Janet Yellen's Guide to Investing

- Jack Bogle, Who Revolutionized the Way Millions of Americans Save and Invest, Dies at Age 89

- Why Trouble in China is Hitting Your 401(k)

- Why China's Currency Has Been Knocking Down U.S. Stocks

- Jack Bogle Explains How the Index Fund Won With Investors

- What Happens If the Social Security Trust Fund Runs Out in 2034?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Janet Yellen, chair of the Federal Reserve, is testifying before the House of Representatives today. Yesterday, she spoke to the Senate. Her testimony is accompanied by a deeper-dive document called "The Monetary Policy Report."

One snippet caused a stir yesterday, because the Fed lays out a fairly detailed view of valuations in the markets. The Reformed Broker blog quipped that it sounded like a report from a portfolio manager at "Yellen Capital Partners". The big news was that the Fed thinks prices for some biotech, social media, and other small companies look "stretched." That's a polite way of telling investors: watch out.

But the Fed's full take on the markets is worth a look. Here's what the bank says -- feel free to skip ahead if you prefer to read Fedspeak in translation -- and what it means.

"Some broad equity price indexes have increased to all-time highs in nominal terms since the end of 2013. However, valuation measures for the overall market in early July were generally at levels not far above their historical averages, suggesting that, in aggregate, investors are not excessively optimistic regarding equities."

A standard way to look at whether stocks are cheap or expensive is to compare prices on the S&P 500 index to companies' earnings. If you use the profits Wall Street analyst's estimate for the coming year, prices look high relative to the past decade, but a long way from the tippy-top prices of the late-1990s bubble.

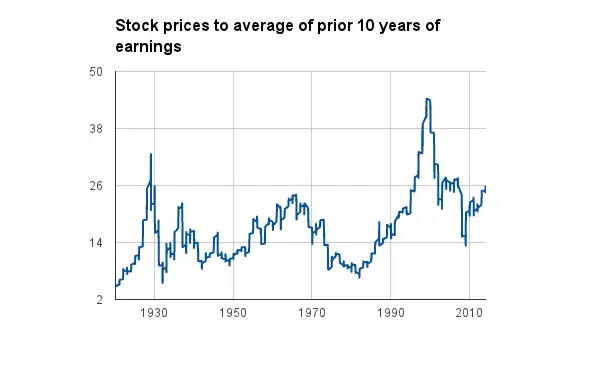

People with a more bearish take on the market prefer to look at stocks relative to the past 10 years of actual earnings. This smooths out times when earnings are unusually high, and cuts out Wall Street analysts' optimism. It also allows you take a longer view. Again, stocks look expensive compared with recent years, less so compared with the peak… but quite high relative to a longer history.

The Fed's saying stocks are on the expensive side, but not crazily so.

"Valuation metrics in some sectors do appear substantially stretched—particularly those for smaller firms in the social media and biotechnology industries."

There was much talk of a biotech bubble earlier this year, and those stocks have been volatile ever since. They're still way ahead of the S&P's big gains in recent years. As Business Insider noted back in March, new biotech IPOs are popping up all over. There were 24 in the first quarter of this year and 37 least year, compared with just 11 in 2012. That can be a sign that investors are throwing their money at anything in hopes of getting that one big lottery ticket stock.

As for social media: This.

"Credit spreads in the corporate sector have also declined, on balance, in recent months… Credit spreads on high-yield corporate bonds are near the bottom of their range over the past decade."

We're talking about bonds here. High-yield is the nice way of saying junk bonds with poor credit quality and a higher risk of default. I bet if Janet Yellen is worried about anything, it's bonds more than weird social media IPOs. Investors who take a plunge on small companies with a new app usually know going in that they could lose money fast.

That's not always the case with bonds. As investors have searched for more ways to get yield, they've been pouring money into "unconstrained" and "nontraditional" bond funds, many of which hold lower grade debt. That may help investors if interest rates go up, but it also means taking on other kinds of risks. Some analysts, like Eric Jabcobson at Morningstar, worry that not all fund investors know the risk they are taking on. Unpleasantly surprised bond-fund investors can make a lot of trouble: In a worst-case scenario, if they all run for the exits at once, fund managers may end up having to fire-sale less-liquid bonds, or sell their higher quality bonds to meet redemptions. That would amplify a bond bear market, which in turn would mean tighter lending conditions all around.

But the Fed isn't painting a worst-case scenario here. They're just saying they are watching this data point.

The big question: What business is it of the Fed's what people invest in?

Like it or not, communicating with markets is a big part of what central banks do. It used to be said that British banks were regulated merely by a raised eyebrow from the governor of the Bank of England. Janet Yellen is giving the markets a little bit of an eyebrow raise here. The Fed's main jobs are getting unemployment down and keeping prices stable, but especially after 2008, it worries about asset bubbles too.

Yellen may also be shaking the tree a little. The Fed doesn't see a whole lot of bubbly behavior, but it also knows it can't see everything that's going on in every corner of the financial system. Blogging economist Tyler Cowen has a theory that Yellen's talk about certain investors getting kinda complacent is really a way of finding out if that's true. If the Fed says biotech stocks are a little high, and then investors take a closer look at their biotech stocks and decide to run away… well, maybe biotech stocks really were getting too high.

But let's not forget the context in which Yellen is raising her eyebrow: Her Fed is still doing Quantitative Easing, though it's likely to end this fall, and still holding short-term interest rates near zero. In other words, she's still telling the financial markets that the Fed will keep stoking economic growth; the report just tempers that message a bit.

Yellen is saying, in effect, "We've still got your back -- but don't come crying to us if you go making crazy bets."