We Will Have Another Crisis...

- Michael Lewis Explains the Unlikely Bromance That Shaped the Way You Manage Money

- 4 Ways to Motivate Yourself to Save and Invest Like a Millionaire

- How to Invest Your Way to $1 Million

- Retire With Money: Take Care in Picking an Advisor

- Retire With Money: Relax, You Don't Have to Get Everything Right

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Few mutual fund managers could pull off what Robert Rodriguez did. During the tumultuous 2000s, his FPA Capital stock portfolio, which is closed to new investors, managed to earn an annualized 9% even as the S&P 500 lost money. At the same time, he also co-managed FPA New Income, a bond fund that earned a spot on our Money 70 list. Rodriguez, 62, is known for thinking big: In early 2007 he laid out a detailed case for why housing debt could trigger a crisis. Now he's just as worried about the federal debt. Rodriguez took a sabbatical in 2010—he traveled the globe, read about the fall of Rome, indulged his car-racing hobby—and has returned to FPA as CEO, with an advisory role on the funds. He spoke with editor-at-large Penelope Wang; the conversation has been edited.

Now that you're back, do you have a different perspective on the economy?

I would say a lot of nothing has changed. Before I left, I was vocal about the difficulties that were going to hit the U.S. economy: the growing federal debt and the lack of meaningful fiscal reform. These issues still have not been addressed. Meanwhile, banks are operating much as before—"too big to fail" is continuing. Investors are still chasing after higher yields and loading up on risky investments. The search for safety in the wake of the financial crisis lasted maybe two years. Very little has been learned.

Won't the economic recovery help us grow out of these problems?

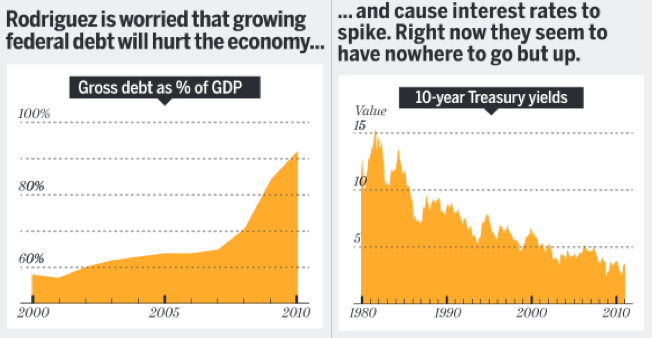

At best, we're facing a substandard recovery. It will probably take another eight years for the consumer to recover. But mainly I worry about the swelling debt of the U.S. government, which is ballooning faster than the economy is expanding. We've been concerned about this as far back as 2003, when federal debt was $6.8 trillion, or about 60% of GDP. At that point we went on a buyer's strike—we wouldn't lend long-term capital to a fiscally irresponsible borrower at low interest rates. And we haven't bought long-term Treasury bonds since. Okay, we were eight years early. But now the ratio of debt to GDP is above 90%, about $14 trillion. This is not a sustainable trend.

So you see rates rising, and bond prices falling. How big will the correction be?

Before my sabbatical, I told clients that if present trends in government continue, we will have another financial crisis within three to seven years—by 2018. I still believe that. We still have time to start the process of fiscal rectitude. But the window of opportunity is shrinking because 2012 will be an election year, when nothing happens.

Since 2003 the 10-year Treasury bond rate has averaged about 4%. Over the next decade, I would say the odds of us staying in the sub-4% range are very low, and the likelihood that we could get yields north of 6% is considerable. But it's hard to put a forecast together because when problems occur, they don't occur in a linear fashion. Take Greece. When the moment came that the emperor had no clothes, what happened to the Greek bond? It went from 4% rates to 10%.

As wary as FPA is of government debt, the New Income Fund hasn't been snapping up corporate bonds either. Weren't you tempted to buy beaten-down high-yield bonds after the crash? They did well.

We missed some opportunities, and I'll take responsibility for that. But I had serious concerns about the state of bondholders' rights. Look at how the GM and Chrysler bankruptcies were handled. The federal government interfered and made ad hoc decisions about who got paid, creating additional financial uncertainty. It was rule of man, not rule of law.

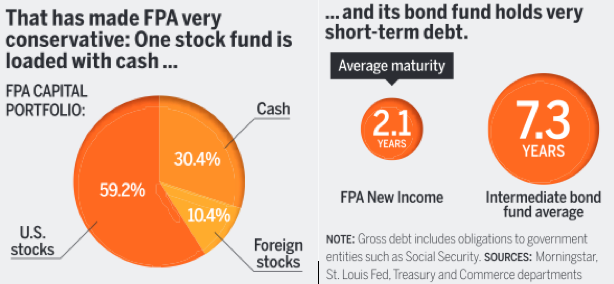

Today I think you have to have your head examined to be in high-yield bonds in general. There isn't enough extra yield there to justify the risk. As far as Treasury debt, we're not being paid to take the risk in intermediate- or long-term bonds, so we aren't going much beyond three-year maturities. We're sticking with one- and two-year bonds.

This conservatism has caused New Income to lag behind its peers in recent years. Have you heard shareholders complain?

What we've done over the past eight years is clearly explain to our investors why we keep maturities so short: the risk of rising rates, and that this policy will hurt returns at various times. But our main goal in New Income is to not lose money. We also say, "If you disagree with us, you're free to leave." And people stuck with us; the fund grew. But then in the last year investor redemptions have picked up as the "risk trade" has become more accepted—you know, selling bonds, buying stocks.

Speaking of stocks, your team doesn't seem to see much opportunity there either—FPA Capital is 30% cash. Is there anything you like?

So far the biggest opportunities we're seeing in stocks are in energy, where we've been investing heavily for more than 12 years. It's a supply-demand situation. Wherever I traveled last year, the one word that came to mind was "gridlock." Cities from Korea to Moscow to South America were totally filled with cars. It makes the 4 o'clock rush on San Diego Freeway in Los Angeles look like a speedway in comparison. There will be more and more demand for oil as consumers' incomes rise in developing nations.

But even there, we have a problem with the high valuations for these stocks. Prices aren't egregiously expensive, but they're not pound-the-table cheap anymore. As prices have moved up, my successors at Capital have trimmed holdings in energy.

Anything else worth holding?

I would say that the number of stocks that are cheap enough to make it through our valuation screen is in the bottom third of what I've seen over the past 20 years. But we believe that the companies that survive, especially if there is another crisis, will be those with liquidity, that are reasonably or highly profitable, that have some form of barriers to competition or unique capabilities. These prospects are in many industries—there's no one hot area. But one thing they have in common is that a growing percentage of their revenue is from overseas. Caterpillar, for example, has done well internationally.

Given your bearishness—and your interest in commodities—I'd think maybe you'd like gold.

When I look at gold, I have a hard time determining its value. There are certain areas of the world that love it for various reasons. It has been a store of value at various points in time. But if you compare gold and oil, which is more productive? That would be oil. Which has a longer life expectancy on this earth? Gold. One commodity does not have a diminishing supply, while the other one does. So I think energy is the better store of value.

Any plans to reopen Capital to new investors?

We may open it, but not likely in the near term. There are two reasons to reopen a fund. One is if you're seeing lots of investing opportunities out there, which we aren't. Another one would be when you're anticipating sharp market declines, with the expectation that the additional capital will be deployed after the market goes down. If you wait for the investment opportunity, you find that nobody wants to invest with you because of fear. The last time I opened Capital Fund, in 2001, I made something like 30 calls to potential investors and got no response. That's how human nature works in investing.