A Simple Trick That Will Help You Understand The Bond Market

- Why Skimpy Bond Yields Are a Retirement Game Changer

- This Nobel Economist Spotted the Last Two Bubbles—Here's What He Says About the Bond Boom

- Here's What to Expect From the Bond Market in 2015

- Yes, Stocks Are Tanking -- But Here's What We Should Really Worry About

- What Does a Bond Fund Manager Actually Do?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

With yields on 10-year Treasuries at a low 2.6%, many experts have been warning that bond investors could be in for unexpected pain if and when rates rise.

Okay.... wait, what? So bonds only pay 2.6% now, but in the future they might pay more? And that's bad why, exactly?

If you're someone who watches the market carefully, you know the answer to this (more on that in a moment).

But to most people—very much including me when I was first learning this—the language of bonds is totally counterintuitive. When the bond market has a no-good, horrible day, the newspapers and CNBC will tell you that bond yields rose. And then when bonds rally back, you'll hear that yields fell. And although many fixed-income investors hold bonds precisely because they want to collect regular interest payments, a scenario where bonds go from yielding 2.6% a year to, say, 3.6% a year is always described as awful.

If you are used to thinking about the stock market, it's always a bit of a struggle to hold the upside-down rules of bonds in your head. But recently I was having a conversation with a money manager, and in passing he did a very simple thing that made bonds instantly easier to understand.

He just flipped the numbers over.

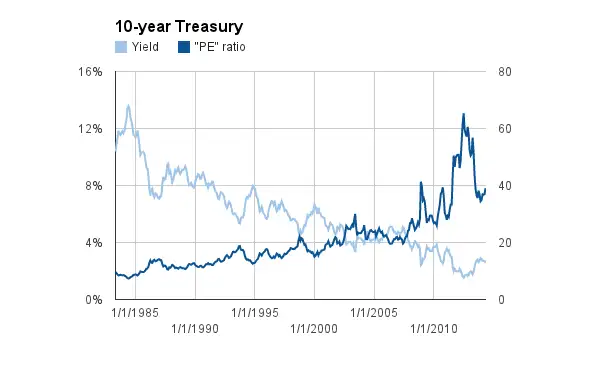

Specifically, he took the yield on a 10-year Treasury, which is the standard reference point for what's happening on the bond market, and inverted it. The 2.6% yield of Treasuries is equivalent to paying $38.46 for every $1 you get in income. (The simple math is 1 divided by 0.026.)

An experienced stock investor might quickly recognize that this is a lot like saying that bonds have a price/earnings ratio, or P/E, of 38.46. And stock investors know that high P/Es mean stocks are expensive. You are paying a lot for every buck of earnings (or, with bonds, coupon payments) you are entitled to.

A chart of bonds' "P/E ratios" show that by historic standards Treasuries are indeed expensive.

The helpful thing about the dark blue line is that it shows bonds going higher when investors are, yup, paying more for bonds. Not long ago, when investors were willing to accept a historic low yield of 1.5% for bonds, that meant they had to pay a "P/E" of nearly 67, or $67 for every $1 of income. Back in 2000, though, you only had to pay $15 per $1 of yield.

And just like you know that it's hard to make a lot of money on stocks if you buy in when the market is high, it's tougher to make a lot when you buy bonds at lofty prices. And that's where we are now.

Today, bond investors face two headwinds. First, there's the simple fact that the yields you'll pocket are low. The 2.6% you get on a 10-year Treasury is exactly what you can expect if you hold to maturity.

But, second, if rates move up, the market value — or price — of any bonds you own now will have to fall to adjust. (Imagine rates spiked and newly issued Treasuries are yielding 3.6%. The only way to get other investors interested in your existing 2.6% bonds is for you to cut their price so that, for the new owner, the pay off is equal to 3.6% of their investment. That's your loss.) That's why last year, when bond yields rose and prices fell in the second quarter, investors in intermediate-term bond funds lost an average of 2.6%, even after accounting for yield payouts.

Don't take the analogy to stocks too far. Unlike stocks and their earnings, bonds deserve to be pricey relative to their payouts, since those cash flows are reliable. Especially when, as now, there's little reason to expect high inflation that eats up the real value of income. And a core intermediate-term bond fund will still be much less volatile than stocks. (That 2.6% loss last year was a big deal in bond land, but amounts to what stock investors call a sideways market.)

But if you've ever scratched your head and wondered why people talk about bonds being "expensive," that still-high dark blue line is why.