Modern Family Finances

- We're in Our 20s, Have $65,000 in Savings, and Want to Buy a Home. Can We Afford It?

- This Generation Has a Huge and Growing Student Debt Burden. It's Not Who You Think

- This Is How Much Debt the Average American Has Now—at Every Age

- This Last-Minute Tax Move Could Save You Thousands. Here's How to Do It

- This Couple Wants to Have a Baby in a Year. Can They Afford It?

Four out of five households no longer fit the old mom, dad, and their 2.2 kids mold. Time to throw out the one-size-fits-all financial plan and get advice tailored to your needs.

Like many thirtysomething couples with kids, Clint and Denielle Chaney of Edmund, Okla., face financial challenges. How to save for both college and retirement at the same time, for one. How to teach the children good spending habits, for another. Then, though, there are the concerns less universal to couples their age and more particular to their family situation—Clint’s sons from his previous marriage, CJ, 15, and Cadon, 11, live with them most of the time, and Denielle is expecting their first child together this April. These questions are tougher: What’s a fair amount for Denielle, an attorney, to contribute to major expenses for the boys? What’s the best way to make sure that if something happens to Clint, who owns a mechanical contracting company, everyone is clear about how much money he wants his older sons to inherit and how much goes to Denielle and their baby? “I don’t want to be making these decisions,” says Denielle. “I don’t want his ex-wife or other relatives saying, ‘Why did you take this or why didn’t you give them that?’ ”

Toughest of all: How can they ease the resentment that Denielle sometimes feels about not having an equal say in how the boys are raised when she is contributing substantially to their support? Says Denielle, “I’m not Clint’s sons’ parent, but I pay for them like a parent, and that can be hard.”

For decades the classic financial planning playbook has been based on a set of common assumptions: A man and woman meet, fall in love, marry, have kids, and build a life together. These days, however, millions of families find themselves following a different pattern that calls for new strategies. Over the past few decades huge demographic shifts have reshaped the American family to include blended households like the Chaneys, married gay couples, single parents, unmarried partners living together, and myriad other permutations. Shifting TV icons tell the story: Ozzie, Harriet, and the Cleavers yielded to the Bradys and then to the Gilmore girls, before expanding to include Jay and Gloria, Cam and Mitchell, and assorted Kardashians.

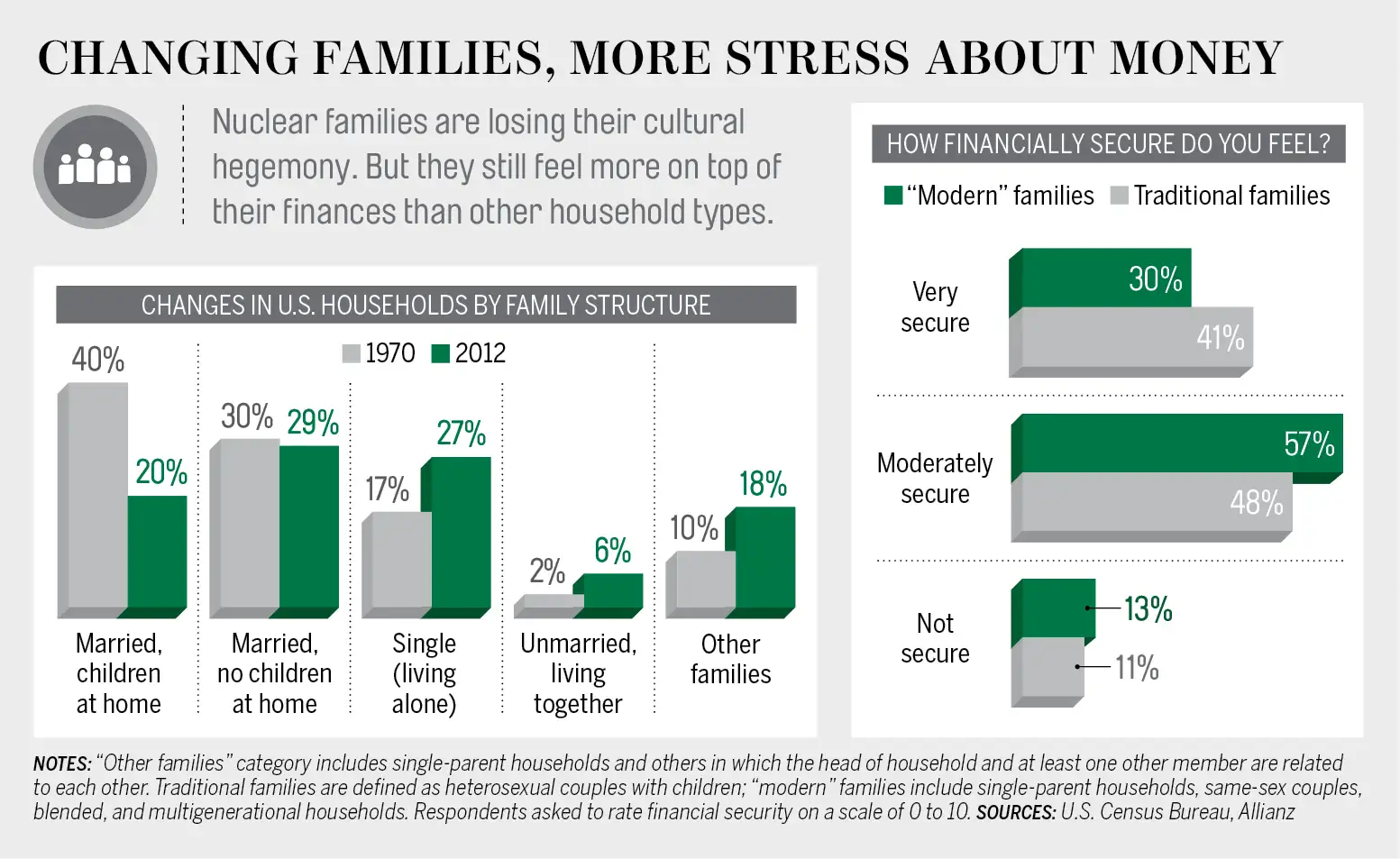

The shift is so profound, in fact, that families made up of two heterosexual parents with kids under 18 now comprise only 20% of households, down from 40% in 1970, the Census Bureau reports. With those changes have come new financial challenges. Who pays for what in nontraditional households? How do you handle jointly owned property if you’re not married? Who will take care of you if you’re an older single and you fall ill? How do you get an ex to pay up? “We know that families are not from the Leave It to Beaver model anymore,” says Miramar Beach, Fla., financial planner Patrick McDowell, “but our planning process hasn’t evolved to reflect those changes.”

All those unanswered questions can add to the money stress that many of these households already feel. According to a 2014 study by Allianz, only 30% of what the financial services firm termed “modern” families feel a high degree of financial security, vs. 41% of traditional families made up of a mom, dad, and their offspring under 21. The nontraditional families were also more likely to say they live from paycheck to paycheck and less likely to feel knowledgeable about how to reach their goals.

To be sure, there are basics that are the same for all households. Everyone should have an emergency fund equal to at least three to six months of living expenses. Everyone needs health insurance. And, of course, you ought to be saving regularly for retirement, ideally in a 401(k) or IRA.

From there, though, your needs are largely shaped by your household’s unique structure. For those of you who don’t fit the nuclear family mold, the story that follows—the last in a three-part series about the impact of demographic changes on how families manage their money—offers solutions to the most common challenges you’re likely to face.

[time-anchor title="Blended Families"]

Biggest Challenge: Unpacking all that financial baggage

Four decades after Mike and Carol Brady joined their broods in cutting-edge TV matrimony, blended families—a couple and their kids from current and previous unions—have become utterly commonplace. While only 23% of the boomers who grew up watching the Bradys have a step-sibling, 44% of millennials do.

What hasn’t changed: how the financial baggage that remarrying spouses carry, combined with the tensions of providing for both biological children and stepkids, can weigh down even the happiest bunch. In the Allianz survey, 43% of blended families said that they have difficulty overcoming issues with money that they or their partner brought into the relationship; a third reported that inadequate support from an ex makes it hard to save. “Most people want to ‘do right’ by all parties involved, but it’s tough to do that without alienating someone,” says planner McDowell.

Plus, in blended households financial planning tends to be a singular, rather than a joint, pursuit. In the Allianz study, two-thirds of the adults in blended families said they were focused on individual needs and goals rather than the household’s.

65% of remarriages involve children from previous marriages

Then, too, targeted advice can be hard to come by. “Our laws and policies are still based on the idea that everything you acquire as a couple is acquired together, and that your financial habits develop along with your kids’ needs,” says Margorie Engel, former president of the Stepfamily Association of America, “With stepfamilies, it’s reversed. Wham! You’ve got the kids. The honeymoon occurs after the kids leave the nest.”

The Solution: Make managing money a team sport.

Don’t confuse equal with fair, says Paula Bisacre, publisher of Remarriageworks.com. Many factors dictate the financial rules and roles that are right for your family, such as how much support you give to or get from an ex, and how much the various adults in question earn. You and your spouse don’t have to contribute the same amount for household bills or each other’s children, and may have different policies about what your respective kids get as gifts or for allowance. And that’s okay, as long as you explicitly work out the system that feels right to both of you, particularly when it comes to major expenses for each other’s children. It’s no problem if your ex does things differently, says Engel: “As long as the rules are clear, the kids will adapt.”

To avoid friction, some blended families find it helpful to maintain separate accounts. But that can also accentuate the feeling that you’re not working together as a team, so have a heart-to-heart about what works best for your household. Clint and Denielle Chaney, for example, decided to combine their finances completely. “When I came into the marriage, I felt like such an outsider,” Denielle says. “If I didn’t share in the family finances, I’d feel like an outsider even more. I didn’t want it to feel like it was him and his kids and me and my dog.”

And Don't Forget...

Make saving a priority. With more expenses to handle than the typical household, blended families save far less, if at all, Allianz reports. Yes, it’s tough, but signing up for automatic investing plans at work or through a bank or brokerage can push you to adjust your budget to incorporate savings.

Be savvy about college aid. The income and assets of stepparents in the household with primary custody are factored into financial-aid formulas, says Mark Kantrowitz of Edvisors.com. If you split custody fifty-fifty with your ex, have the lower earner fill out aid forms.

Spell out bequests. Want to make sure your biological kids get their fair share after you’re gone? Set up a QTIP trust to leave some assets directly to your kids while also providing for your spouse.

[time-anchor title="Domestic Partners"]

Biggest Challenge: Making the world see you as a pair

44% of adults have cohabited at some point in their lives

A few decades ago, unmarried people were those who hadn’t found true love, or gay couples who were legally prohibited from tying the knot. No longer. According to the Census Bureau, there are 8 million unmarried couples who are living together, a 25% increase just since 2007.

Increasingly, employers are recognizing these committed relationships. Nearly half of companies with 500 or more workers now offer some benefits to same-sex domestic partners, up from about a third in 2010, according to Mercer, and many extend those rights to opposite-sex partners as well. Several states, the District of Columbia, and many local governments also offer legal standing to domestic partnerships, or called civil unions.

Still, if you’re living together without the status of marriage, you typically forgo more rights than you gain. You aren’t eligible for survivor benefits from retirement plans or Social Security, for example, and transferring or bequeathing assets to each other may trigger a tax bill that married couples don’t face. You aren’t the default decision-maker in case of ill health or death, and you have no automatic rights to your loved one’s property and other assets if you split up. Partners of people who are self-employed or work at a small company are more likely not to have access to their health insurance or other benefits. And even if you can get on her plan or vice versa, the value of those benefits will be counted as taxable income to you, not pretax income, as would be the case for married folks.

The Solution: Create a legal partnership

Register your domestic partnership or civil union with the proper authorities, if that option is available. Ensure that your partner can make health care or financial decisions on your behalf if something happens to you by completing the paperwork to name him or her as your power of attorney for health care and finances. Both of you need wills to make sure you each inherit the assets you want the other to get. Concerned that your blood relatives may contest the will? Create a revocable living trust, says Atlanta estate planning attorney Richard Barnes. Expect to pay an attorney from $1,500 to $2,500 in setup fees, but the trust can’t be as easily fought in court.

What if you break up? While divorce laws aim for an equitable division of assets, unmarried partners generally have no claim on each other’s possessions. So keep a portion of your money in an individual account and keep non-mortgage debts separate; if you co-sign for a loan or a credit card, you’ll be on the hook for the entire amount if your partner refuses to pay his share. Also consult a lawyer about a life partnership agreement, similar to a prenup, that spells out who owns what and how your assets should be divvied if the relationship ends.

And Don't Forget...

Know where you stand. You can usually find out whether your city or state offers domestic partner privileges and what it takes to qualify for them by contacting the agency that handles marriage certificates, often the county clerk’s office or bureau of vital statistics. Your HR department can tell you what benefits are available at work to you and your partner. If you’re both employed at companies with good coverage, though, you may be better off each going your own way, since the value of benefits obtained through your partner’s work will be added to his income, making this a potentially costly way to get insurance.

Decide how to co-own your home. A joint title with rights of survivorship is usually the best arrangement, since it allows your partner to automatically inherit the home, says Chicago real estate attorney Sam Tamkin. If one of you has contributed a lot more, however, you can use a tenants-in-common title, which lets each of you specify a percentage of ownership. Then outline inheritance wishes in your will.

Name beneficiaries. Your partner can’t roll over your IRA or 401(k) into her account. However, thanks to a 2006 law change, she no longer has to immediately take the money out as a lump sum; she can take distributions (and pay the tax bill) over time.

[time-anchor title="Single Household"]

Biggest Challenge: Figuring out who will catch you if you fall

The single life, it seems, is trendy. A record share of Americans have never been married, according to Pew Research; among single adults ages 25 to 34, roughly one-third say they are not sure if they ever want to tie the knot. When that’s combined with divorced and widowed folks who haven’t gotten hitched again, 27% of households consist of one person, up 10 percentage points since 1970.

Financially speaking, living without a partner has perks. You get to decide whether to scrimp or spend, unfettered by your significant other’s desire for a Mercedes or a McMansion, and often without the draining expenses of kids. On the other hand, you lose out on some of the reduced costs built into couplehood, such as a shared home or car and amplified savings and Social Security benefits. “When I was married, both my spouse and I were able to save at a good clip,” says Donnell Butler, 41, of Lancaster, Pa., a dean at Franklin and Marshall College who has been on his own for four years now. “It’s much harder now that I’m paying for everything on my own.”

20% of adults have never been married, up from less than 10% in 1960

The toughest nut, though, is when things go wrong. Lose your job? “Single people have no backup income,” says Jan Cullinane, author of The Single Woman’s Guide to Retirement. Become ill or incapacitated, which gets more likely as you age? Without a built-in caretaker, you could be on your own.

The Solution: Line up a reserve team.

Err on the side of caution when it comes to your emergency fund, and aim to have enough to cover nine months to a year’s worth of living expenses. Disability insurance is critical. If you can’t get coverage through your employer, spring for an individual policy if possible. To lower the cost, opt for a longer period before you collect benefits—say, 180 days instead of the more typical 90.

You may also want to spring for a long-term-care policy, which would cover the cost of in-home care as well as a nursing home. “When there’s no obvious caretaker, people want to avoid being a burden,” says Covington, La., planner Lauren Lindsay. And be sure to grant someone you trust—say, a sibling or close friend—power of attorney and the right to act as your health care proxy if you’re not able to handle your finances or direct your own care.

And Don't Forget...

Skip life insurance. No dependents? You likely don't need a policy.

Pump up retirement savings. Unlike married couples, you won't be able to tap a partner's Social Security or pension. One plus: When your peers with kids are struggling to pay college bills, you'll have bandwidth to funnel tons into your 401(k).

Build your legacy. Without clear heirs, you need a will to spell o ut what you want to happen to your home and other assets when you die. Otherwise the courts will make those decisions for you.

[time-anchor title="Single Parents"]

Biggest Challenge: Juggling higher expenses on lower income

Raising a child without a live-in partner is often as tough financially as it can be emotionally. According to the National Bureau of Economic Research, the family income of children whose parents divorce and remain divorced for at least six years falls by 40% to 45%. “Even when a divorce is pleasant,” says planner Lindsay, “the financial impact is severe.” The Allianz survey further backs up that view: Just 45% of single parents said they were on track for a comfortable retirement, vs. 57% of traditional families, while more than three-quarters reported being stressed by trying to simultaneously save for retirement and their child’s college tuition.

While alimony or child support can help defray day-to-day expenses, it often doesn’t make a meaningful dent in the killer cost of childcare, which is often an unavoidable expense for single parents with younger kids, says Lindsay. Moreover, as children grow older, many bills pop up—piano lessons, orthodontia, summer camp—that may not have been anticipated and accounted for in the original divorce agreement. “People create a divorce decree based on a small child’s expenses, and then things change,” Lindsay notes. Plus, support agreements generally end when the child turns 18—often without having worked out how college bills will be handled.

The Solution: Put yourself first.

Understandably, single parents are often deeply concerned about making sure their kids don’t get shafted when it comes to their future. In the Allianz survey, nearly half of the single-parent respondents named “saving for my kids’ education” as their main motivation for developing a financial plan, compared with only a quarter of other modern families.

28% of children under age 18 live with a single parent

So this will be tough to hear and perhaps tougher to implement, but it is your best path nonetheless: In the college-vs.-retirement savings quandary, your retirement wins. For one thing, as Rapid City, S.D., financial planner Rick Kahler points out, you can’t count on splitting retirement living costs with a significant other. And if you had to divide 401(k) or IRA assets with your former spouse, you’re probably further behind than you’d otherwise be at this stage of your life. Meanwhile, your child may qualify for financial aid (especially if your income and assets are lower as a result of your divorce) or can borrow as need be. And if absolutely necessary, you can also take out a loan against your 401(k) or withdraw money penalty-free from an IRA to pay for college, while these assets won’t be counted in the federal aid formula.

To get savings for both college and retirement on track, you may need to have a frank talk with your child about cutting back. That’s what librarian Joy Birdsong, 52, of Brooklyn did with her daughter, Savannah, 12, after filing for divorce last year. “All my assets have to be split,” says Birdsong. “I am responsible for Savannah’s upkeep, and preteens in 2014 have a lot of needs.” Birdsong sat down with Savannah and let her know that the latest iPhone and frequent trips to Starbucks were out. Says Birdsong: “I didn’t want to scare her, but I did let her know the situation was serious.”

And Don't Forget...

Renegotiate with your ex. Look for equitable ways to split child expenses that weren’t outlined in your divorce agreement. An informal talk may suffice if you have a good relationship; enlist the aid of an attorney if you anticipate pushback.

Take care of the what-ifs. Create or update your will to name a guardian for your child (if your ex is not in the picture or dies before you). A testamentary trust will enable you to appoint someone to manage money you’ve left to your child on his behalf until he is no longer a minor.

Be tax-smart. Alimony is taxable income to the recipient; child support is not. Filing as a head of household usually results in a lower tax rate than filing as a single, says Bonnie Lee, author of Taxpertise.

[time-anchor title="Same-Sex Married"]

Biggest Challenge: Straddling two very different legal realities

For most of their 34-year relationship, Steven Rabinowitz, 69, and Mark Quiello, 59, jumped through hoops to ensure they had as many of the protections afforded married straight couples as possible. They drew up wills, health care proxies, and powers of attorney; registered their domestic partnership; maintained joint accounts; and worked with an attorney to title their home and structure estate plans. Then, last year, New Jersey, where the men live, became one of the 32 states that have legalized gay marriage, and the two tied the knot. Says Quiello, a senior consultant with a major telecom company (Rabinowitz is a retired textile designer): “We feel more secure now.”

35% of same-sex couple households consist of married partners

Among the biggest changes for the two men and the more than 250,000 other same-sex married couples in the U.S.: Since the Supreme Court struck down the Defense of Marriage Act last year, gay spouses in states that have legalized such unions are now entitled to the same federal benefits as heterosexual married couples. That means access to spousal and survivor Social Security benefits; the ability to transfer or bequeath assets to each other without paying taxes; and protected status as a beneficiary when it comes to pensions, retirement accounts, and annuities, among other rights. States confer additional protections, such as rules guiding a fair division of assets in case of a divorce.

Yet if you work in, move to, or have other dealings in a state that doesn’t recognize same-sex marriage, you still need to take precautions. Consider: A married gay couple who live in Illinois can make medical decisions on each other’s behalf in their home state, but not if one partner is in a car wreck and hospitalized in neighboring Missouri, where their marriage isn’t recognized. Filing a tax return for a state where the union isn’t legal is tricky too. “There are still many complications that heterosexual couples don’t face,” says Harrisburg, Pa., planner Tracy Burke.

The Solution: Jump through the right hoops.

Better safe than sorry: You and your spouse both need a health care directive and a power of attorney so that you can make medical and legal decisions on each other’s behalf no matter where you live, work, and play, says Rockville, Md., planner Joshua Hatfield Charles. If one or both of you work in a state that doesn’t recognize your marriage, you’ll most likely have to file separate state tax returns in addition to a joint federal return, says Janis Cowhey, co-leader of the LGBT practice group at the accounting firm Marcum LLP. Have a second home in a state where your marriage isn’t legal (say, Florida)? You need a joint title to ensure that if you die, your spouse automatically inherits the property.

And Don't Forget...

Look for tax breaks. Filing a joint return often results in a higher tax bill, says Cowhey. Max out pretax contributions, consider muni bonds, and favor low turnover funds that generate little in capital gains in taxable accounts.

Reapply for insurance. Married couples often qualify for discounts on homeowners and auto policies.

Put good fortune to good use. Gay families had higher average incomes than all other households in the Allianz study. Crank up your savings rate, then indulge a little. You’ve earned it.

See the previous stories in the Love & Money series:

7 Ways to Stop Fighting About Money and Grow Richer, Together

How to Avoid Paying for Your Kids Forever