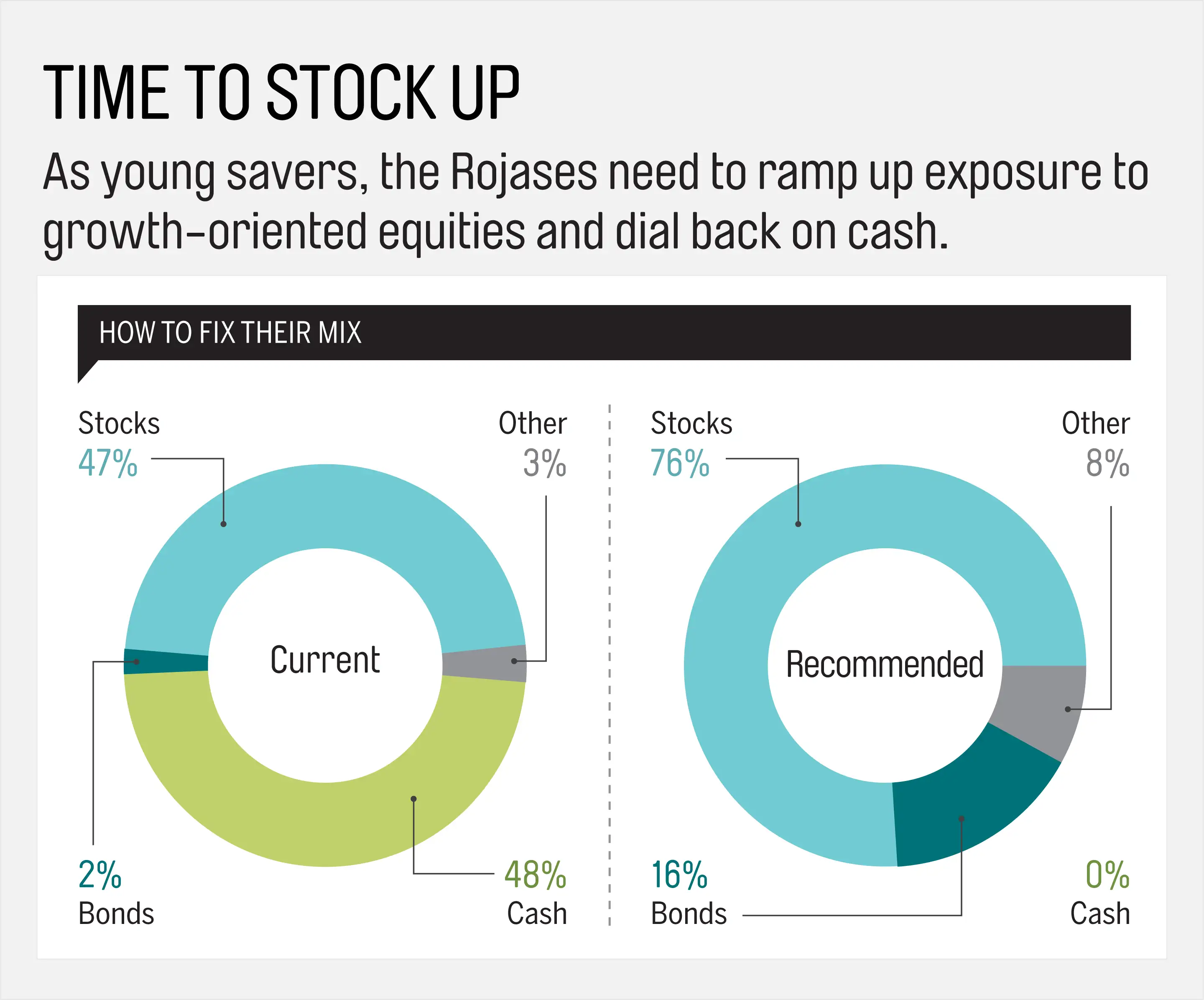

In their retirement account, the Rojases need to shift out of no-growth cash into faster-growing equities, which ought to represent most of their investments at their young age (see chart).

But the pair must redeploy cash elsewhere too. For example, $32,000 sits in a money-market account partly as an emergency fund and to add central air-conditioning to their home. Reardon says they should use $9,000 to cover the costs of tuition rather than taking out a student loan. Then get a home-equity line of credit to pay for the A/C renovation. "HELOC interest is tax-deductible, and the rates tend to be lower than student loans," says Reardon. "I'm not worried about you guys using your equity as a piggy bank."

Tim and Jennifer Eldredge, both 49

Live in: Aptos, Calif.

Occupations: Hospital sales rep and full-time mom

Total income: $140,000

Financial assets: $682,000 (not including more than $400,000 in home equity)

Tim and Jennifer Eldredge live in an area of the country known for its natural beauty. So it's not surprising that they would like to stop working within a decade or so to spend more time enjoying their great outdoors. There's just one problem—or rather three. They also want to cover the cost of college for kids Megan, 16, Holden, 14, and Jack, 11. And they have saved only $21,000 in 529 plans.

To help pay tuition, the couple have been contributing $50 a month to each child's 529 account for about six years, adding some extra on their birthdays. Unfortunately, that's left them far short of the $60,000 to $80,000 per child they figure they need. Says Tim: "It hasn't added up like we hoped."

PROGRESS REPORT

Though the Eldredges are behind on college savings, they have done a solid job saving for retirement, says Edina, Minn., financial planner Kathleen Longo. Tim, who works in pharmaceutical sales, recently upped his 401(k) contribution from 11% to 12% of pay (not including bonus); his firm matches 6%. Jennifer, who has been a stay-at-home mom for the past 16 years, puts the maximum $5,500 into a Roth IRA. Altogether they have $615,000 in retirement savings, plus another $67,000 in a taxable account.

Even though they live in an expensive area, the Eldredges are otherwise in good financial shape. They bought their current home two years ago, downsizing from a larger one nearby. Thanks to that move, they have about 50% equity in a house worth about $800,000. Tim's firm also provides excellent benefits, including a company car. Besides the mortgage, they have no other debt.

While retirement in their fifties is out of reach, they aren't too far off: "Your savings is on track to retire at age 60," Longo tells the couple. They should be able to cover about two-thirds of their current expenses after age 60, and Longo says their spending is likely to fall once the kids leave home. This also assumes Tim's plans to work part-time as a golf instructor, worth about $800 a month plus free course time.

ADVICE

Look for creative solutions for the kids' education.

"Given the age of their kids, the Eldredges are likely going to have to prioritize," says Longo. For instance, Longo suggests limiting their choices to cheaper schools or having the kids take on some loans. But Jennifer isn't keen on that idea. "We think it's really important for the kids to remain debt-free," she says.

Her compromise: To cut costs by almost half, the couple will have all the kids go to the local community college for two years, which runs just $4,000 a year. After that, they can transfer to a state university or private college. "I am willing to help them graduate from the best school they can get into," she says.

Jennifer adds that if need be, she's willing to start working, perhaps even full-time, to help pay for tuition. But Longo notes that even though college costs will loom large over the next five to 10 years, the couple shouldn't lose sight of growing their nest egg.

Make full use of catch-up contributions.

The Eldredges can have more flexibility in spending if they raise Tim's 401(k) contributions closer to the $18,000 annual limit, up from about $14,000 today. Longo suggests gradually adding more with each raise and using some of his quarterly bonuses as well.

Once they turn 50 this year, they should also make catch-up contributions, which will allow Tim to put another $6,000 in his 401(k) and Jennifer to add an extra $1,000 to her IRA. Combined, this extra savings could amount to nearly $150,000 more by quitting time at 60.

Fix their investment mix.

Tim's 401(k) is simultaneously too risky and conservative, says Longo. Ten percent of his savings is in company stock, which is too much, especially since his livelihood also depends on the success of the firm. Beyond that, he owns several target-date retirement funds in his account, all of which have different retirement dates. Collectively, they give the couple's overall portfolio an average of 69% in equities. Longo suggests dropping the fund with the nearest retirement date—with only 60% in stocks, it's too conservative anyway—and consolidating to a single target-date fund with a 70% to 80% stock allocation. Jennifer should hold a target-date fund in her Roth IRA with a similar 80% stock/20% bond mix.

Increase insurance protection.

The Eldredges have no wills or health care directives, and they're underinsured, threatening their plans in an emergency. In addition to a small life insurance policy through his employer, Tim is also paying $179 a year for a second, restrictive policy covering accidental death. Jennifer has no insurance.

Longo suggests Tim drop the secondary coverage and use the funds to offset the costs of 10-to-15-year level-term life policies for both Tim and Jennifer—enough to cover them until they retire early.

Bob and Teresa Jacobson, 49 and 50

Live in: Las Vegas

Occupations: Senior program director for a carpenters' union and IT manager

Total income: $230,000

Financial assets: $840,000 (not including $460,000 in home equity)

Bob and Teresa Jacobson are living the good life in Las Vegas. Originally from Chicago, the couple relocated to Sin City about five years ago for Bob's work. Today they're living in a 5,000-square-foot home, eating out at least five nights a week, and traveling for long weekends to visit far-flung family. "I don't miss the snow at all," says Teresa.

The Jacobsons also enjoy their work life. Bob, 49, serves as a program director for the United Brotherhood of Carpenters union, and Teresa, 50, is a manager in the information systems division of a shipping company. Nevertheless, Bob and Teresa, who have no kids, have long thought of age 55 as a retirement date to shoot for.

Fueling that dream is the knowledge that Bob qualifies for generous pension plans that he can start tapping at that age. Further bolstering the case for retiring ahead of schedule: Bob and Teresa can also continue to be covered by Bob's employer's health insurance after they retire—though at a higher cost.

Once they retire, the Jacobsons would have the time and freedom to travel even more, including trips farther abroad. They would also like to spend more time pursuing outdoor activities such as hiking and golfing. To make that happen, they're willing to downsize from their spacious house to a smaller townhouse, which would eliminate their mortgage payments and free up cash.

What they don't want is to have to resort to belt-tightening to make their retirement dreams come true. "I think we're in a pretty good place, but what can we realistically withdraw?" asks Bob. "If the number falls short of being as active as we want to be … I don't know if we'd be happy with that."

PROGRESS REPORT

The Jacobsons can retire before 60, says Boulder certified financial planner Judy McNary. But to figure out how many years before, they must get a grip on their budget. "You know that, coming and going, you feel comfortable, but there's no real target or focus on spending," she says.

Right now the Jacobsons think they'd need $100,000 to $120,000 a year in retirement, not counting their mortgage. If they can stick to a $100,000 annual budget, they should be okay to stop working at 55, says McNary, who calculates that the odds of their money lasting throughout their retirement is nearly 90% based on that spending level. But what if they want to spend a little more?

ADVICE

Work just a little bit longer.

The Jacobsons can still have their cake and eat it too—just think about working a mere year past their target of 55, McNary says. "Even just one extra year buys you a lot," she notes (see chart below). Teresa says she'd be fine working a bit longer. "I'm not streaking for the door just yet," she says. Bob is less sure. "I would like to be completely done with it," he says. "And her one rule is that she won't work a day longer than me."

Wait to tap one pension.

Bob is eligible to start tapping pensions from two different employers at 55. One will provide nearly 50% of his current income. The smaller pension would pay nearly 25% of his salary if he takes it at 60, but he'd be penalized 5% for every year he takes it earlier than that age.

To buy them time, the couple should tap additional savings and allow that pension to reach its max, says McNary. That's because it's effectively a 5% guaranteed return that they may not get on their investments. Similarly, the couple should hold off tapping Social Security benefits until they reach the full retirement age of 67.

Scale back on stocks.

The Jacobsons' portfolio is 90% in equities. Bob says that was by design. He deliberately chose to have greater exposure to growth-oriented investments, knowing that he has the security of a pension. Plus, "seeing bonds just sitting there makes me antsy," he says.

But the point of holding bonds in a retirement portfolio isn't to provide return, says McNary—it's to dampen volatility and protect against losses. And 90% is way too much for a couple who will need to start tapping that nest egg within five years or so, says McNary. "Stocks have had a nice run, but as you get towards retirement, you need the protection of bonds."

She suggests a 60% stock/40% fixed-income mix, diversifying across different asset classes including large- and small-cap U.S. equities, international shares, real estate investment trusts, and short- and intermediate-term bonds. The worst one-year loss for a 60/40 mix is a drop of around 25%, vs. about 40% for a strategy with 90% or more in stocks.

Decide on survivor benefits.

When he takes his pensions, Bob must choose whether to get survivor benefits for Teresa. On the larger pension, that would subtract about $1,000 from his monthly payment.

He needs to provide protection for Teresa should he die first, but there may be a cheaper way, says McNary. If he remains in good health, it may make sense for him to buy a 25-year level-term life insurance policy, which could cost as little as $300 a month.