I Paid Off $180,000 in Student Debt in 8 Years. Here's How I Did It

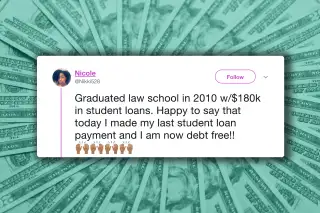

After Nicole Medham, an attorney based in New York City, finished paying off her $180,000 student debt, she announced the news in a celebratory tweet — complete with a Beyoncé hair-flick gif.

The Internet loved it, responding with over 30,000 likes, as well as dozens of commenters asking for Medham’s secrets.

We were curious too. We asked Medham, who graduated law school in 2010 with $180,000 in loans, to explain her strategy. Largely, she says, it came down to focus. She never missed a payment, and added extra to her monthly minimums to ensure she could be debt-free faster.

Then there was her housing situation: Although she works in Manhattan, Medham decided to live with her parents in Brooklyn instead of a costly city studio or one-bedroom. (She says she paid modest rent and pitched in on some household bills.) “I always tell my friends, if you can live at home, if you don’t have a bad family situation, do that,” Medham says. “Don’t worry about people making fun of you; when you can pay off your debt, they’ll be wishing they were in your situation.”

With her high law firm salary, plus money she saved by living at home, Medham could — and did — allocate her earnings to her debt and save what was left.

Here is everything else Medham says she did to pay off her huge student loan burden — plus the advice she has for others struggling with debt.

How did you wind up with such a big debt?

All of my debt was from student loans from law school. Luckily I didn’t have any debt coming out of undergrad. I started law school in 2007. The idea of taking all of this debt for law school was a little bit jarring, and at one point I was thinking about not going. But, eventually, I bit the bullet.

I did get a little bit of financial aid from my school, but the bulk of it was all loans. I had private and federal loans, and a Perkins loan.

Was there a moment when you realized you needed a lifestyle change to pay it off?

I had that moment right before I went to law school. It was always in my head that, as soon as I get out, I need to think about the best way to pay off my loans — because I don’t want to have that hanging over my head forever. Especially living in New York City, where the cost of living is super high and you want to have financial freedom to not just be paying off your loans.

I had a friend in law school who had a really good Excel spreadsheet, where you could plug in figures for your income and it could figure out how long it would take you to pay off your loans. If you had a goal of paying things off in five years or six years, you could put in that information too. That stuck with me.

Initially my goal was to finish paying off my loans in five years, but it didn’t work out that way because of some job stuff. I graduated around the time of the recession, and that really had a huge effect on the legal industry. I didn’t start my firm job right away; I was deferred for a year and worked at a public interest position, so I wasn’t making the bigger salary I thought I would.

That tacked on a couple of years to my five-year plan, but I still had it in my head that I want to finish as soon as reasonably possible.

What were your biggest expenses at the time?

Honestly my biggest expense was my loan.

I paid a couple of bills around the house to help my mom, but largely it was my loans. I graduated in May 2010, and I started paying off my loans automatically in November 2010. Automatically, my loan servicers had me on a 10-year repayment plan. I know a lot of people try to [change it to] 20 or 25 years, or income based, or what have you — but I just left it that way.

At the time, when it was a 10-year plan, my minimum monthly payment was around $1,900 to $2,000. That was really my biggest expense.

What big lifestyle changes did you have to make?

At one point, I left my firm job and I wasn’t working. At that point I cut out all the extras. In addition to still living at home, I was fortunate enough to have saved quite a bit of money from my firm job — so that when I just volunteering, I didn’t have to put my loans into forbearance; I could still pay them off.

I wasn’t bringing in any income, but I had saved so much where I was still paying off my loans normally; I was paying the monthly minimum.

What is your current financial state?

Currently in savings I probably have $55,000 to $60,000.

How did you maintain your savings while paying off your debt?

I didn’t maintain it fully. During the period in which I was just volunteering, I was using my savings to continue paying off my loans, and by that time I had paid off one of my loans. So that was a good $15,000 to $17,000 I had to use of my savings; I would have had way more money had I not taken a gap year.

But the thing is, outside of that gap year, I didn’t use my savings to pay off my loans; I was just using my salary. I don’t touch my savings unless there is an emergency.

What's your strategy for putting money in savings?

I allocate monthly, but it’s not formal. Essentially, what I always plan to do is to set aside a certain amount of money toward savings. For the last couple of years, with my lower government salary, I want to make sure I’m putting in at least $500 a month.

And then you'd pay the loans after that?

Yes. None of my loans were consolidated.

What was helpful: I organized my loans in order of highest interest rate, and that’s how I decided what to pay off first. I had one loan that had an 8.5% interest rate when I got out of law school, so that’s the one I focused on trying to get rid of first.

I know I was in an unusual position because I was working at a big firm and making a higher-than-usual salary, but for people looking for tips, I always tell people: Even if it’s $50 or $100 extra you’re putting toward your debt per month, it makes a huge difference.

The last loan I finally paid off was my Perkins loan: The monthly payment was $127, but from the time I graduated, I always paid $150. That was just an extra $23, but over a seven-year period, it helped me get closer to paying off the principle faster. It’s just $23 a month. So that’s something very easy that readers can do: If you can afford to add a little bit extra on a loan, that’s when you really start seeing a difference in your loan burden.

Did you use any other tricks?

It was just being focused. Quite a few of my friends switched their automatic repayment plan so that they could have a lower monthly payment. Just realize that, paying over 20 years, you’re going to be giving these loan service companies a whole lot of money — just based off the interest.

I know everybody’s situation is different. Some people were lucky because their parents gave them a huge chunk of money; I’m lucky because my family allowed me to stay home. It’s just having the mindset that you want to get rid of these loans as quickly as possible.

How does it feel to be debt free?

It feels really good. A part of me can’t believe it.

It will be super interesting to go through a whole month without having to pay a monthly loan payment. I have a smile on my face thinking about it.

What’s your next financial goal?

My next financial goal is to just to continue saving money, so I can potentially buy a condo or apartment in New York City. Also, I want to really get into investments for beginners, now that I have disposable income.

What’s your biggest piece of advice for people who are struggling with a lot of debt?

The best thing to do is to track all of your money for a period of two to three months. Have a column of fixed costs, like your rent and bills, versus the things that fluctuate. Track those things so you can figure out what you’re really spending your money on, and what to cut.

For me personally, I’m going to start bringing my lunch to work at least two times a week. I buy lunch pretty much every day, and I work in Manhattan. Even the local salad place, salads cost $14-$15. I’m spending a lot of money on lunch alone. That’s something that can be decreased.

If you see you’re going to Starbucks everyday, maybe buy the Keurig cups from Target. People are really surprised at what they spend their money on, and that’s a good way to take things out. And that’s where you can see savings right away.