What Is an IRA?

- Why Some Social Security Recipients Will Get 2 Payments in May

- Why Keeping Your 401(k) After Retiring Could Be a Smart Savings Decision

- Most Adults Fail This 5-Question Quiz on Retirement Basics

- Most Older Investors Say Retiring at Age 65 Is No Longer Feasible

- Why the 'Right' Retirement Age Doesn’t Actually Exist

An individual retirement account, or IRA, is a tax-advantaged investment account that allows you to save for retirement on either a tax-free or tax-deferred basis, depending on the kind of account you have.

With a traditional IRA, you won't pay taxes on your earnings until you make a withdrawal in retirement, or you can contribute after-tax income with a Roth IRA. Both of these kinds of accounts can help fund your retirement, perhaps alongside Social Security payments and workplace benefits such as a 401(k).

Regardless of what IRA you choose, these accounts can boost your retirement saving and diversify your portfolio. We'll explain the differences between the two main types of IRAs below.

IRA fast facts:

-

- Anyone can open an IRA account as long as they have earned income, even minors.

- There are certain exceptions that allow for penalty-free early withdrawals of your IRA contributions.

- Generally, however, withdrawing earnings before the age of 59½ is subject to a 10% tax penalty.

- You can own more than one type of IRA.

- Anyone can open an IRA account as long as they have earned income, even minors.

- There are certain exceptions that allow for penalty-free early withdrawals of your IRA contributions.

- Generally, however, withdrawing earnings before the age of 59½ is subject to a 10% tax penalty.

- You can own more than one type of IRA.

Part of what makes IRAs attractive is that they are simple to set up and offer certain tax benefits. Unlike a 401(k), which requires sponsorship from an employer, you can open an IRA through a bank, broker or an automated investment advisor on your own in minutes. There is no age requirement on these accounts, so anyone can open an one as long as they have W-2, 1099, or 1040 earnings.

Determining what type of IRA is right for you depends on your income, both now and what you expect to earn in the future. Roth IRAs have an income limit of $161,000 for single filers and $240,000 for married couples filing jointly as of 2024. If your wages surpass the cap, you may want to consider a traditional IRA.

According to Alicia Munnell, director of the Center for Retirement Research at Boston College, if you’re eligible for both a Roth and a traditional IRA, you should take a look at your tax expectations in the future to decide the smartest option.

“If you have a high income, a traditional IRA can allow you to defer paying income tax now and help you save toward retirement," Munnell says. "If you would prefer to pay taxes upfront as you contribute and not worry about it later, a Roth can be a good investment.”

Traditional vs. Roth IRAs

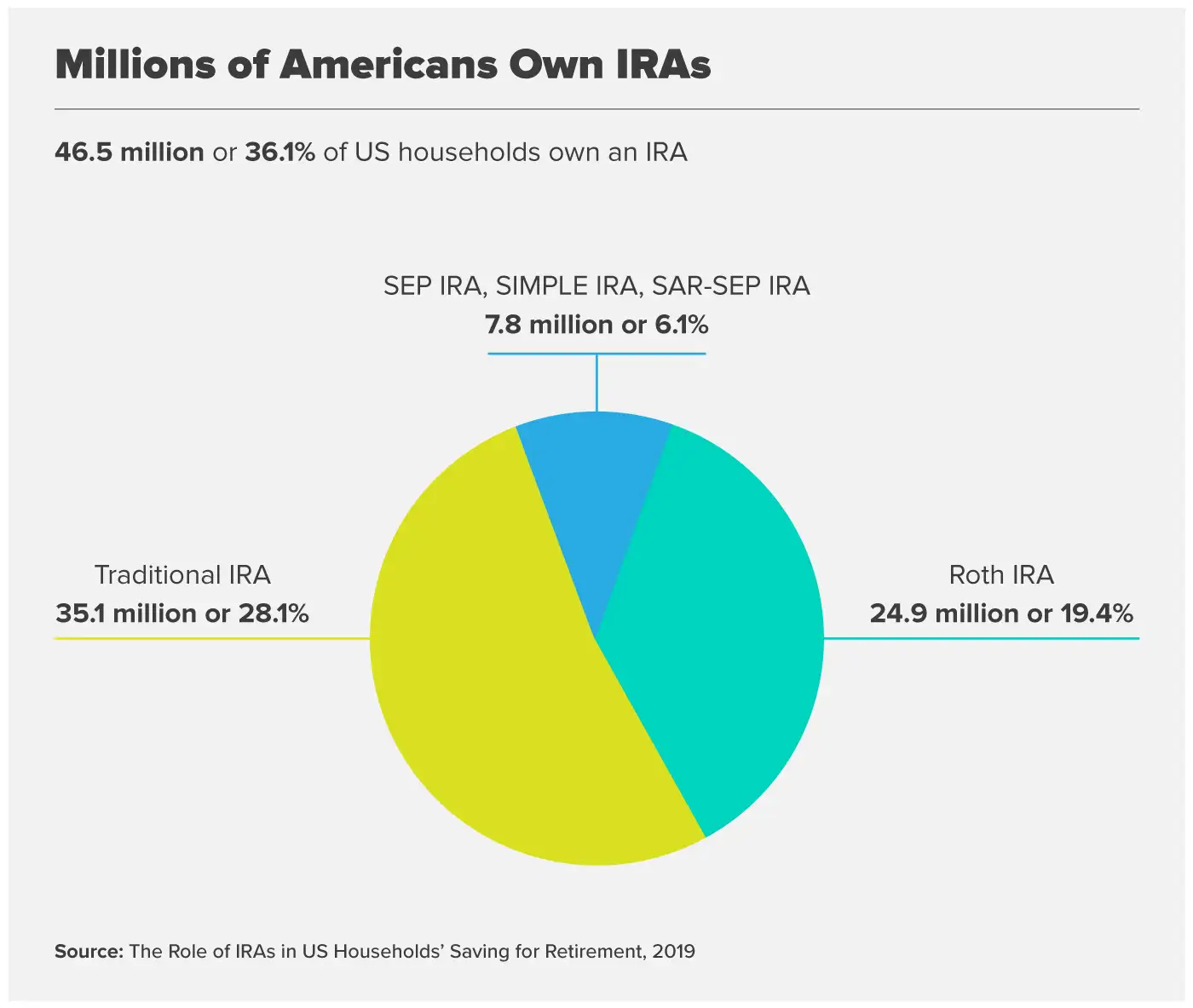

Traditional and Roth IRAs are the most common IRAs. More than 60 million Americans own IRAs as of 2020, according to the think tank Tax Policy Center, with the average account balance hovering around $157,000.

One of the main advantages of both traditional and Roth IRAs is that your investments will grow tax-free.

| Traditional IRAs vs. Roth IRAs |

| You can defer paying income tax on your contributions until they are withdrawn from your account. | Your investments are made with after-tax dollars so that once you reach retirement you’ll get your savings tax-free. |

| Has no income limit. | Has an income limit. |

| Has required minimum distributions (RMDs) starting at a specific age. The account holder must start taking RMDs at 72, or at 73 if they turn 72 after Dec. 31, 2022. | Has no required minimum distributions (RMDs,) meaning you can continue to let your savings grow indefinitely. |

| You may qualify for a tax deduction. | Doesn’t include tax breaks. |

| There’s a 10% early withdrawal penalty on distributions before age 59½ unless the money is withdrawn due to an exception such as death, disability, funding education, medical expenses, a first home purchase, or the birth or adoption of a child. | Withdrawals are more flexible. For one, you can withdraw contributions any time without penalty, since you've already paid taxes. As for withdrawals on earnings, they are tax-free if you’ve had a Roth IRA for at least five years and you are 59½ (or older). You can also withdraw tax-free at any age if you’ve had a Roth IRA for five years and qualify for certain exceptions, such as a first-home purchase. |

| Similarities |

| You can grow cash tax-free. |

| You can open an account regardless of your age, as long as you have earned income. |

| You can contribute up to $7,000 in 2024 ($8,000 if you’re 50 or older), even if you’re also contributing to a 401(k) or other company-sponsored savings account. |

What kind of IRA is right for me?

If you’re one of the many people thinking of starting a retirement savings account, it’s important to explore all of your options. Opening an IRA is simple, and most people invest in them to take advantage of their tax benefits, which help their money grow faster.

There are a few other kinds of IRAs in addition to the traditional and Roth, and each one has its advantages. Here's a breakdown of the different IRAs available to consumers:

| Type of IRA | Definition | Contribution limit |

| Traditional IRA | A traditional IRA allows your contributions to grow tax-deferred until you withdraw them upon retirement. There are two main types of traditional IRAs: deductible and nondeductible. Your financial situation will determine whether or not you get a tax deduction on your contribution. Non-deductible IRAs are similar to Roth IRAs in that contributions are made with after-tax dollars, but differ from them in that contributions aren’t limited by how much you earn. | For 2024, total annual contributions to your traditional IRA can’t exceed $7,000 ($8,000 if you’re age 50 or older). Your contributions can’t surpass your taxable compensation for the year. |

| Roth IRA | A Roth IRA is funded with after-tax dollars, meaning you’ve already paid taxes on the money you put into it. In return, your money grows tax-free. Once you retire and withdraw your savings, you won’t pay any taxes. | For 2024, total annual contributions to your Roth IRA can’t exceed $7,000 ($8,000 if you’re age 50 or older). Your contributions can’t surpass your taxable compensation for the year. |

| SEP IRA | A SEP IRA (or Simplified Employee Pension) is a type of traditional IRA designed for self-employed individuals and small business owners with few employees. Like traditional IRAs, the money in SEP IRAs is not taxable until withdrawn. Unlike traditional IRAs, these are funded with employer contributions only. | Contributions for tax year 2024 can be up to 25% of compensation or up to $69,000, whichever is less. |

| SIMPLE IRA | Unlike SEP IRAs, employees are allowed to make contributions to a SIMPLE IRA (or Savings Incentive Match Plan for Employees). SIMPLE IRAs are most commonly used by small business start-ups with under 100 employees. Additionally, employers are required to match up to 3% of the employee’s salary or make nonelective contributions of 2%, up to an annual limit of $290,000 for 2021. | Employees can contributes up to $16,000 from their salary to a SIMPLE IRA in 2024, plus a catch-up contribution of $3,500 for those over 50. |

| Spousal IRA | Spousal IRAs are intended for married couples and allow the working spouse to contribute to an account on behalf of a spouse that earns little or no income. To qualify for a spousal IRA, couples must file their income taxes jointly. It’s worth noting that spousal IRAs are not co-owned. | Each spouse may contribute up to the same limit as traditional IRAs or Roths ($7,000 for 2024). However, the total of their combined contributions can’t exceed the taxable compensation reported on their joint income tax return. |

Who can open an IRA?

You must have earned income from a W-2 job or self-employment to open an IRA, which means just about anyone with a job can open an IRA account, regardless of age.

A parent or legal guardian can set up an IRA for a minor through a custodial account. Once minors turn 18, or 21 in certain states, they will have full access to their IRA account.

Types of IRA rollovers

An IRA rollover — sometimes referred to as a "rollover IRA" — allows you to move money from your former employer-sponsored retirement plan to an IRA. Many people roll over their savings to consolidate former employer 401(k) plans and avoid the hassle of early withdrawal tax penalties.

However, there are some factors you should watch out for when rolling over your IRA. If done incorrectly, your rollover could be considered a distribution or early withdrawal and be subject to taxation.

Larry Sprung, founder and wealth advisor at Mitlin Financial, says there are two methods to avoid potential pitfalls.

“The easiest and least troublesome option is a direct rollover. With a direct rollover, you have the custodian of the current IRA write a check to the custodian of the new IRA for your benefit. And you as the IRA holder never take possession of the money,” Sprung says.

The second method is an indirect rollover, which will provide a check to your name that must be deposited within 60 days after you receive it. If you fail to do so, the money will be completely taxable. You also need to make sure you're not selecting the option to withhold taxes when you complete the indirect rollover application.

“If you withdraw money from a 401(k), the default is to withhold 20% for tax purposes, it’s very common for people to make the mistake of inadvertently withholding taxes unless they specify otherwise,” Sprung says.

While the IRS allows only one indirect rollover in any 12-month period, there is no limit to the number of direct rollovers you can request.

“If you're looking to rollover money and it's not a direct rollover, you really want to consult a wealth advisor, financial advisor or your CPA to make sure that you're filling out that paperwork properly," Sprung adds.

Depending on the plan you have, your investments could maintain their tax-deferred status when rolled over directly into an IRA account. Some qualified plans include 401(k), money purchase, profit-sharing and defined benefits plans. If you're considering a Rollover IRA, verify whether your account qualifies for a rollover.

Watch for early withdrawal tax penalties

You can withdraw early from an IRA prior to age 59½, but the money may be included as part of your gross income and subject to a 10% additional tax penalty. However, tax penalties are waived if your early withdrawal is for a qualifying distribution, or if you meet certain exceptions.

How do I open an IRA?

You can open an IRA account through a variety of financial institutions, including online banks.

Before getting started, take your time comparing providers. While the IRS doesn’t require a minimum contribution to get an account started, some providers may require $500 to $1,000 as an initial deposit plus servicing fees, depending on the account. Other institutions may have a lower minimum deposit requirement or none at all, so weigh your options.