How to Master the Medicare Maze

ILLUSTRATIONS BY JOHN TOMAC

MEDICARE IS "complicated and often opaque and impenetrable," says Money contributor Philip Moeller, co-author of the bestseller Get What's Yours: The Secrets to Maxing Out Your Social Security. That's a shame, given the impact Medicare—the health insurance program covering more than 95% of Americans 65 and older—can have on your life. Medicare households spend 15% of their budget on health care, reports the Kaiser Family Foundation, compared with the U.S. average of 7%. The wrong coverage or a missed deadline can not only cost you thousands but also threaten your health.

To guide you through the morass, Moeller has written Get What's Yours for Medicare: Maximize Your Coverage, Minimize Your Costs, due out on Oct. 4. In the book, Moeller walks you through the system's many complexities, including sign-up windows, coverage options, and provider quality.

Below are five key pieces of advice drawn from Moeller's new book. They'll help you save money while ensuring you get the quality care you deserve.

Know Your True Deadline

Signing up for medicare can cause a major brain freeze. The circumstances under which you do or don't need Medicare at age 65 are often unclear. And you face potentially harsh financial penalties if you get the decision wrong.

Let's say you are 65 or older and are covered by a current employer's group health insurance policy, either through your own job or your spouse's. In most cases you don't have to sign up for Medicare. Only once your or your spouse's coverage as an active employee ends does the clock start ticking. You have eight months after that to sign up for Medicare.

As is the case for people who sign up for Medicare at 65, you generally enroll in Part A (primarily for hospitals and other inpatient treatment) and Part B (doctors, outpatient treatment, and medical equipment). You usually must have those before you apply for other Medicare policies, like Part D, which covers prescription drugs.

Not everyone who has employer-provided health insurance when turning 65, however, can skip getting Medicare. Watch out for some very important exceptions to the rule.

SMART STEPS

Does your employer have fewer than 20 employees? Then you have to get Medicare when you turn 65, since at these small businesses Medicare automatically takes the role of what's called the "primary" payer of your insurance claims. Employer insurance moves to the backseat as the secondary payer of claims, helping defray expenses not fully covered by Medicare, including deductibles, co-pays, and co-insurance.

Another exception is if you have a retiree health plan from an employer that insured you or your spouse as a worker. As indicated above, you have to be in an active employer group plan to belong to the "don't need it" club.

You also don't get a pass if you have health insurance under the COBRA law, which allows people to stay on their employer's health plan by paying not only their employee premium but also costs previously picked up by their employer. If you go on COBRA when you're 65 or older, or are already on it when you turn 65, the clock can start ticking on your Medicare enrollment obligations.

In all these situations you could be on the hook for various financial penalties, starting with a 10% higher monthly premium—for life—for each full year you are late signing up for Medicare Part B.

Worse, perhaps, is that you might be living with no primary health insurance at all. In many cases you won't even know this until you get the bill for medical expenses. Pray that they are minor.

You could be on the hook for various financial penalties, starting with a 10% higher monthly premium—for life.

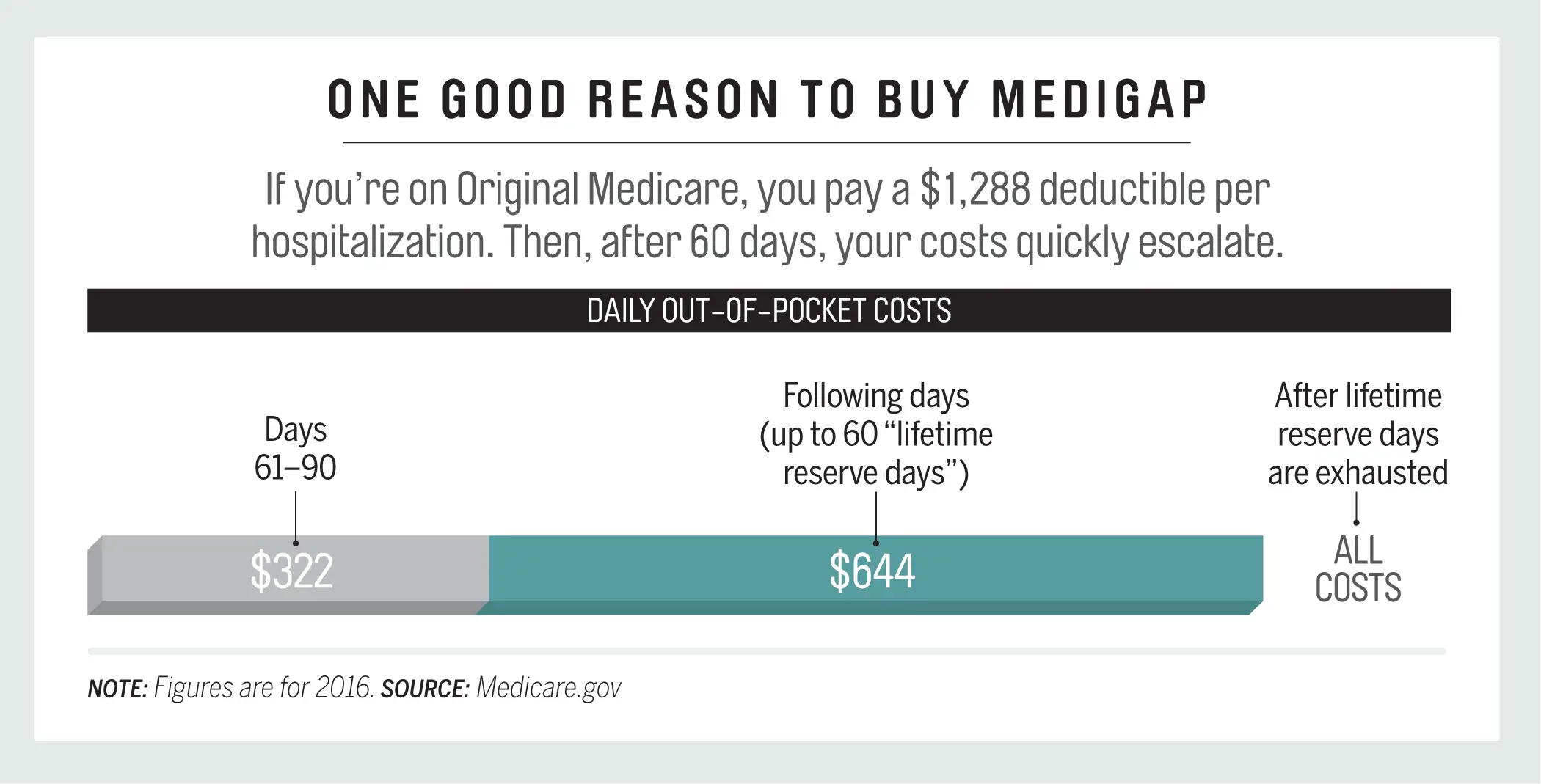

Fill Gaps with Medigap...

Medigap policies, also known as Medicare supplement plans, are private insurance plans that fill coverage gaps that can leave people with Parts A and B—also known as Original Medicare—vulnerable to enormous expenses. Part B, for example, generally pays only 80% of the cost of covered services and medical equipment. You pay the other 20%.

There are 10 standard Medigap policies that can be sold by insurers, designated by different letters of the alphabet, from A through N. Coverage varies by letter; for example, only some of the policies (C, D, F, G, M, and N) pay for emergency medical needs during foreign travel, which Original Medicare does not do.

What all Medigap plans cover is 100% of Part A co-insurance and hospital costs up to an additional 365 days after Medicare benefits are exhausted. Should you have Original Medicare but not Medigap, an extended hospital stay could cost you dearly. This single Medigap feature would save just about everyone from the poorhouse.

Medigap policies offered by any insurer must include exactly the same coverage as the same-letter plans offered by other insurers. Insurers are free, however, to charge different prices for the same-letter policies. And they do. The Kaiser Family Foundation reported in 2013 that the monthly premium for Plan F, the most popular, ranged from about $155 to $197 across most states.

Smart Steps

Because of the variability in premiums, comparing prices when you shop for Medigap is essential.

Also, once you have secured Part A and Part B coverage, you normally have six months of guaranteed access to Medigap. Insurers must sell you any plan they offer that you want; they can't refuse to insure you because of preexisting conditions, and they can't nail you with higher premiums because of those conditions. Also, the Medigap policy is guaranteed to be renewable on these terms as long as you keep up your premiums. These guarantees may go "Poof!" if you miss your enrollment window.

...Or Find a Medicare Advantage Network

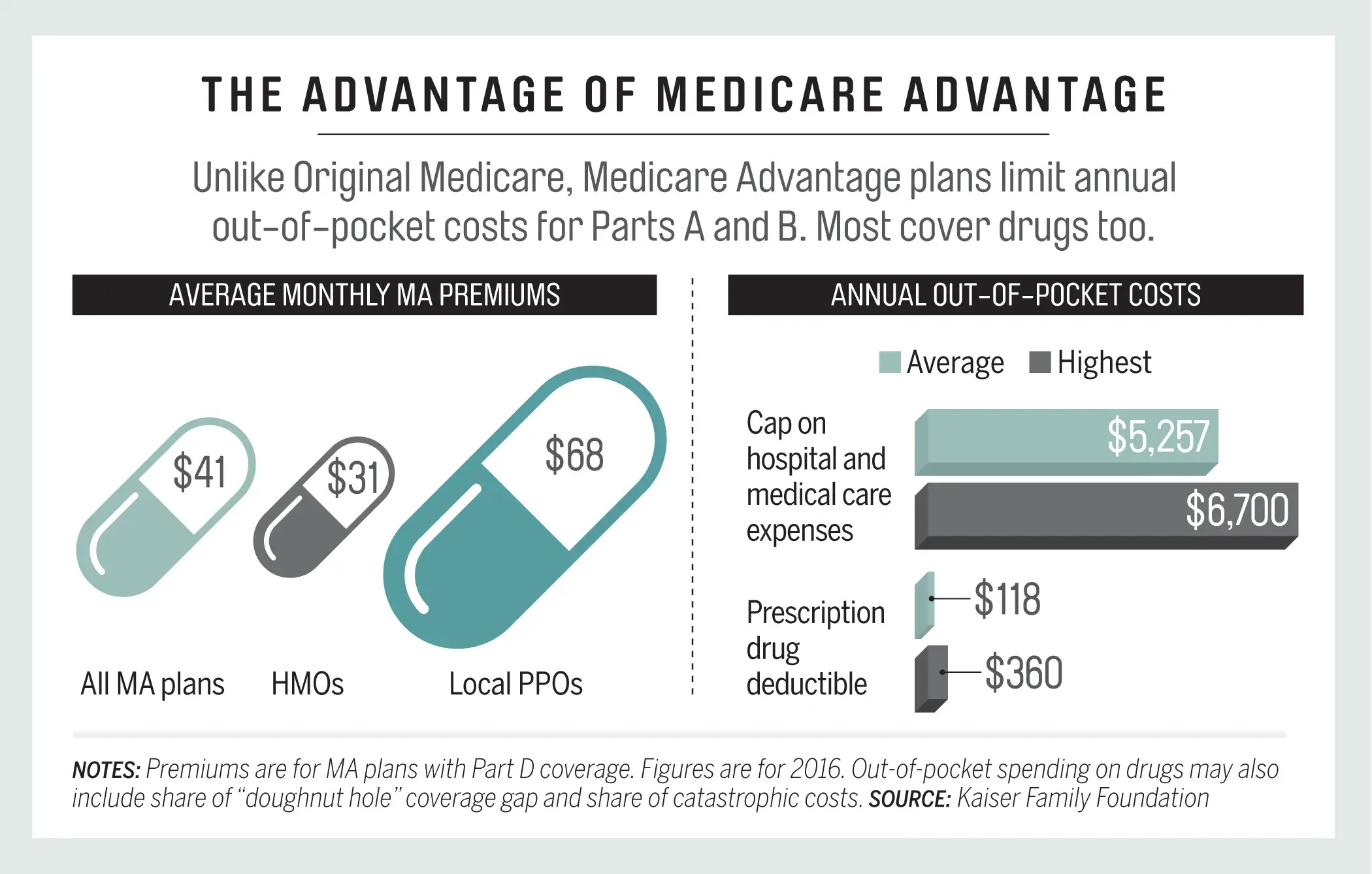

As an alternative to the fee-for-service Original Medicare (with stand-alone Part D for drug coverage and a Medigap plan), one-third of Medicare recipients have chosen Medicare Advantage plans, which have surged in popularity over the past decade.

Available from private insurers, MA plans are simpler to buy and use than Original Medicare and usually end up costing less, even though their premiums come in addition to Part B premiums instead of replacing them. Most are sold with Part D prescription-drug coverage built in, and many include dental, hearing, and vision coverage, which aren't covered by Original Medicare or Medigap. Although Original Medicare has no cap on annual out-of-pocket expenses (unless you have Medigap), MA plans do limit your maximum exposure. What's not to like?

Medicare Advantage plans are simpler to buy and use than Original Medicare and usually end up costing less.

Here's the catch: If you're on Original Medicare, you can use any care provider that accepts Medicare patients—and most do. MA plans, by contrast, usually require members to use only the providers within a plan's network. The plan picks the doctors, hospitals, and other key health care providers you can see. If your doctor and preferred hospitals are in the network, terrific. If not, you'll pay higher out-of-network fees or full price.

About two-thirds of MA plans are health maintenance organizations, most of which make you get all your services in their networks (except for emergency care and out-of-area urgent care). Your primary physician coordinates your treatment and is the gatekeeper for any referrals you might need. This is generally the cheapest type of MA plan.

Read: 3 Burning Questions About Clinton's Gigantic Medicare Proposal

Most other MA plans are preferred provider organizations, which offer you broader access than HMOs to doctors and hospitals outside their networks. You usually don't need referrals from your primary physician. As is the case with HMOs, if you want Part D drug coverage, you must purchase it bundled with your MA plan; you can't buy it separately.

Smart Steps

You should not—repeat, not—buy an MA plan unless your doctor and other preferred providers are in its network (or you're willing to switch to providers who are). You may not know whether a doctor is, but he or she will. Or more accurately, the doctor's office staff will.

Also, are you a snowbird living in more than one place in the U.S. over the course of the year? Fee-for-service Original Medicare with Medigap may be better for you because you can take your coverage with you. This may not be possible with a Medicare Advantage plan tied to a local network of providers.

Prepare to Reverse Course, If Necessary

Many people believe that once you have Medicare, you will need to keep it for the rest of your life. Not true. And it's especially not true in today's economy, in which people are regularly moving into and out of the labor force after they turn 65.

Let's say you're over 65, happily retired, and on Medicare. Then one day you land a great job with benefits that include a very good health plan.

If you are actively employed and you can be covered on your employer's group health insurance, you can drop Medicare without facing a penalty when you re-retire and sign up again. The same is true for your spouse, if he or she is covered by your new plan.

Read: The Hidden Risks of Those Popular Medicare Advantage Plans

SMART STEPS

Because dropping Medicare is such a serious decision, the government makes you have a personal interview with a Social Security representative before you can fill out the necessary form. To get started, you'll have to make an appointment with Social Security, which handles Medicare enrollment. Find contact information at ssa.gov/locator.

One caveat: Your ability to drop Part D prescription drug coverage hinges on the drug coverage included in your employer plan being what's called "creditable." That's an important code word in Medicare meaning that the provided coverage is as good as, or better than, typical Medicare drug coverage. Your employer should have this information.

Revisit Your Drug Plan Again and Again

Part D prescription-drug plans are voluntary. But voluntary or not, if you are late in enrolling for a plan—if your coverage doesn't kick in within two months after your deadline for enrolling in Part B—you may be hit with lifetime penalties. For each month you're late, a 1% fee is tacked on to your basic Part D premium. So sign up four years late and you're facing a 48% markup every month for the rest of your life.

Once you get Parts A and B, you have two pathways into Part D. You can buy a stand-alone plan, often called a PDP. Or you can get a Medicare Advantage plan bundled with Part D—most MA plans are packaged that way—usually abbreviated as an MA-PD plan.

Calculator: Social security retirement income estimator

SMART STEPS

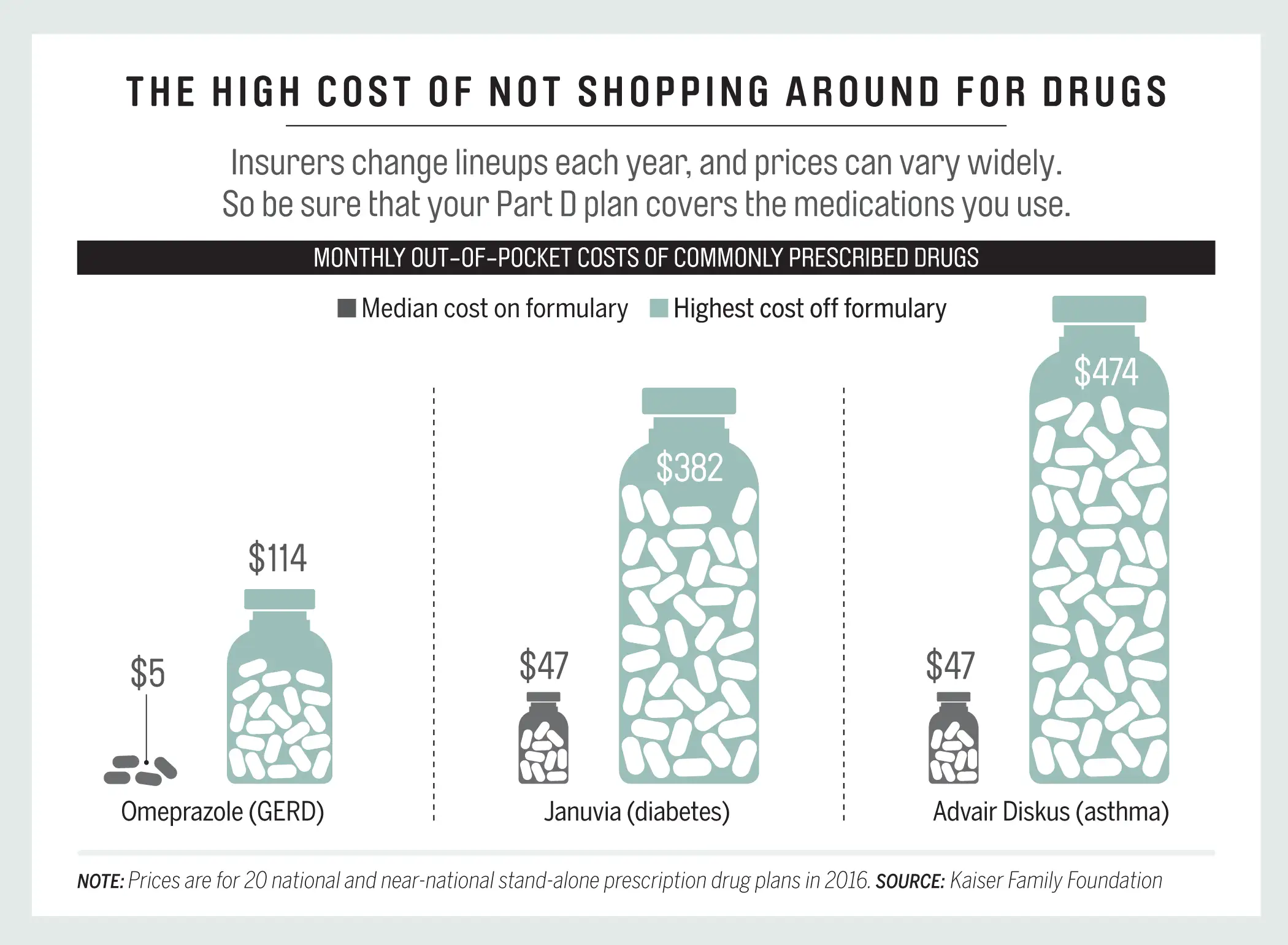

What good is a drug plan if it doesn't include the drugs you and your doctors think you need? A plan's list of drugs, called a formulary, is one of the first things you should evaluate in a Part D plan, since the cost difference for you if a drug is on-formulary or off-formulary can be huge (see the chart above for some examples). In most cases you can find what a plan charges for the drugs you need at its website, but Medicare's Plan Finder (medicare.gov/find-a-plan) is the easiest way to see how all plans available to you handle your drugs.

After you enter your drug information into Plan Finder, the software will sort through available plans and tell you roughly what a year's worth of those drugs will cost you. You can return to your account and change your drug list as needed.

What good is a drug plan if it doesn't include the drugs you and your doctors think you need?

When you use Plan Finder, make sure you include the pharmacies you like to use so that you can see whether a plan works with your pharmacy and how this may affect your costs. Part D plans usually include a preferred pharmacy network. Filling prescriptions through the network will generally be cheaper, especially for mail orders, than going outside the network to another pharmacist. So investigate. Are you restricted to a certain pharmacy provider for your plan's prescriptions? What happens if you want to fill a prescription elsewhere?

And don't assume that a plan that's terrific for you in 2016 will be terrific in 2017. Rates, formularies, and other details can change from year to year, and usually do.

Medicare gives you the right to freely change not just drug plans but also health plans every year during open enrollment, which runs from Oct. 15 through Dec. 7. I'm urging you to take advantage of this right and to make sure you have the best plan possible each Jan. 1. People tend to stick with the plan they have, despite overwhelming evidence that they would be better off switching.

Philip Moeller is an expert on retirement, aging, and health. Adapted from Get What's yours for Medicare: Maximize Your Coverage, Minimize Your Costs by Philip Moeller. Published by arrangement with Simon & Schuster Inc. Copyright © 2016 by Philip Moeller.