The States With the Highest (and Lowest) Taxes for Retirees

- Here's How Much a Job Loss Now Will Cost You by Retirement

- Retirees Are Too Pessimistic on Their Investments—And It's Costing Them

- What U.S. Military Need to Know About Their New Retirement Plan

- This Common 401(k) Rule Is Making Life Difficult for Retirees

- The Military Is Revamping Its Retirement System to Attract Millennials

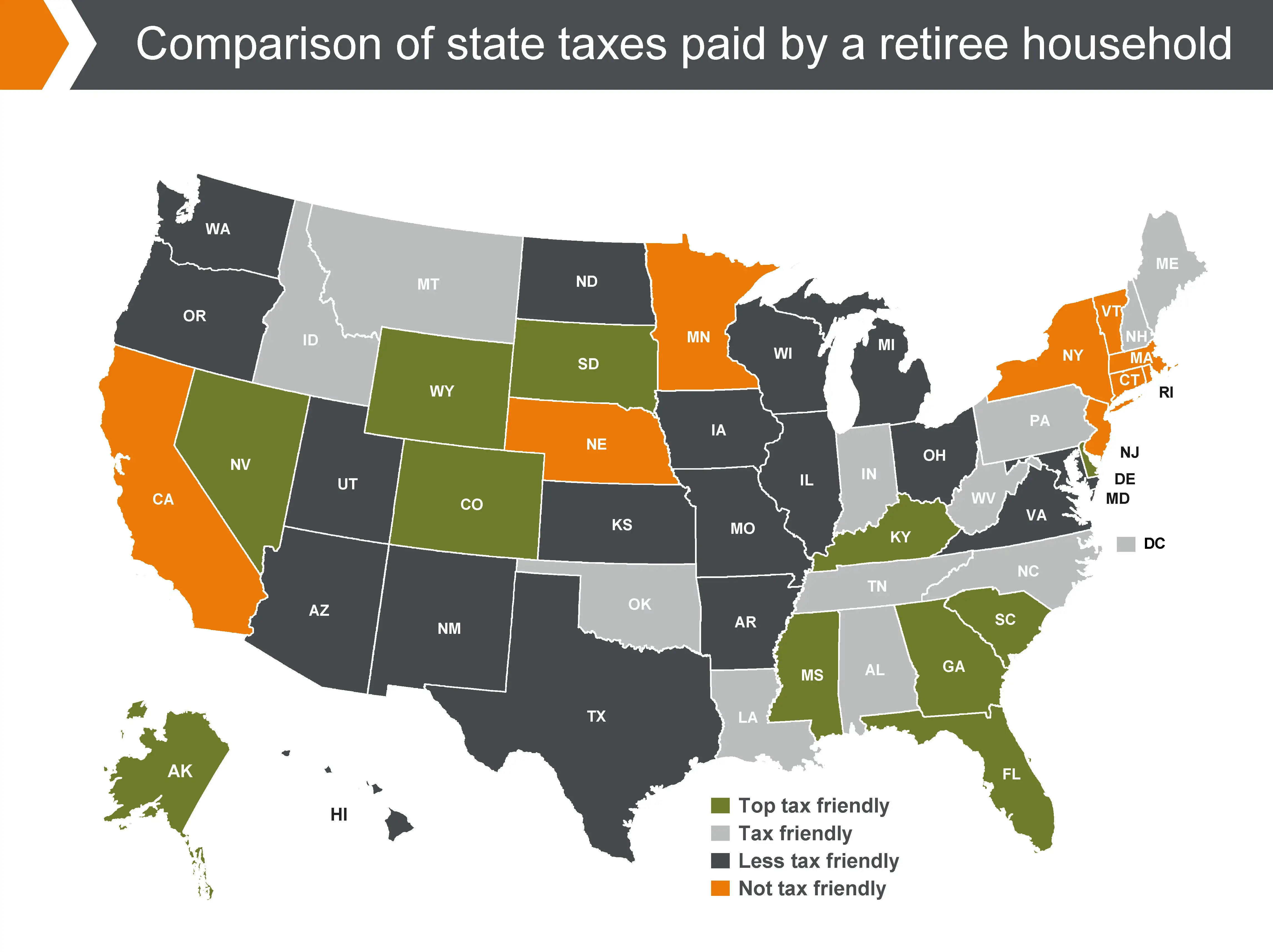

Retirees have many good reasons to change where they live: climate, health care facilities, hobbies, crime rate, proximity to family. Cost of living is another big consideration—and on that front, state and local taxes may be a big component. [Bankrate.com recently offered up its overall ranking of the best and worst states for retirees.]

States have very different tax structures. If you move for lifestyle reasons—say, to California—you might be rudely surprised by the state’s average effective tax rate of more than 13%. You can get similar weather, if not views, in Nevada or Florida, where the comparable state tax rate is less than 8%.

These are averages, reported in J.P. Morgan Asset Management’s annual retirement guide. The figures include income, sales, and property tax for a hypothetical retired couple. Your own rate will depend on many factors, including your sources of retirement income and the specific region in which you settle.

Different states treat income from Social Security, assets, earnings and pensions differently. For example, 13 states including Colorado, Connecticut, and New Mexico tax Social Security benefits, according to the J.P. Morgan report. Five states, including Oregon, Alaska, and New Hampshire, have no sales tax. Nevada, South Dakota, and Wyoming, among others, have no income tax.

Within a state, the city you choose may also makes a big difference. New York City, for example, levies an additional 3% to 4% on taxable income above and beyond the state levy. So it pays to give local tax treatment some thought before you pack up.

In general, the most tax-friendly states for retirees are, in order, Alaska, Delaware, Georgia, Nevada, and Wyoming, according to the J.P. Morgan report. The least tax-friendly states, in order, are New Jersey, Connecticut, New York, Massachusetts, and Vermont. Property taxes tend to be especially burdensome in the least tax-friendly states.

This is based on estimates for a retired couple filing jointly with annual retirement-plan distributions of $80,000 and annual combined Social Security benefits of $42,000. It also assumes property tax based on a home valued at 2.5 times the median in the state.

The average Social Security beneficiary gets 33% of total income from Social Security, 32% from earned income, 21% from pensions, and 10% from assets. Your own mix may be considerably different, which is why there are no easy answers to which state you will do best in, from a tax point of view. But it is worth looking into--and remember that taxes are just one part of the equation.