When it Makes Financial Sense to File an Auto Insurance Claim—and When It Doesn't

Getting into a car accident is bad enough—you’re shaken, your vehicle is damaged, and worst of all, you or someone else may be hurt. Adding insult to injury, auto insurers these days are hiking policyholders’ rates sky-high after just one accident, even when a driver has an otherwise impeccable record.

A single claim boosts the premium by an average of 41% nationwide, according to a recent study by InsuranceQuotes.com. And in some states, the jump can be as much as 76%. (Massachusetts, California, and New Jersey are the worst.)

Considering that the average premium is $815, a fender-bender could cost you an additional $334 to $619 per year.

Even simply calling your insurer to discuss your options can have consequences. “As soon as you start talking about something that just happened, it goes on your record—it’s called an inquiry,” says Amy Danise with Insure.com. “If you build up inquiries, even if you never get a dime from a claim, you can still be viewed as high-risk, and that can affect your rates.”

All this means that you’ve got yet another thing to think about after a crash: whether you should file a claim or pay repair costs out of pocket. This road map can help you make at least that part of the situation easier.

When You’ve Had an Accident and Someone Else is Involved

You’re better off claiming, says Laura Adams, senior analyst for InsuranceQuotes.com.

If you’re at fault, and you hit another person or vehicle, he has the right to make a liability claim against you, and he could potentially sue. With insurance, you’re entitled to a legal defense and coverage of a judgment against you up to a certain amount. “The average liability claim is $15,000,” says Adams. “In those cases, it’s hard to conceive of a situation where you wouldn’t want to make that claim.”

Even if the damage seems minor, and you and the other driver agree that you’ll handle everything yourselves, that approach can backfire. “I’ve heard of cases where the other person called later and said, ‘Send me $3,000,’” says Insure.com’s Danise.

And if you wait too long to loop your insurer in—say, after you’re notified that the other driver has filed suit against you—the insurer could deny your claim entirely.

“You’re better off saying, ‘Here’s my insurer, here’s my policy number,’ and handing it off so the insurer can deal with that person,” says Danise.

When You’ve Had an Accident and No One Else Is Involved

Let’s say you back into your garage door or hit a guardrail when you skid in the snow. You’re at fault, but the only car affected is yours.

As long as you’re fairly sure there won’t be any lingering medical issues, you’re better off paying out of pocket if you can afford it.

Of course, the more money it costs to fix, the less you can probably afford it—and the more it will raise your rates.

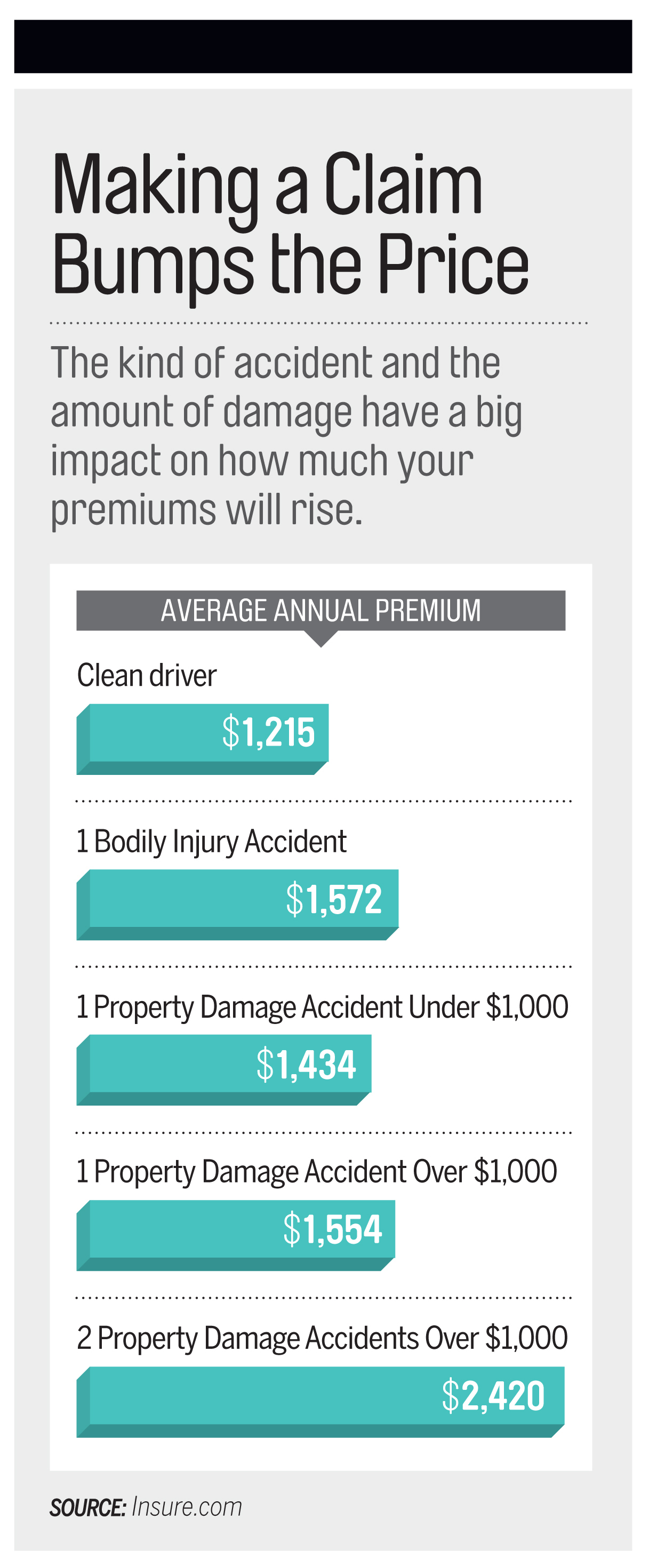

For property damage claims of under $1,000, rates will go up 18% on average, according to numbers from Insure.com. For claims over $1,000, it’s more like 29%.

Not sure? Check out the “When to Make an Insurance Claim” calculator at InsuranceQuotes.com to see how it looks in your state.

When Your Car was Damaged, but Not in an Accident

If a tree limb falls on your hood or your car gets burglarized, that’s not your fault—and insurance companies generally won’t punish you for it.

Even if you file a comprehensive claim of $2,000 or more, you’re looking at an average rate hike of just 2%, or about $18, according to InsuranceQuotes.com. So if the damage goes above your deductible by more than a few hundred dollars, there’s no harm in claiming it.

...And If You File a Claim For Any Reason and See Your Rates Rise as a Result

Ask your insurer for the surcharge schedule—which should tell you how long it will be before your premiums return to normal levels.

Also, remember that not all insurers give accidents the same weight, so you can always shop around for a cheaper policy.

More from Money.com:

25 Ways to Get Smarter About Money Right Now

How I Plan for the Stock Market Freak-out…I Mean Sell-off

What Women Can Do to Increase their Retirement Confidence