Tax Day Is Fast Approaching. Here Are All the Ways the New Tax Law Affects You

- Dec. 31 is a Crucial Tax Deadline for Many Retirement Savers. Here's What to Know

- If You Own a Mutual Fund, You Could Face an Unexpected Tax Bill This Year

- This Is the Clearest Sign Yet That the Trump Tax Cuts Are Having an Impact

- The Best Stocks for 2020, According to 3 Investing Pros Who Outsmarted the Market

- Investors in Active Mutual Funds May Get Surprise Tax Bills This Year. Here's Why

- What the Democrats Winning Georgia Means for Your Wallet

- H&R Block Wants to Put Your Tax Refund on an Amazon Gift Card. Here's Why That's a Terrible Idea

- Many Americans Are Getting Smaller Tax Refunds This Year. Here's How to Know If You'll Be One of Them

- How Much Do You Pay in Taxes? Research Says It's Less Than You Think

- HQ Trivia’s $250,000 Jackpot Will Come With a BIG Tax Bill

With Tax Day 2018 coming up fast, many Americans are deep in tax prep, scrambling to meet this year's April 17 tax deadline.

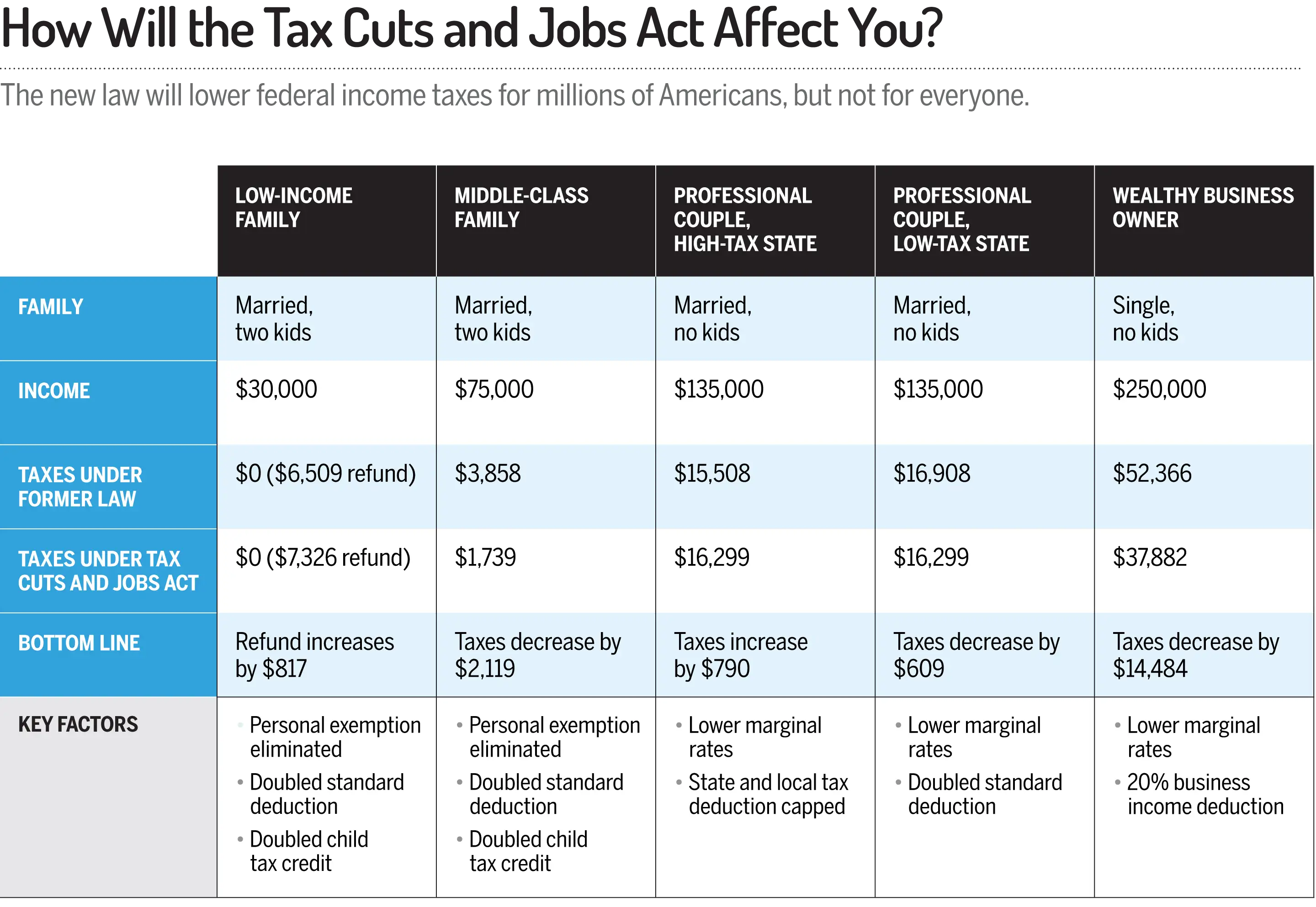

But as you're wrapping up paperwork for your 2017 taxes, it's also a good time to look at how the new Tax Cuts and Jobs Act—arguably the largest overhaul of the U.S. tax code since the Ronald Reagan era—will affect your taxes for 2018 and beyond.

Much remains to be settled, of course. While the bill was designed to boost the overall economy and create new jobs, it's too soon to tell whether those changes will materialize—or whether the law's $1.46 trillion price tag will push inflation and interest rates to levels that outweigh any potential benefits. What you can count on, however, are dozens of changes to the individual tax code—many of which already went into effect in January, such as a more generous standard deduction and child tax credit. Other perks have been curtailed, such as the state and local tax deduction, now capped at $10,000.

Overall, the law should mean a lower tax bill and simpler filing for millions of Americans. But just how much you can expect to save depends on your particular circumstances: for instance, what kind of job you hold and whether you own your home or rent.

To understand just where you fit in, and how the tax changes will affect you, read on.

If you have a middle-class job ...

Critics have been quick to paint the new law as a giveaway to the rich. There's some truth to that, with more than 40% of cuts going to the top 5% of earners, according to the nonpartisan Tax Policy Center. But middle earners stand to benefit too, at least in the near term. In 2018 middle-income households—those earning $49,000 to $86,000—will see a tax cut of $930 on average, the Tax Policy Center found.

Those who make a bit more but might still plausibly be called middle class—families earning $86,000 to $149,000—will get back even more, with an average cut of $1,810.

The savings "cover about a year's worth of gas for your car," said House Speaker Paul Ryan at a press conference. "It can help you put away more money for college. It can help you save for retirement."

The extra cash may have already started showing up in your paycheck. The IRS urged companies to adjust the amounts they withhold from workers' paychecks by mid-February. That means your employer has probably already taken action, based on information in the W-4 form you filled out when you were hired. If you want to fine-tune what you pay, the IRS offers a withholding calculator in the "individuals" section of its website, which it has updated to reflect the new rules.

The new law could also do more than just lower the amount you owe. One of the biggest changes to the individual tax code is a doubling of the standard deduction—the preset amount all taxpayers are allowed to lop off their taxable income, unless they opt to tally individual deductions—to $12,000 from $6,500 for singles ($24,000 from $13,000 for couples). The upshot: The number of taxpayers who need to laboriously itemize their expenses is expected to fall to about 19 million for 2018, from 47 million under the old rules, according to the Tax Policy Center. (Of course, if you aren't sure which method will reap you the most, it may make sense to tally your potential deductions just to see, says Tax Policy Center researcher Joseph Rosenberg.)

The new law does have its drawbacks, however. One is that while the business tax cuts are generally permanent, most individual provisions expire after 2025 unless Congress extends them. And while lawmakers had pledged to eliminate the alternative minimum tax, in the end they kept it, although the amount of income that's exempt rose to $70,300 from $55,400 for singles ($109,400 from $86,200 for couples).

One widely used perk that will disappear: the personal exemption, a $4,150 write-off each taxpayer has been able to claim for him or herself and each dependent. The good news: To offset that loss, lawmakers expanded another benefit available to parents, doubling the child tax credit to $2,000 and hiking the threshold at which it phases out to $200,000 from $75,000 for singles ($400,000 from $110,000 for couples). Under the old rules the exemption acted like a deduction, reducing filers' taxable income for each person claimed, while the credit, which takes its place, will cut filers' bills dollar for dollar.

Takeaway: Most people can expect a tax cut.

- You may not have to itemize to save.

- Most of the savings expire in 2025.

If you're a working freelancer ...

If you work for yourself, you may be in for an even better deal, with a new benefit that could cut your tax bill by up to roughly one-fifth.

While intended to promote hiring and investment by small-business owners, the new rules apply to anyone who is his or her own boss—from Uber drivers to wedding photographers to freelance journalists.

Savings could be significant. A single freelancer with no kids making $50,000 would owe just over $10,200 in federal tax next year, nearly $1,800 less than before, according to the Tax Policy Center. A wage earner with the same profile would also get a tax cut, but a much smaller one—worth about $1,100.

The benefit takes the form of a 20% deduction that taxpayers can apply to "pass-through" business income. That doesn't include dividends or interest if you own stocks and bonds. But it does include partnerships, S corporations, and so-called sole proprietorships, the default status you assume when you work for yourself.

You are eligible even if you take the standard deduction. Still, not everyone who is self-employed will benefit. To prevent wealthy professionals who aren't likely to do much hiring from getting a hefty tax cut, Congress put in place several restrictions. Perhaps the biggest: The benefit phases out for workers in so-called service fields—such as health care, accounting, and the law, among others—who earn more than $157,500 from all sources ($315,000 for couples).

And some workers who may think of themselves as freelancers—those who move from gig to gig yet get paid as an employee through an outsourcing agency—may not be eligible. One way to tell: "Generally speaking, you are probably a freelancer if you receive a Form 1099 and an employee if you receive a W-2," says Melissa Labant, director of tax policy at the American Institute of CPAs.

Takeaway: You get a new 20% deduction.

- You don't need to own a business.

- Wealthy professionals face caps on the deduction.

If you're buying or selling a house ...

For homeowners, often regarded as a favorite child of the U.S. tax code, the new law scales back some long-standing write-offs, including mortgage interest and state and local taxes.

It's not necessarily bad news. Given the law's many other tax-slashing provisions, many, if not most, homeowners will likely still see an overall tax cut. On the other hand, the law could still hurt them in a different way: by slowing the growth of home prices.

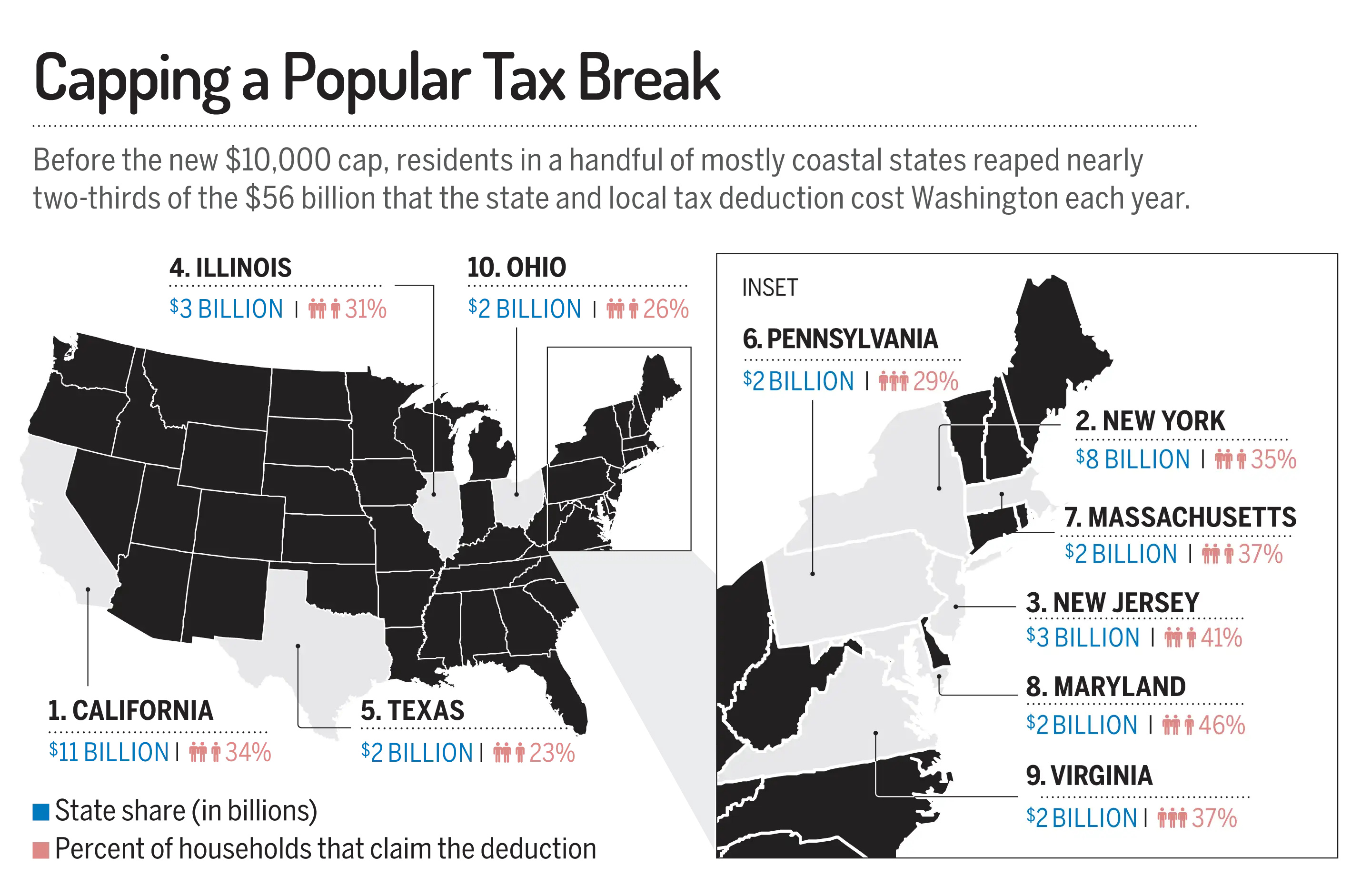

The chance to deduct hefty expenses like mortgage interest and property taxes has long been a big financial benefit of owning a home. These will continue. But lawmakers tightened the cap for mortgage interest, allowing homeowners to deduct interest on loans up to just $750,000, down from $1 million, for money borrowed after Dec. 14, 2017. Meanwhile state and local taxes were squeezed even more dramatically. While previously unlimited, taxpayers will now be allowed to deduct a total of $10,000 from their federal tax bill, including income, property, and any other taxes owed to state and local governments.

The double whammy means homeowners in coastal states like New York and California could be hit hard, since home prices ($1.4 million average in Manhattan; $1.3 million in San Francisco) and taxes (more than 10% of income in both places) are both high. (It may be no accident that blue states are bearing the brunt.)

Homeowners who live in less expensive houses or in lower-tax states won't necessarily fret the new caps. That's because the value of the new, doubled standard deduction will outstrip housing costs they otherwise would have written off. (The share of homeowners who itemize is expected to fall to 14% from 44%, according to Zillow.)

Even for taxpayers who end up with lower bills, however, the law still poses a financial risk. With some homeowners losing deductions and others no longer needing them, some economists worry the rules could sap incentives for Americans to buy homes, hurting home prices.

One recent study by the Urban Institute found that so-called break-even rents—the monthly amount above which renters are better off becoming homeowners—jumped significantly under the new tax law for upper-middle-class and wealthy taxpayers. Under the old rule, for instance, for a typical three-person family earning $75,000, owning became more financially advantageous once the family's monthly rent exceeded $893. Under the new law that number climbs 14%, to $1,017. For wealthy families the difference can be even more dramatic. For a family making $300,000, the break-even rent jumps 32%, from $2,757 a month to $3,631.

So what if you're a homeowner worried about values? The National Association of Realtors says the change isn't likely to send home prices downward, but the group is predicting slower growth for 2018 of 1% to 3%, down from 5% to 7%.

Takeaway: Homeowners take a hit.

- You may still see lower taxes overall.

- Housing price growth could slow as a result.

If you're paying for school ...

Parents and grandparents saving for a child's education have big new 529 plan withdrawal options: private and parochial schools.

The plans have long been a key college savings tool. Money that's invested grows tax-free, and you don't pay taxes on withdrawals if you use money for approved costs. Now, those approved costs include K-12 tuition.

There are some limitations. Since 529s let parents skip taxes on investment gains, any tax benefits are likely to be smaller when that money is spent on secondary education—if only because, all things being equal, the money will be withdrawn sooner. In addition, when it comes to higher education, eligible expenses include tuition, room and board, and books. With the K-12 provision, only $10,000 in tuition per child, per year, qualifies.

All the same, the increased flexibility of 529s could be especially valuable to residents of the more than 30 states that offer a state tax benefit for 529 contributions. If your state and local tax deduction is limited because of the new $10,000 limit, you may be able to contribute more to a 529 plan and recoup some of that money.

One thing to keep in mind: Not all state tax codes automatically follow the federal definition of a qualified 529 expense. And that means you may not be eligible for a state tax break if you use a 529 for K–12 tuition. The answer will vary by state, so ask your plan administrator about potential consequences before withdrawing. States including Iowa, Indiana, and New York are still assessing whether state tax benefits will apply to private school tuition. If they don't, taxpayers risk having to pay back any deductions claimed on money later used for K–12 expenses.

Takeaway: K-12 tuition gets a new break.

- For some families, the tax break may offset the new cap on state and local deductions.

- Check your state's eligibility rules.

If you're saving for retirement ...

While most Americans are focused on their personal tax bills, the centerpiece of the new tax law is actually a big tax cut for corporations, which lawmakers hope will give a jolt to the economy and, with it, your 401(k).

The new law cuts the top corporate tax rate from 35% to 21%. The law also gives businesses a big incentive to repatriate some $3 trillion worth of earnings sheltered overseas, which will be taxed at 8% to 15.5%—a significant discount to the new, lower corporate rate. Republicans hope this flood of new cash will boost corporate profits, making stocks more attractive.

To be sure, many investors have already reacted to the promise of tax cuts. The S&P 500 rose more than 20% last year. Those big gains mean stock prices are higher, relative to profits, than at any time since the dot-com bubble.

Some analysts, however, think stocks still have room to rise. One big reason: While investors have been banking on a tax cut for a while, it's not yet clear how the changes will affect individual companies, especially firms bringing back money from overseas. Stock analysts hope companies will use a big slug of that money to repurchase their own stock, a practice that tends to boost earnings per share and ultimately stock prices. Buybacks may total $585 billion in 2018, projects Goldman Sachs, up from an estimated $495 billion last year.

Small companies, without much in the way of overseas profits, stand to benefit too. That's because with fewer tax-planning options, they're more likely to have paid the top 35% rate under the old rules. (One recent study by the left-leaning Center on Budget and Policy Priorities pegged the average effective tax rate for multinationals at 28% under the old rules.) As a result, according to Sameer Samana of Wells Fargo Advisors, returns for small stocks could even outpace those of larger ones. Samana forecasts a 7% rise in the Russell small-cap index for 2018, compared with a more modest 4% gain for the S&P 500.

While stocks rallied on the tax news, bond investors haven't been so lucky; 10-year Treasury yields rose 5% in the first weeks of the year. (Bond prices fall when yields rise.) And bond investors' pain could increase if the tax bill drives economic growth, as the Trump administration is hoping, according to Samana. That's because rapid growth would likely be accompanied by inflation, prompting the Federal Reserve, already forecast to raise rates three times in 2018, to move even faster.

Bond investors also face another risk looming on the horizon: the $1.46 trillion the bill is expected to add to the U.S. debt by 2027. While that total may be trimmed somewhat by economic growth, economists worry the extra debt could push interest rates up and bond prices down. "That's a difficult situation" for retirees with long-term bonds, says Red Bank, N.J., financial planner Thomas Yorke. Instead, he recommends balancing a portfolio out with shorter-dated bonds, despite their lower yields.

Takeaway: Buybacks could boost stock prices.

- But valuations are already high, so the effect may be muted.

- Rising interest rates are another threat to the rising stock market.