Unemployment Benefits Fail to Cover Basic Living Expenses in Most States, a Money Analysis Finds

- How Rich Are Donald Trump and Kamala Harris? Inside the Candidates' Personal Finances

- Money Teams Up With Financial Planning Association to Find America's Best Financial Planners

- Identity Theft: Who's at Risk and How It Affects Their Lives

- These States Are Using Their Budget Surpluses to Give Tax Breaks to Residents

- How Much Is Pet Insurance?

Imagine you and a friend live and work a 15-minute drive apart in Dubuque, Iowa and Dickeyville, Wisconsin, and both lose your jobs when your employers close for good. You pay the same rent and make comparable salaries that allow you to draw the maximum unemployment benefits in your state.

Iowa pays you enough to cover the basics, with a little left over for other expenses. Your Wisconsin friend, by contrast, receives about $950 less a month from his state’s unemployment program, forcing him to turn to family and food banks to make pay his rent and keep food on the table.

This scenario plays out daily across the country thanks to the crazy quilt that is unemployment insurance in America. Each state runs its own unemployment insurance program, with “the federal government taking only an advisory role,” says Andrew Stettner, Senior Fellow with The Century Foundation.

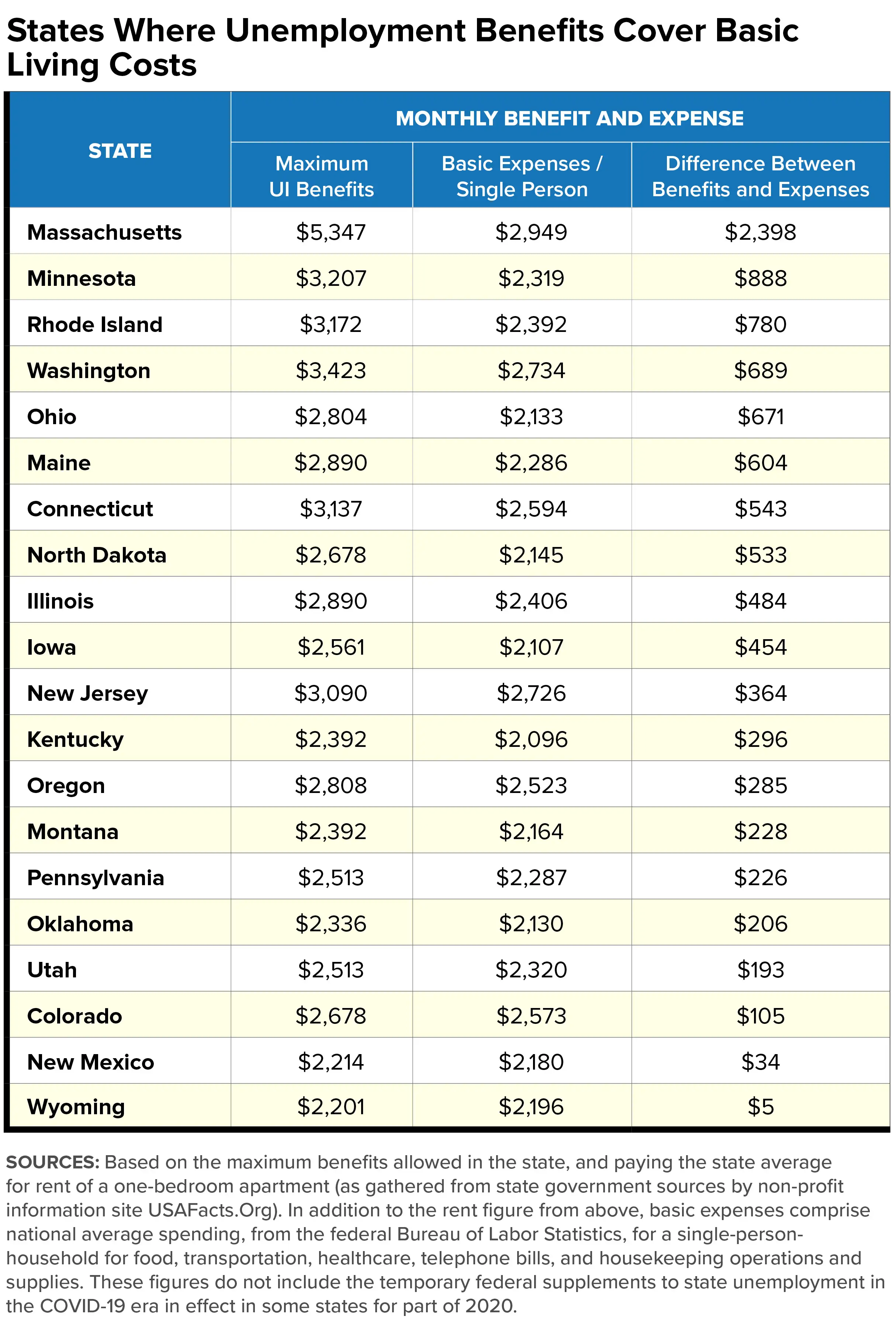

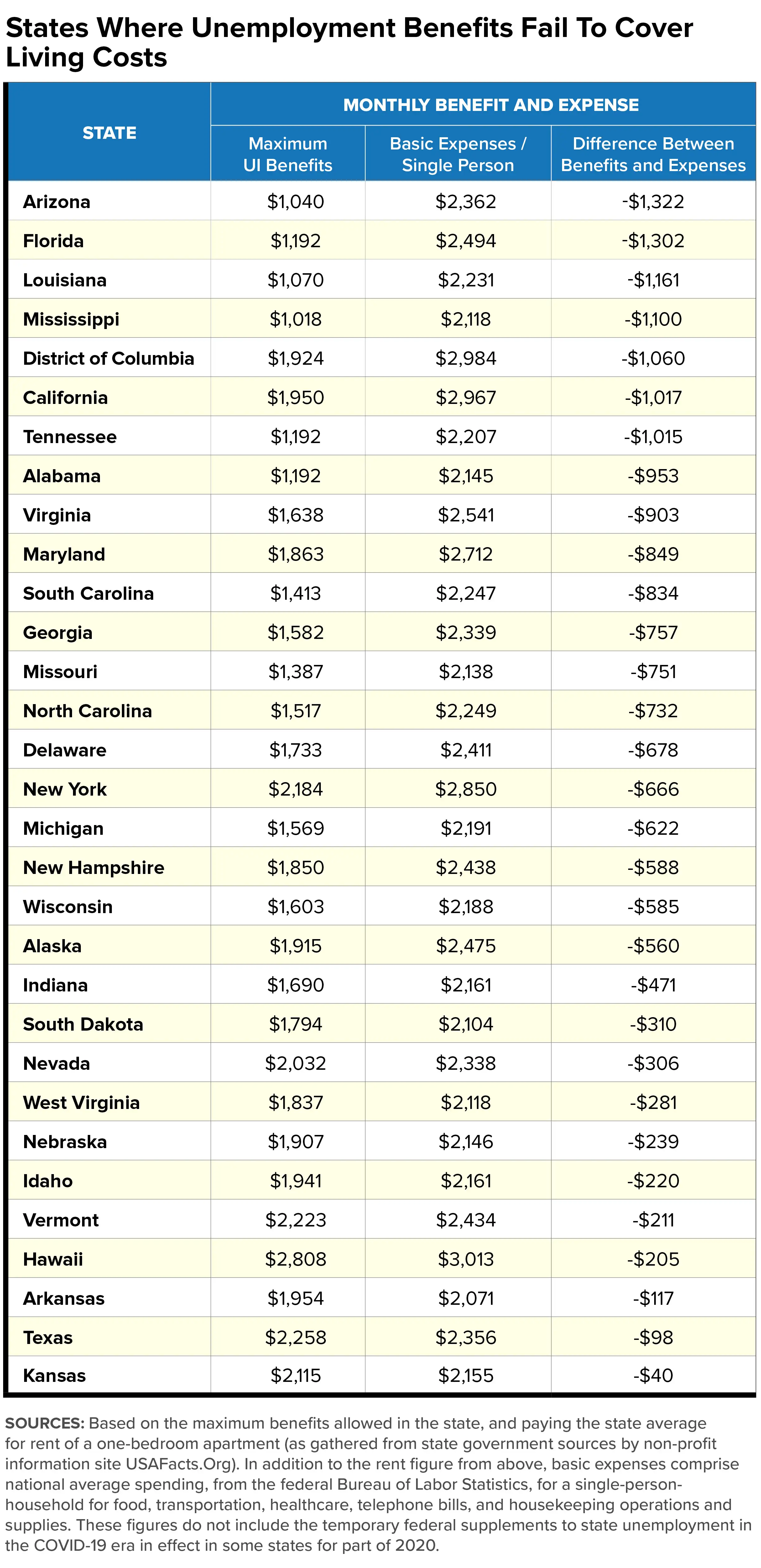

Washington does impose a federal tax that helps states pay for unemployment benefits, along with providing occasional supplemental unemployment payments, such as those included in the CARES Act during the COVID crisis. But each state decides the level of benefits to provide. And in a full two-thirds of states, those payments fall short of covering the living needs of unemployed workers, a Money analysis finds.

We added local rent costs for a one-bedroom apartment, as gathered by USA Facts.Org, the non-profit government-data site, to select average national expenditures for a one-person household, as calculated by the federal Bureau of Labor Statistics. We included spending on food, healthcare, transportation, and cell-phone bills but not discretionary items like furniture, clothing, and entertainment that many might forego when out of a job. Then we compared each state's total for rent and other spending to the most that unemployed workers can collect there.

The resulting rankings are a mishmash that reveal a fractured system, at best. On the whole, affluent states are more likely to provide adequate unemployment benefits. Massachusetts and Connecticut, among the wealthiest of states, also provide some of the most generous payments in relation to living costs, as do well-off North Dakota, New Jersey, Minnesota, and Illinois.

But states where jobless benefits cover the basics also include Maine and Kentucky, both of which are among the 10 poorest states in the country. And places where benefits fall short of living costs include the District of Columbia, where incomes are far higher than those of any state, and three states where incomes are well above average: California, New York, and Maryland.

Low state benefits were a better predictor of whether jobless recipients would be in the financial red than a high cost of living in the state. Still, Hawaii, California, and New York are among the states where high average rents help to create big budget holes for those who depend on UI payments.

It doesn’t help that unemployment benefits are constant within each state, but the cost of living isn’t, especially in highly urbanized states. How much you need to make ends meet varies by $1,500 and $2,000 a month respectively between the priciest and cheapest counties in New York and California, for example.

Unemployment: The Most Generous and Least Generous States, Explained

If economics doesn’t adequately explain the state-to-state disparities in jobless benefits, neither do traditional Republican and Democratic political differences. Both the most generous and least generous states for benefits are a mix of political red, blue, and purple. Some Republican-inclined states are notably high in their payments, and some Democratic jurisdictions are among the most measly. And vice-versa.

Racial politics may play a bigger role in explaining disparities than party leanings. As researcher Stettner points out, states where benefits are the most ample tend to have higher proportions of Whites in their populations. Conversely, states in which payments fall short by often have above-average Black people per capita, and have had that for a long time.

“In the deep South, with its higher proportion of Blacks, workers were traditionally viewed as a little more disposable and less deserving” of unemployment assistance than is the case elsewhere, Stettner said. The mostly White legislators tended to view the programs as “more like welfare, and so ‘we don't really want to support it that much.’”

Then come the differing calculations on how best to sustain benefits over time, especially during recessions. Many states that now have low benefits, such as Georgia, chose in the past to freeze or even reduce the unemployment tax on employers — a key source of programs’ funding. That limited the ability to increase worker payments over time, Stettner says, and sometimes forced the states to borrow against their unemployment trust funds — loans that eventually needed to be repaid, further hampering improvements to benefits.

Also, not all states index benefits against weekly wages in the state, to help reduce the effects of inflation. And among those who do so, Stettner says, many reduced or eliminated that indexing during the Great Recession of 2008-2010, and most have not fully restored those automatic increases since.

Finally, Stettner says, economic history helps explain the high benefit levels of many northern states, from Maine to Minnesota to Montana to Washington and Oregon. In those, he said, unemployment programs were established to allow sustained prosperity for a workforce where employment was highly seasonal, dominated as it was by industries such as logging. While many of those state economies have since diversified, the tradition of strong out-of-season benefits has remained.

More From Money:

How to Apply for Unemployment Insurance and Get the Most Money