How to Stop the Next Housing Bubble

- Jack Bogle, Who Revolutionized the Way Millions of Americans Save and Invest, Dies at Age 89

- Why Trouble in China is Hitting Your 401(k)

- Why China's Currency Has Been Knocking Down U.S. Stocks

- Jack Bogle Explains How the Index Fund Won With Investors

- What Happens If the Social Security Trust Fund Runs Out in 2034?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

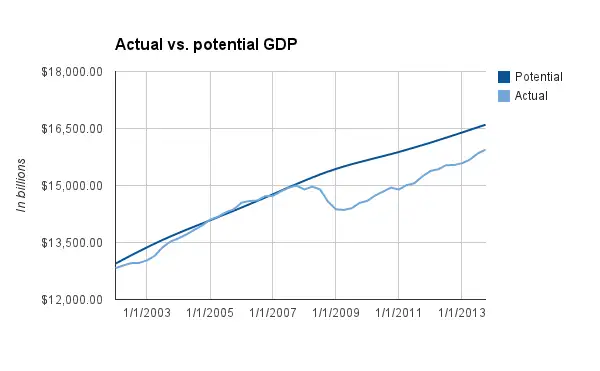

More than five years after the Lehman Brothers collapse, America still has a bubble problem.

The economy is improving, but the country is still poorer and less busy than it should be this long after the official end of the Great Recession. Here's where actual GDP lines up against where it might be if the economy had returned to its normal path:

Despite this gap, the Fed last week announced it was continuing to slow down its massive program of bond buying known as "quantitative easing," which was designed to ease lending and goose the economy. The central bank is keeping short-term interest rates near zero, but many economists and economic pundits still think the Fed should be even more aggressive, rather than slightly less so. The Fed holds back mostly out of fear of inflation (which remains low) but another worry has emerged: Investors are getting cocky. Stocks are way up, bond investors are buying riskier stuff in a "reach for yield," and yet a gauge of market mood called the "fear" index is registering an unusual lack of anxiety.

The Fed has expressed concern, at least in a keeping-it-on-our-radar way. "There is some evidence of reach-for-yield behavior," said Janet Yellen on Wednesday in a press conference.

That doesn't mean we're in bubble territory. Even if a market drop is coming, there's a difference between that and a systemic crisis like 2008's; Yellen said she isn't seeing a rise in dangerous financial leverage. But that we're even having this conversation is a sign that there is a lot of unfinished business left over from the crisis. There's still too much risk built into the financial system.

This story is the first in a series I'll be writing for Money.com about ways to prevent future bubbles—or at least to limit the damage when they pop. There are numerous pieces to this puzzle. Banking regulations, consumer protections, Fed policies, and broad-based economic growth are all important for a healthy financial system.

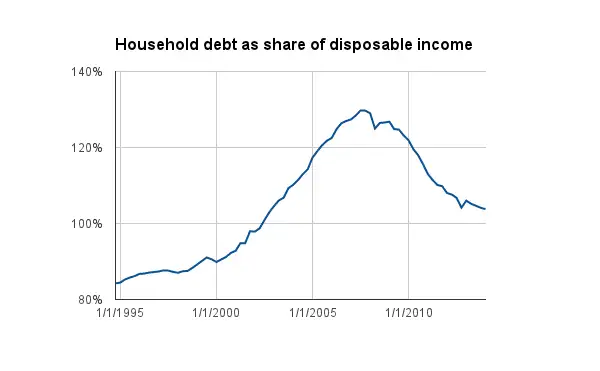

But the most obvious place to start is literally close to home: Mortgages. The 2000s saw an enormous build up in household debt, largely driven by home loans.

A lot of attention has been paid to how crazy a lot of those mortgages were. There were "NINJA" loans (no income, no job or assets), no- or low-downpayment mortgages, and exploding ARMs that started with low teaser payments. Such loans are impossible or at least very hard to get now. But a pair of fascinating new books make the case that there's still a basic flaw in how mortgages work, one that Washington had a golden opportunity to fix but failed to. Put simply, home loans are far too difficult to renegotiate when things go badly wrong.

Over the years I've read a tall stack of books about the financial crisis. Other People's Houses, by Vermont Law School professor Jennifer Taub, provides the clearest, beginning-to-end explanation I've seen of what went wrong. And Taub's beginning is a surprise: A 1993 Supreme Court decision about how bankruptcy law applies to mortgages.

A mortgage on your primary residence is different from other kinds of loans–and not in a good way. When a borrower is buried in bills, the bankruptcy process can help discharge many kinds of debt. In the early 1990s, Harriet and Leonard Nobelman found themselves underwater on a condo in Dallas—they owed more than $65,000, but the current market value had fallen to $23,500. As part of a bankruptcy plan, they proposed that the balance of their mortgage be reduced to that $23,500. The bank fought this in court. Ultimately, the Supreme Court decided that the principal value of a mortgage can't be modified by a judge in the bankruptcy process.

Fast forward to 2008 and the housing crisis, and this technical-sounding decision suddenly mattered a lot. Candidate Barack Obama endorsed changing the bankruptcy law, but ultimately nothing ever came of it. And the administration resisted other proposals—coming from political conservatives as well as liberals—to encourage or push lenders toward principal reductions. (A program to subsidize some principal mods began in 2010.)

"Hang on," you may be saying, "forcing people into bankruptcy doesn't sound like much a solution. I know lots of people who went underwater on their home, and they never would have declared bankruptcy."

That's true. But Taub tells me that that this law matters even for those who never go to court. "It would have shifted the bargaining power," she says. "Knowing that would be an option would have brought the lender to the table more quickly and more willingly."

Of course, many underwater homeowners ultimately did get out from under their debts—by letting the bank take the house, or agreeing to a short sale and moving out. But could a more orderly, less painful principal reduction process have made the housing crisis less damaging?

Economists Atif Mian of Princeton and Amir Sufi of the University of Chicago say yes. Their book House of Debt argues that the Washington's failure to help more homeowners renegotiate their debt needlessly prolonged the economic slowdown.

When households are weighed down by debt they can't pay, they spend less, and the effect can spread throughout the entire economy. This seems intuitive, but most economists have preferred to focus on fixing broken banks. Mian and Sufi have found compelling evidence that homeowners' woes were the real main event. For example, in U.S. counties with the sharpest declines in net worth during the crash, spending fell almost 20%.

Much of this is water under the bridge now. But not all of it. Taub points out that foreclosures are up over last year in some states. In any case, she argues that resetting the rules for how mortgages work could help to prevent the next bubble. "Hopefully, lenders, if they are disciplined by having to take losses, won't engage in these no-money-down and no-doc mortgages and so on," she says.

Letting off the hook people who borrowed too much is touchy stuff. (See Rick Santelli's famous CNBC rant.) But if borrowers should be more cautious, so too should lenders. Although putting more risk on lenders might raise the cost of mortgages somewhat, Taub argues "that's reasonable insurance to pay to avoid massive foreclosures and abandoned houses and the whole downward spiral." You didn't need to have an option ARM on an oversized house to feel the pain of the foreclosure crisis.

Mian and Sufi have another proposal for future mortgages that bypasses these hot-button fairness questions. A new kind of loan, called the "shared responsibility mortgage" could link mortgage payments to an index of local housing prices. If local prices fall, a borrower's monthly nut would drop too. In return, the bank would get 5% of any capital gains on sale. The idea is both to ease the economic damage housing declines cause, and to give lenders an extra incentive to be careful about lending into frothy markets. (The tax code would likely have to be changed to make such loans popular.)

As Mian and Sufi point out, mortgages looked like a pretty safe investment from the point of view of lenders. That was a big part of the problem. Even if housing prices fell, lenders assumed homeowners would be obligated to make their full payments. But the economy as whole would have been safer if more of the risk was shared.