Boomers Take a Lot Out of Social Security and Medicare, but Millennials Will Use Them Even More

It's become a cliché that young people expect to get nothing out of the Social Security and Medicare system.

But a new report from the Urban Institute says that if government continues to pay its current commitments, a married millennial couple stand to receive roughly twice as much as their parents got. On average, the young couple will get $2 million in Social Security and Medicare benefits, adjusted for inflation, during their lifetimes.

And this won't just be money paid back to them: It will be nearly double what the couple contributed over their lifetimes in payroll taxes.

Increases in Medicare payments, which are driven by rising health care costs, are responsible for most of the projected rise. Two other factors: Millennials, defined as people born between 1981 and 1997, will earn more in wages than their parents, and Social Security benefits automatically increase to keep pace with wage gains. Plus, today's young people will live longer than their parents, meaning they'll have more years to collect both Social Security and Medicare benefits.

The Urban Institute report, written by by C. Eugene Steuerle and Caleb Quakenbush, brings attention to the gap between what people are paying into the Social Security and Medicare system, and what they are taking out.

This benefit-payment gap isn't new. It was $440,000 over a lifetime for a couple turning 65 in the year 1980, and $355,000 for a couple hitting that age this year. It will grow to $518,000 for couples turning 65 in the year 2030, and $887,000 for a 30-year-old couple turning 65 in 2050.

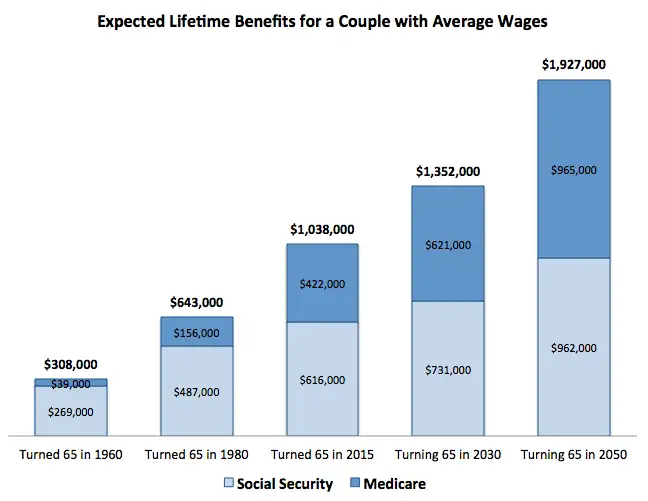

Here is a look at actual and projected lifetime benefits for couples earning average wages ($49,000 this year), based on the year they turned (or will turn) 65:

Projected high benefits might appear to reassure younger Americans that they will enjoy a strong federal safety net in their later years. But rising costs and program funding deficits could raise pressure on Congress to cut these benefits—especially if it proves difficult to rein in health-care costs. Even if this does not come to pass, Steuerle says in an interview, he does not see how we can avoid cutbacks in other government programs that will harm all younger generations.

“We know the system is not sustainable as it is now,” he says. “For millennials, the problem is that the longer we delay [needed changes] the more we put the burden on younger and future generations.”

Outside of Social Security and Medicare, such impacts could include reduced education support, lower child tax credits, less spending on infrastructure needs, and other cutbacks that would disproportionately hit younger Americans.

“It’s a crazy system,” argues Steuerle. “Is this really how millennials would want to design the system if they had the chance? We put all our [spending] support and leisure time for them at the end of their lives, and all their expenses up front.”

Creating a more level pattern of government supports during their lifetimes, he says, could take pressure off of federal spending, improve living standards for younger Americans, and still provide adequate Social Security and Medicare benefits to them during their later years.

Philip Moeller is an expert on retirement, aging, and health. He is co-author of The New York Times bestseller, “Get What’s Yours: The Secrets to Maxing Out Your Social Security,” and is working on a companion book about Medicare. Reach him at moeller.philip@gmail.com or @PhilMoeller on Twitter.