7 Ways to Stop Fighting About Money and Grow Richer, Together

- We're in Our 20s, Have $65,000 in Savings, and Want to Buy a Home. Can We Afford It?

- This Generation Has a Huge and Growing Student Debt Burden. It's Not Who You Think

- This Is How Much Debt the Average American Has Now—at Every Age

- This Last-Minute Tax Move Could Save You Thousands. Here's How to Do It

- This Couple Wants to Have a Baby in a Year. Can They Afford It?

When she graduated from college two decades ago, Jehan Chase had traditional expectations about money and marriage. She figured she’d soon fall in love, settle down, and, once she was wed, turn over managing the family’s finances to her husband. “I thought it would be nice not to have that responsibility,” she says. But life hasn’t followed the script. Instead, Jehan, 44, stayed single until two years ago; by then she’d built a successful career as a government attorney and had become accustomed to managing her own money. After her marriage to Seth, 40, an advocate for a nonprofit who makes a good deal less than she does, Jehan continued to take the lead in managing money for the Alexandria, Va., couple—partly out of convenience, since Seth already had his hands full taking care of his disabled mother and sister, and partly because she didn’t want to cede control. She says, “I’m comfortable being in charge of the finances.”

For his part, Seth, who had been the bigger earner in his previous marriage, says the income role reversal took some getting used to. Now, though, he’s happy with the way the couple manage their money. “Jehan works in a field that pays better than the one I work in, so the income difference isn’t an issue for me,” he says. “She seems to really like doing the finances—and she’s better at it than I am.”

The growing number of wives who, like Jehan Chase, make as much as or more than their husbands is having a profound impact on the way that married couples manage their money and how they feel about their financial union. That’s the clear takeaway from a new national Money survey of more than 1,000 married adults ages 25 and older. The responses reveal that as wives’ economic contribution to the household grows—on average, women in dual-earner households now bring in about half of the family income and nearly a quarter of wives earn more than their husbands —every aspect of couples’ lives together is affected. That means not just how they save, spend, and invest but also what they worry about, what they fight about, and even how happy they are in their relationships. “Traditionally women’s income was ‘pin money,’ used for extras like shoes or kids’ braces,” says Liza Mundy, author of The Richer Sex. “Now many families have fully integrated the woman’s earning power into their financial planning. That’s a real transformation.”

What’s clear from the Money survey is that this transformation extends far beyond the numbers in the family’s bank account. When women earn as much as or more than their spouses, the results show, they take a far more active role in financial planning, getting deeply involved in everything from budgeting to retirement planning. They bring a more collaborative style to managing the household’s money. And husbands, by and large, appear pleased with the results. “These days women are engaged in all aspects of personal finance,” says New York University sociology professor Kathleen Gerson, who is working on a study about how contemporary work habits are reshaping family life. “It’s not only acceptable; it’s expected.”

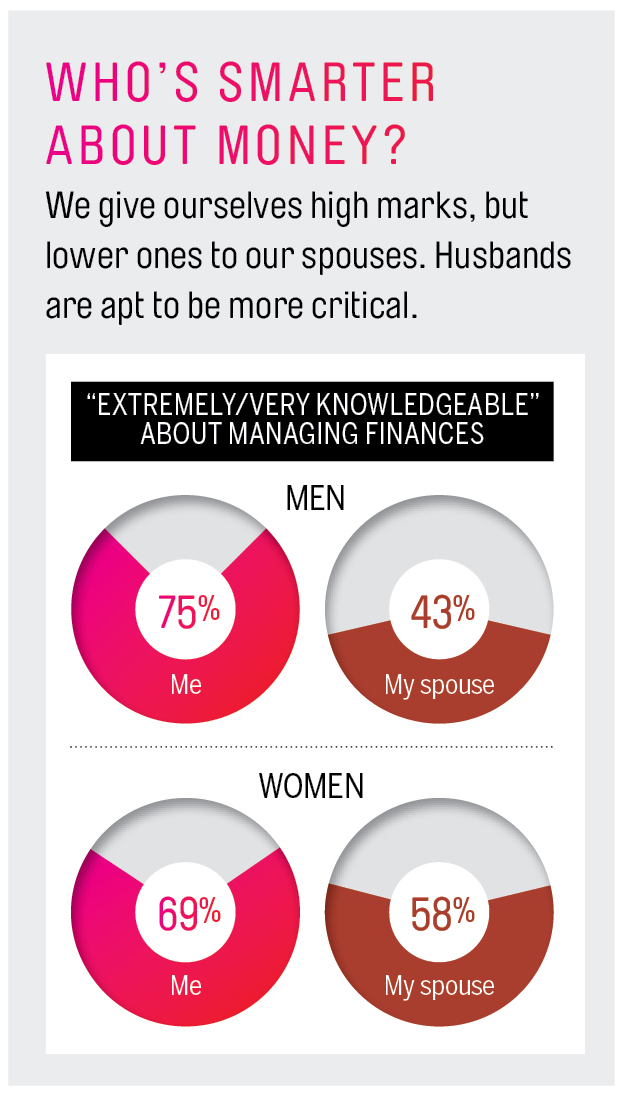

These new dynamics, however, are also creating new tensions, as women feel heightened financial stress, men come to grips (or not) with shared decision-making, and both spouses struggle to figure out a fair division of labor (financial and otherwise) at home. Meanwhile, no matter how much the husband or wife earns, the survey found that money remains the top source of friction for couples overall, with spending a particularly contentious issue. And while spouses overwhelmingly think they’re in sync about their finances, the survey results also make clear that when it comes to money, they are typically anything but: Husbands and wives often don’t agree on the roles they play and the financial skills they have, or understand what really matters to their partner.

How can you ensure that this conclusion doesn’t describe your relationship? The insights and advice in the story that follows—the first in a three-part Money series that looks at how major demographic shifts are changing the finances of American families—will give you a better understanding of the challenges you face and the ways that you and your spouse can work together to build a richer, happier life.

Finding No. 1: Women who bring home the bacon like to cook it too.

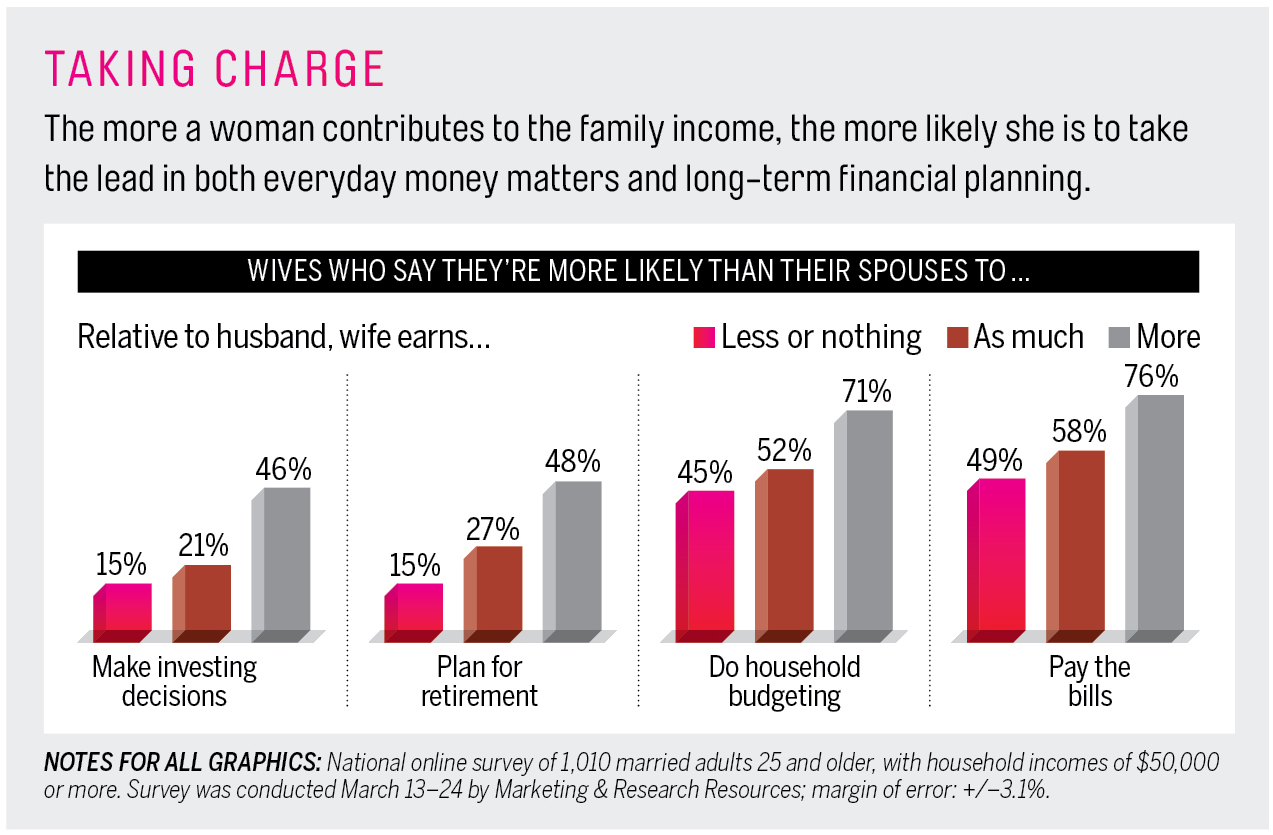

The more a wife earns relative to her husband, the greater her involvement in all aspects of the family’s finances—especially the responsibilities that have traditionally been the purview of men, such as investing and retirement planning. That insight from the Money survey makes intuitive sense and may not be surprising. What is startling: the extent to which a woman’s contribution to the family’s income drives her financial participation, either as chief decision-maker or in concert with her spouse, and the effect it has on how she feels about managing money. “There is a definite relationship between a woman’s earnings and her confidence with finances,” says psychologist and certified financial planner Brad Klontz, co-author of Mind Over Money.

Consider: About 80% of the wives in our survey who earn more than their husbands say they’re very or extremely knowledgeable about financial matters, compared with just over half of those who earn less (and lower-earning women are three times as likely to say they know very little). That greater confidence translates directly into action. For instance, wives who are the larger breadwinner are roughly three times as likely as lower-earning women to take the lead in investing and retirement planning. They’re also more apt to be in charge of the household budgeting and bill paying, and to buy insurance for the family.

And it’s not just the women who say so. Husbands in the survey who didn’t earn as much as their wives were far less likely to say they were the primary decision-maker, although they remained a lot more involved than wives who earn less or no salary in nearly all areas. “Money management is still a role men pride themselves on,” says Seattle sociologist Pepper Schwartz, co-author of The Surprising Secrets of Happy Couples.

What’s apparent is that while men typically feel ownership in the family’s finances no matter how much they earn, women often need to be making a direct and substantial monetary contribution before they feel the same. “I do the research on our investments and spearhead those decisions, and a lot of that does have to do with the fact that I make more,” says Amanda Austreng, 27, a medical lab scientist in St. Paul who out-earns husband Nick, 26, a preschool teacher. “I want to make sure my money is doing as much as it can.”

For greater harmony:

- Manage based on interest, but decide together. Who earns what is a lousy way to determine who does what when it comes to your money. One person is usually more interested in financial chores or available to handle them, and as long as you agree on who is best suited to a particular responsibility, it’s fine for that spouse to take charge of, say, paying bills, picking mutual funds, or preparing the taxes. Just be sure to draw a clear distinction between tasks and decisions, says psychologist Jonathan Rich, author of The Couple’s Guide to Love and Money: “No one has the right to single-handedly guide the family’s goals.”

- Master the basics. While it’s understandable that women step up their game as they earn more, both partners, regardless of how much they earn individually, need to be clued in about the family’s finances, says Atlanta financial planner Mary Claire Allvine. It’s particularly dangerous for women to remain in the dark, as they tend to outlive men:“I see my older female clients having wealth management thrust on them, and it’s uncharted territory,” Allvine says. Schedule uninterrupted time, a minimum of twice a year, to sit down with your spouse and review what you own and what you owe. Then discuss how these numbers jibe with your immediate and future financial goals.

Finding No. 2: The spouse who earns more drives the financial style.

When husbands are the bigger earners, they take the lead in managing the couple’s money—especially in their own estimation. When asked who is primarily responsible for major decisions about retirement planning and portfolio management, for example, six in 10 higher-earning men claimed the title, with only 39% saying they share the role with their wife.

By contrast, in the view of both husbands and wives, households in which the woman makes the same as or more than her spouse have a collaborative money management style—“We decide” vs. “I decide.” Overall, nearly two-thirds of respondents from these families say they share financial decision-making with their partner, compared with less than half from households in which the man earns more. Perhaps most telling: Only 4% of lower-earning husbands feel they’re not a financial decision-maker in the family, vs. 28% of lower-earning wives.

These gender-driven differences in approach echo the contrasting professional styles that researchers have observed in the workplace, says University of Maryland sociology professor Philip Cohen. He notes that female managers tend to be more collaborative and relationship-oriented than their male counterparts. When it comes to money, higher-earning women may also work harder at being inclusive because they worry that their husbands will be unhappy in a nontraditional family role. Says Liza Mundy: “Female breadwinners are more likely to want to empower their husbands.”

That rings true for Roopal Carbo, 40, of Yorktown Heights, N.Y., a pharmacist whose husband, John, 41, is a stay-at-home dad to their three kids, ages 6 to 11. “My husband thinks that because I earn the money, I should decide where to spend it,” she says. “But just because I earn it doesn’t mean he’s not playing an important role in the family and that he doesn’t have just as much right to voice concerns.” John says it took him a few years to get comfortable offering his opinions on financial matters. “My wife still drives the major decisions, but now we discuss everything,” he says. “Each year we get better at this, and the conversations are easier to have.”

For greater harmony:

- Play to your combined strengths. Sorry, guys, but when it comes to money, a joint approach typically trumps managing solo. Besides the fairness factor (income power shouldn’t automatically confer decision-making power), there’s a practical reason: Men and women, it’s been well documented, often have different but complementary financial skills that work better together than separately.

Men, for instance, are usually more willing to act when it comes to investing and planning and to take risks for greater gain. That works to temper women’s often expressed conservatism. Men are also prone to overconfidence, which can lead them to trade excessively, ultimately hurting their investment returns. Women are more patient, buy-and-hold investors and tend to thoroughly research each financial decision before they act. “Balancing your styles is ideal,” says psychologist Jonathan Rich.

Finding No. 3: Husbands are happiest when their wives earn as much or more.

The downsides of marriages in which women are the bigger breadwinner have been well catalogued in research and by the media. The husbands suffer from bruised egos and feelings of emasculation; the spouses fight more than other couples, have lousy sex lives, and are more prone to divorce.

The problem with these characterizations? They’re not necessarily accurate. The most publicized recent studies are based on data from couples interviewed during the early to mid-1990s, missing a generation’s worth of shifting expectations and experience when it comes to working women and marriage. In fact, the responses from the Money survey suggest unions in which women earn as much as or more than their husbands are at least as happy and as hot as marriages with a traditional earner relationship—and, in some cases, more.

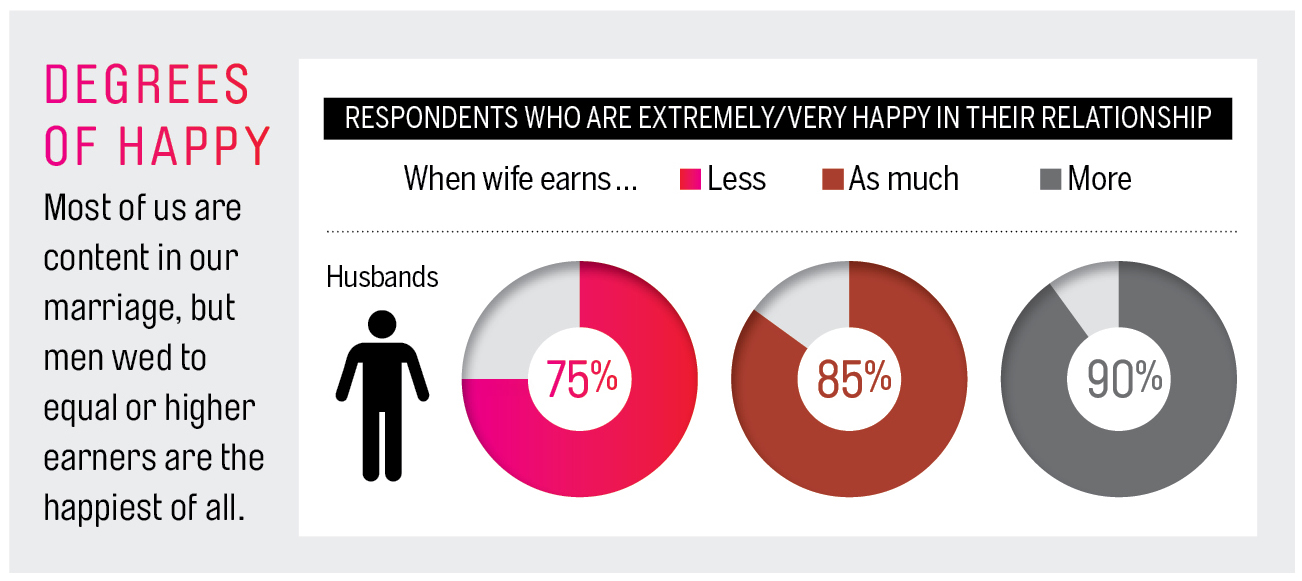

Take marital satisfaction. Spouses in households where women earn as much as or more than men were as much in love as everyone else (six in 10 gave their relationship a five— “very much in love”—on a scale of one to five). They were a bit happier—83% were very or extremely happy, vs. 77% of families in which the wives earned nothing or less than their husbands. As for heat, marriages in which the partners earn roughly the same took the prize: They reported the best sex life, with 51% saying that their romantic encounters were “very good” or “hot,” vs. 43% of spouses overall.

What’s more, the most satisfied partners of all were the husbands in egalitarian and female-breadwinner marriages. For example, 56% of men wed to women who make as much as they do characterized their sex lives as “hot” or “very good,” vs. 43% with wives who made less. Men married to women who earn the same or more also expressed the greatest happiness with their relationship (see below). Psychologist Klontz theorizes that these husbands may be a self-selecting group: “Men who are attracted to higher-earning women probably desire more egalitarianism in their relationships.” For her part, sociologist Schwartz says her studies have also found a strong link between egalitarianism and sexual satisfaction.

The results of the Money survey may also reflect ongoing changes in men’s socialization and expectations, says Cohen at the University of Maryland. “Men are now being raised on the assumption that the woman is going to have a career, so there’s no shame that she ‘has’ to work,” he says. “They might not want their wife to make more, but they also might not care if she does.”

The tough economy of the past several years may also play a role. “We have found that it is burdensome for many men to have full responsibility for the family’s income,” says Ellen Galinsky, president of the Families and Work Institute. Andy Wen, 49, a music professor in Bryant, Ark., whose wife, Debra, 60, a special-education teacher, earns roughly the same salary, agrees. “Because neither of us is the main provider, there is no imbalance of power in our relationship, and it takes some of the pressure off both of us,” he says.

For greater harmony:

- Emphasize the team, not the score. What’s driving satisfaction in more egalitarian marriages probably has less to do with who has the bigger W-2 and more to do with both partners feeling they are working in tandem to build their family’s security. Neither one carries the burden alone. Make financial togetherness easier by ensuring that all information is relayed jointly, suggests Manisha Thakor, co-author of Get Financially Naked: How to Talk Money With Your Honey. “If you have investments, for example, make sure both your names are copied on the trade confirmations,” she says. You can also set up your online banking accounts so that you each get the same alerts—say, when a deposit over a certain amount has posted to your account or a bill payment is due.

Finding No. 4: Female breadwinners are feeling the stress.

Not everything is peachy in marriages where women are the bigger breadwinners. Husbands in these relationships may be happier than most, but the wives? Well, not so much. Higher-earning women are not as likely as other spouses to say they’re very much in love (58% say so—15 percentage points less than men married to higher earners). These wives worry considerably more about finances than men and lower-earning women do, and they are also more apt to identify money as an area of tension in their relationship (one particular sore point cited by nearly a quarter of these wives: their husband’s lack of career ambition).

What’s going on here? In a word, pressure. Many studies have documented the strain that working women feel juggling their jobs while having to keep up with their regular chores at home. Add the stress of being primarily responsible for the family’s income, and the reasons for female-breadwinner discontent don’t seem that difficult to fathom.

In fact, the Money survey tapped into this resentment: In marriages where the wife earns more, household chores rivaled money as the subject couples fight about most frequently, and arguments about grocery shopping, cooking, and taking out the garbage were more frequent than in homes with a male primary breadwinner. That’s true even though men in these relationships seemed to be doing considerably more around the house than their higher-earning counterparts, and female breadwinners were doing less than lower-earning women and stay-at-home wives.

Part of the problem, says San Diego psychologist and marriage counselor Jonathan Kramer, is perception. “Men often magnify the extent to which they’re doing chores at home,” he points out. Meanwhile, some wives may not recognize how much more their husbands are doing, especially if the guys do the cleaning, shopping, cooking, and child rearing differently than the woman would do them herself.

Whatever the reasons, women like Ashley Papke, 31, an office manager in St. Louis who makes almost twice as much as her attorney husband, Erik, 34, are feeling the weight keenly: “It’s a constant struggle to be the best at my job, the best mom, the best wife, the best financial planner for our lives, the best homeowner, the best coach,” she says. “Sometimes I feel like there is so much expected of me that I may just explode.” Though the Papkes theoretically divide financial-planning tasks, Ashley says she feels “more responsible” for the family’s financial success. “Erik is helpful, but since I earn more and worry more, I feel it’s on my shoulders,” she says.

For greater harmony:

- Outsource what you can. Yes, a monthly or biweekly housecleaner, and takeout or prepared foods, can get expensive. Still, if you can afford at least a few time-and-energy savers without sacrificing important goals, go for it, says Money contributing editor Farnoosh Torabi, author of When She Makes More (check out an excerpt here). Harmony on the home front is worth something too.

- Be appreciative. Ladies, your husband may not cook, clean, and take care of the kids as you would. When he takes on a task, though, you have less say in how it gets done and vice versa. Say “Thank you” and move on.

Finding No. 5: Spending is everyone’s hot-button issue.

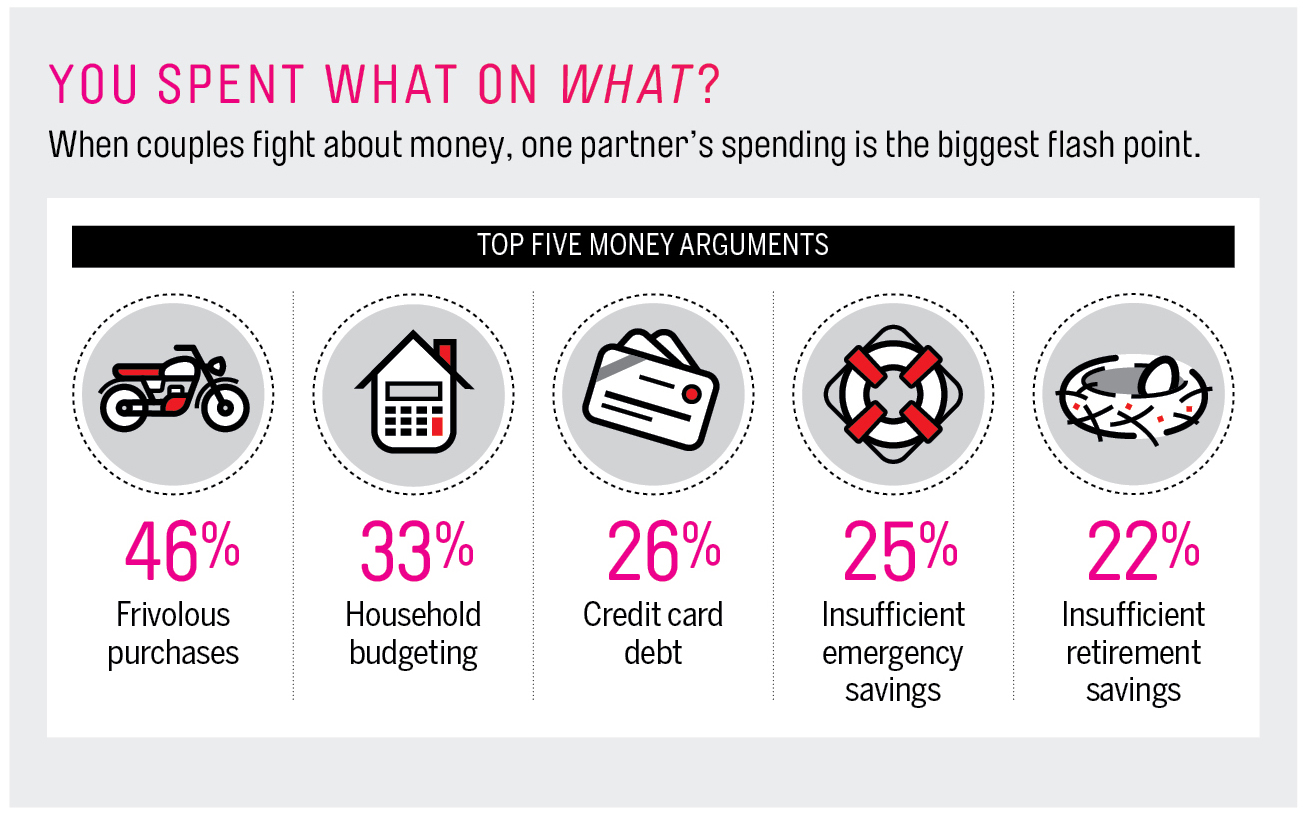

No matter which spouse earns more, money has traditionally been the greatest source of friction for couples, and our survey found the same: Money is the topic that spouses argue about the most, ahead of household chores, spending quality time together, sex, snoring, in-laws, and what’s for dinner.

The most contentious issue was spending, with 46% of respondents citing frivolous purchases as the top cause of money fights. And both men and women think their partner is the one with the bad spending habit.

Still, the more wives contributed to the family income, the less an issue spending appears to be. That’s what Lisa Dieter, 33, a certified financial planner in Mettawa, Ill., learned when she swapped breadwinning roles with husband Matt Miller, 38. Until last year, when Miller launched an online dining guide business, he had earned about 70% of the household income as the manager of an online certification website. “I used to check with him first before making a big purchase,” says Lisa. “Now it’s my income, so I feel like I can make my own decisions. Before I felt like he had the final say. Now I do.”

For greater harmony:

- Work off the facts. The majority of us marry our money opposites, says Scott Palmer, co-author with his wife, Bethany, of The 5 Money Personalities: Speaking the Same Love and Money Language. If you’re a worrier and saver, you may find it hard to understand why your free-spending spouse craves a pricey vacation—and she, in turn, may be frustrated by your claims that you can’t afford to take one. Remove the emotion from the discussion by looking at hard numbers to figure out whether your spouse’s spending is actually interfering with your ability to, say, build an adequate emergency fund or save for retirement. If so, discuss it, framing the conversation about the goal (a positive), not your partner’s errant ways.

Yet you may well find that, while you don’t see the value in what your spouse is buying, there’s no actual financial harm to your family in the purchases. As Bethany Palmer points out, judgments about spending go deeper than whether a couple can afford the purchases: “It’s really about having control and ownership of the money we make.”

- Agree on a wish list. You and your spouse should separately jot down five to 10 things you want to spend money on, suggests Deborah Price, author of The Heart of Money, and then compare notes. “Where the items overlap is where you allocate your resources, putting most of the money in shared values,” she says. “Then negotiate the differences so that both people’s different needs are still met with any leftover discretionary income.”

Finding No. 6: We don’t agree on roles and goals.

Most couples think they’re on the same page when it comes to money, or so eight in 10 spouses in the Money survey said. Yet when it comes down to the particulars, not so much.

Asked to name their spouse’s greatest financial worry, for example, both sexes think their partner is more concerned with keeping up a certain lifestyle than most husbands and wives actually say they are. Women believe their husbands are more worried about losing their jobs than men say they are. And both sides underestimated how important the opposite sex rates goals such as emergency savings and paying off debt. Men were especially off base about women—only 42%, for instance, said their wives cared about having the right investments, vs. 64% of women who rated that as a top goal.

Spouses also don’t agree on who pays the bills, does the budgeting, or takes care of long-term planning. And each partner gives himself or herself more credit for everything from financial know-how to who worries more about money.

The disconnect can seem amusing, like a familiar plot from a TV sitcom—until you realize that being out of sync with your spouse can really get in the way of attaining your goals. As Klontz puts it: “If you’re not on the same starting line, there’s no way you can cross the finish line together.”

For greater harmony:

- Get help, as needed. Frustrated by conflicting goals and styles? Sometimes a neutral third party can help—say, meeting with a financial adviser or attending a money seminar. After years of being at odds over money, Karl and Lucinda Harms, both 54, of West Liberty, Iowa, decided to jointly attend a financial-management workshop last year. “My wife is a budget person, I am not, and we weren’t on the same page about what to do with our money,” says Karl, a design draftsman. The course made them realize that getting out of debt was the top priority for them, and they devised a plan to achieve it, primarily by cutting back spending. “It was an eye-opening experience,” Karl says. “I wish we’d done it 30 years ago.”

Finding No. 7: Spouses aren’t coming clean with each other.

Money’s survey found that nearly a quarter of married people don’t tell their spouse about things they’ve bought. About the same number fib about cost—and expect that their spouse does the same. And about 6% of spouses even have a separate financial account that they don’t want their partner to know about.

Why so secretive? “The No. 1 reason we do this is because we want to avoid a fight,” says Klontz. “If your partner is really anxious about money, even a totally appropriate purchase can become a point of contention.” And in fact, the top reason spouses gave for their subterfuge, cited by 35%, was to avoid a lecture from their mate.

For greater harmony:

- Allow for some money autonomy. You don’t have to justify your desire for the latest-model iPad or to opt for Laura Mercier over Maybelline. With your spouse, agree on a monthly amount that you’ll each put into separate accounts, to be used at your discretion. “Research has found that the happiest couples have a joint account for the essentials and then some discretionary money,” says Schwartz.

The system is working for Adam Hall, 31, a middle school band director, and his wife, Kristen, 25, an art teacher, who set aside $50 a month for each to spend, no questions asked. “We trust each other with our accounts, but it’s nice to have a little money of our own,” he says. “We both just wanted a little bit of financial freedom.”