What Is Compound Interest?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Compound interest is the interest generated on both the principal and the interest already accumulated. In the simplest terms, it’s interest on interest.

What You Should Know About Compound Interest:

- For investors, compound interest is your best friend as it generates interest on something other than the principal.

- For borrowers, compound interest is your worst enemy as it increases the debt because it’s calculated not only from the principal still owed, but from the unpaid interest previously generated as well.

- Calculating compound interest is complicated. How to calculate it depends on the type of financial instrument, the type of rate used (APR or APY), the number of compounding periods, and other factors.

The Difference Between Simple Interest and Compound Interest

Compound interest can be found in savings accounts, certificates of deposit, investment instruments, loans, and credit cards.

Simple interest is, as its name implies, easier to understand. It can be found in amortized loans such as car loans, student loans, and mortgages, or short-term personal loans.

The difference? Compound interest includes the interest generated on the principal and the accumulated interest from any previous period. Simple interest is the interest generated only from the principal. Therefore, if both simple and compound interests have the same rate, the interest generated will always be higher when compounding.

Both types of interest are calculated at certain periods which can be annually, semiannually, quarterly, monthly, daily, or any other period defined by the financial institution.

Let’s compare two scenarios with an initial principal of $1,000, both with a 5% interest rate that is calculated yearly, but one has simple interest while the other has compound interest.

| Calculating period | With Simple Interest | With Compound Interest |

| Initial amount | $1,000.00 | $1,000.00 |

| Amount after 1st year | $1,050.00 | $1,050.00 |

| Amount after 2nd year | $1,100.00 | $1,102.50 |

| Amount after 3rd year | $1,150.00 | $1,157.63 |

| Amount after 4th year | $1,200.00 | $1,215.51 |

Compounding interest creates an additional $15.51 in earnings.

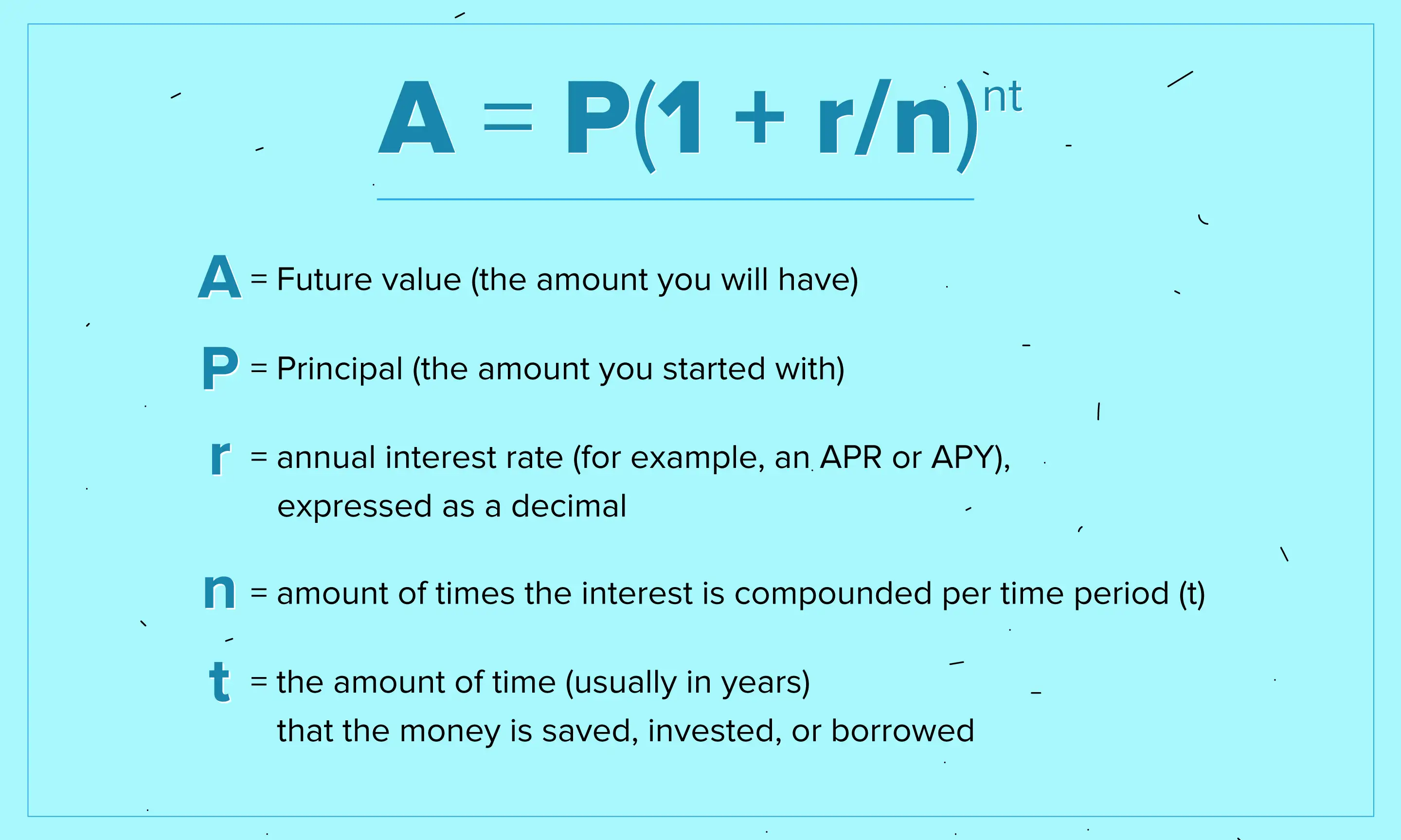

The Compound Interest Formula: A High School Math Refresher

Compounding Interest Pros and Cons

Depending on the type of financial instrument you’re managing, compounding interest can either help you or hurt you.

How Compound Interest Benefits Savings and Investments

Compound interest helps investors and savers grow their original amount faster because the growth is exponential.

Let’s say you opened an investment instrument for a 30-year term with a compounding 5% rate of return. The interest is calculated at the end of each year, giving the instrument 30 compounding periods. Let’s look at what the amount would be after every five year interval:

| Year | Starting amount for the interval | Compound interest accrued during five-year period | Total with compound interest at end of interval |

| 5 | $25,000.00 | $6,907.04 | $31,907.04 |

| 10 | $31,907.04 | $8,815.33 | $40,722.37 |

| 15 | $40,722.37 | $11,250.83 | $51,973.20 |

| 20 | $51,973.20 | $14,359.24 | $66,332.44 |

| 25 | $66,332.44 | $18,326.43 | $84,658.87 |

| 30 | $84,658.87 | $23,389.69 | $108,048.56 |

The total interest accrued for the whole 30 years is a whopping $83,048.56. The magic of compounding interest turned $25,000 into $108,048.56.

If the return were calculated using simple interest instead, the total amount would be $62,500, or about 72% less than with compounding interest.

Interest Rates in Savings and Investments

Though the above example is a nonspecific representation of compound interest in action, the truth is that compounding can come in different forms and be calculated in different ways.

Financial instruments such as certificates of deposit (CDs) or high-yield savings accounts also have compounding interest. However, while CDs generally have fixed interest rates, savings accounts tend to have variable rates that can change daily due to market fluctuations.

Investment instruments such as stocks and 401(k)s reinvest gains or interest to compound earnings. The compounding periods for these instruments and their formulas will vary but the principle is the same: exponential growth to benefit the investor.

How Compound Interest Affects Your Debt

In much the same way that compound interest can help you grow your earnings quicker, it can also balloon your debt if left unchecked. Nowhere is this more evident than with credit cards.

We can fill a book trying to explain how credit card interest is calculated. But let’s try to simplify the process and focus on how the compounding interest works in this case. Remember that credit card interest is only applied if the total amount of the credit card balance is not paid off during the next statement period.

For our purposes, we’re carrying a $1,000 credit card debt with a 19.99% APR.

How long would it take us to pay off the credit card, assuming no more purchases were made and no charges or fees were posted, if we only paid the minimum? And how much interest would be generated? What would our monthly payment be if we decided to pay off the debt in one year?

| Credit Card Balance | Monthly Payment | Payoff Time | Principal Paid | Interest Paid | Total Paid | |

| Paying the minimum | $1,000 | $35 | 40 months | $1,031* | $369 | $1,400 |

| Paying it off in one year | $1,000 | $93 | 12 months | $1,005** | $111 | $1,116 |

| *The last $35 payment is made when only $3.95 of debt is remaining. The excess of that payment is applied here to the principal. |

| **The last $93 payment is made when only $88.13 of debt is remaining. The excess of that payment is applied here to the principal. |

With a minimum payment, it would take us 40 months to pay off the credit card with $369 in interest payments during that time.

How can this be? For one thing, although credit card interest only appears at the end of the billing cycle, it is compounded daily. As we’ve learned, the more compounding periods, the faster the amount will balloon.

In this case, the $1,000 debt starts compounding interest on the first day and continues daily until it’s paid off.

If we wanted to pay it off in one year, we would need to pay $93 monthly to clear the debt. The compounding interest for that year would be $111.

The lesson here is that if you don’t pay your credit card statement debt in full when your due date arrives, you will be charged compounding interest on your next statement. Therefore, paying off high-interest credit cards is usually recommended to avoid swelling debt.

Using a Compound Interest Calculator

Although you’re already equipped with the knowledge of how compound interest works, you might want to learn how to calculate it. You might even try using an Excel formula. But calculating compound interest is complicated, and it’s usually not as easy as simply using the formula we provided above.

Different financial instruments might calculate it in various ways, and other times you’d need to do additional computations to figure out interest rates, such as with credit card APRs.

Nevertheless, you don’t need to do the math yourself to figure out how much you would earn in an investment account. There are many online compounding interest calculators that only require you to input the principal amount, length of the term, interest rate, and compounding frequency before calculating the compound interest.

FAQs About Compound Interest

What is the Rule of 72?

A fast and easy way to figure out how long it will take for an investment to double, given a fixed interest rate. All you have to do is divide 72 by the interest rate and you get the number of years.

For example, if you have a 6% interest rate, divide 72 by six and you get 12. You’ll double your investment in 12 years.

Although the formula is too reductive to get detailed information, the rule of 72 can help provide a quick and informal estimate to determine if an investment is worthwhile.

What’s the difference between APR and an APY?

Both are ways of presenting interest rates as percentages. But whereas APRs present the simple interest rate, APYs include compounding interest.

APR, or Annual Percentage Rate, is the rate for earning or borrowing money in a year while APY, or Annual Percentage Yield, is the same rate but with compounding periods integrated.

The more compounding periods there are, the higher the APY and the larger the difference with the APR.

Lenders will typically advertise their APRs for mortgages, loans, and credit cards, while investment products and savings accounts will promote their APYs.

Is compound interest good or bad?

It can be both. Investors love the gains that compound interest provides because it creates money without effort.

On the other hand, debtors despise compounding because they wind up paying interest on money they didn’t even use.