Why Big Oil Can Withstand Cheap Oil Prices

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

The price of oil dropped dramatically in the second half of last year, resulting in less-than-stellar earnings for some of the world's biggest energy companies. Exxon Mobil, BP, and Royal Dutch Shell all recently produced underwhelming fourth-quarter results thanks to lower demand for, and excess supply of, oil.

Despite recent struggles, investors have not jumped ship, and the petro-behemoths have outpaced the broader stock market over the past week. What's going on, and what does this mean for you?

Oil Companies Have Lots of Money

The last three months of 2014 were not pretty for oil producers. The value of a barrel of oil hit around $115 in June, fell to $55 by the end of the year, and recently dropped to $45 before rebounding in the last couple of days. Exxon's revenue dropped 21%, BP posted a replacement-cost loss (which is akin to net income) of $969 million, and Shell only saw gains thanks to ancillary businesses.

Despite the recent price uptick, oil's outlook isn't much better. The U.S. Energy Information Administration expects the price of oil to average $58 a barrel in 2015, compared to $109 just a few years ago. Lower oil prices simply makes it harder for major energy conglomerates to make money.

Fortunately for executives in Irving, Texas, London, and The Hague, however, large integrated oil and gas companies tend to have a lot of capital to soften these blows. Even after enduring a rough quarter, Exxon has nearly $5 billion in cash on hand, BP earned more than $12 billion for all of 2014, and Shell took in about $45 billion in cash flow last year.

Oil Companies Have Other Businesses

While cheaper oil makes the act of getting the black stuff out of the ground less profitable, other businesses in these large oil companies actually stand to benefit from lower oil prices. Exxon's chemical operations, for example, actually saw a 35% increase in earnings over the same period in 2013.

"Our chemical business is very well positioned to take advantage of the lower commodity prices," says Exxon's head of investor relations Jeff Woodbury in the most recent earnings call. "Particularly in the U.S. our manufacturing sites are highly flexible and can run across a wide range of feedstocks, from ethane all the way to gas oil."

It's About Expectations

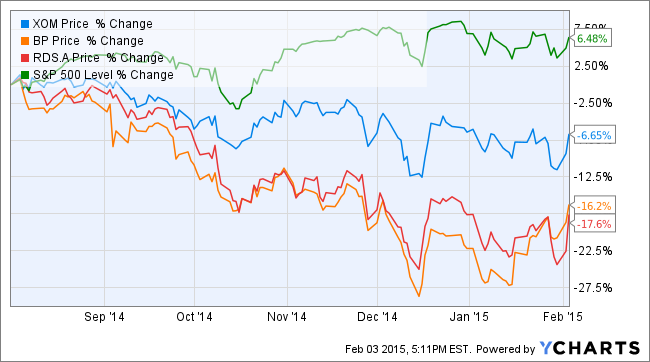

Falling energy prices was one of the biggest stories at the end of last year. Americans are feeling better about their own financial situation; cheaper prices at the pump feel to them like a pay raise or a tax cut. Which is to say, the market was not shocked that large oil companies had muted earnings during the last three months of 2014. In fact over the past six months shares of Exxon, BP, and Shell have fallen 6.7%, 16.2% and 17.6%, respectively. (The S&P 500, over the same period of time, has actually jumped 6.5%.)

And oil executives are doing all they can to lower costs and expectations for the near future. BP announced that it will be spending $4 to $6 billion less in capital expenditures in 2015 than it originally thought, and about $3 billion less than the company spent last year.“We have now entered a new and challenging phase of low oil prices through the near and medium term,” BP chief executive Bob Dudley said in a press release. Shell has also announced that it will reduce costs next year, and expects to spend $15 billion less through 2017.

What Does This Mean for You

Investors still pay a premium to own big oil stocks. Forward-looking price-to-earnings ratio for Exxon, BP, and Shell all exceed that of the S&P 500.

But they still look relatively attractive to USAA fund manager Bob Landry. Oil prices may not rebound this year, he says, but they've probably hit a floor at around $40 a barrel. "If you're a long-term investor you can hold some of these companies that pay a solid dividend, and pick up shares for cheaper than what they were four-to-six months ago," Landry says. "These companies can survive this turmoil thanks to a fortress balance sheet and the ability to generate significant cash flow."