3 Ways to Lower Your Taxes in Retirement

- What the Democrats Winning Georgia Means for Your Wallet

- The Deadline for Retirees to Return Unwanted RMDs Is Almost Here

- How a 27-Year-Old Math Whiz (and His Uber Driver) Found a Big Flaw in an IRS Tax Formula

- Senate Tax Bill Expands the Break for High Medical Costs

- An Important Tax Deduction for Seniors and Their Families Is on the Chopping Block

The first few years of retirement are a perfect time to explore your passions, travel the world, and bond with your family. Something else they can be great for: cutting your lifetime tax bill—and leaving you more money to spend on yourself.

The reason? Once you stop collecting a paycheck and start living off other funds—say, investments, part-time work, and maybe a pension—chances are good that, as for most retirees, your income will drop, putting you in a lower bracket. That means you'll pay a lower federal tax rate on your highest income. But this might not last.

If you're diligently waiting to tap your tax-deferred accounts so they can continue to grow and delaying Social Security to build up your monthly benefit—both smart moves—you could pop back up to your higher tax bracket once you hit your seventies and start taking required minimum distributions (RMDs).

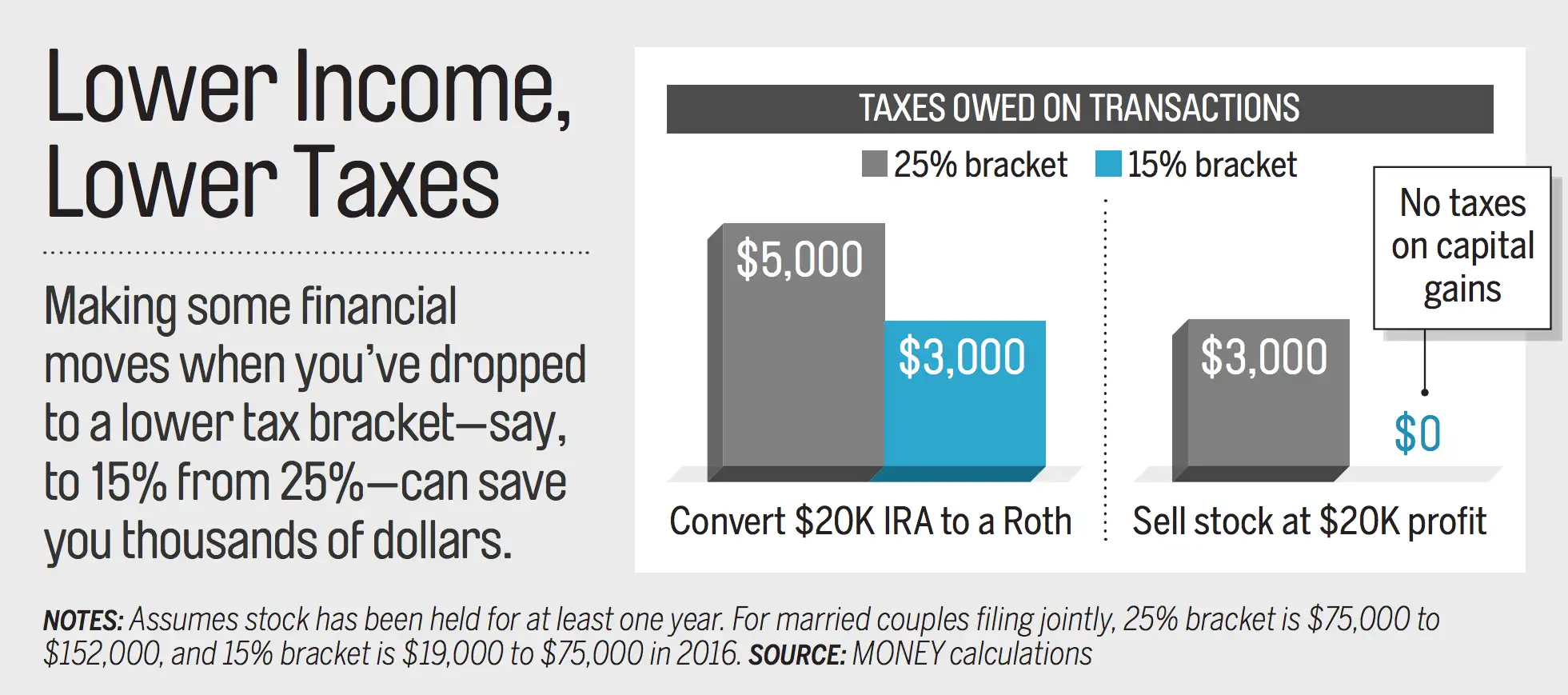

And odds are you will, say planners, if you have savings of at least $500,000 and you were in the 25% bracket pre-retirement (in 2016 that means taxable income between about $75,000 and $152,000 for married couples filing jointly; $38,000 to $91,000 for singles). Nearly all of these households could benefit from strategic moves when they're temporarily in the 15% bracket, says John Leis, vice president of personal financial solutions at American Century Investments.

Here's how you can take advantage of your briefly low bracket.

Switch to a Roth

Converting a 401(k) or traditional IRA into a Roth can significantly reduce your future taxable income, since no federal taxes are due on Roth withdrawals, unlike the case with those tax-deferred accounts.

Upon converting, you'll owe ordinary income taxes on the amount converted (excluding after-tax contributions). But once you're in a lower tax bracket, your tax bill may be smaller than it would have been a few years earlier or later.

Planners suggest stretching out a Roth conversion over a number of years, each year converting only an amount that won't push you into a higher tax bracket. "You're nibbling at the IRA," says Laura Scharr-Bykowsky, a financial planner in Columbia, S.C.

A Roth conversion is less attractive, however, if you are under 65 and are buying subsidized health insurance on the public exchanges, she warns. Because converting will increase your income, it will also decrease your subsidy.

Read More: 6 Ways to Avoid Taxes Like a Millionaire

Get ahead of the IRS

Is the bulk of your savings in tax-deferred accounts? A Roth conversion might not make financial sense, says Michael Goodman, a certified public accountant and financial planner in New York City, since you will need funds outside your 401(k) or traditional IRA to pay taxes on the conversion.

So instead you might start taking distributions from a 401(k) or an IRA while you're in your sixties. Retirement savers try to hold off on withdrawals until they turn 70½ and the IRS imposes RMDs; in the latest figures from the Employee Benefit Research Institute, 21.7% of traditional IRAs held by people in their late sixties had withdrawals, but that figure jumped to 60.7% for accounts of people in their early seventies. You might save money, however, by starting to make withdrawals earlier and in a lower bracket (as long as you're over age 59½, avoiding the 10% penalty you're subject to in most cases).

Calculator: Compare a Roth 401(k) to a Traditional 401(K)

This strategy can help you delay claiming Social Security, ensuring a higher payout when you do file and giving you income to live off before then. It also lowers your future tax liability on your retirement account by reducing the balance.

Sell some stock

If you're in the 15% federal tax bracket or lower, you don't owe capital gains taxes on the sale of securities you have held for more than one year. Investors in higher brackets will owe at least 15%. So if you drop to a low bracket, you could sell stocks that no longer fit in your portfolio, especially if they have appreciated in value, says Scharr-Bykowsky.

Your circumstances can change from year to year, based on such factors as changing tax rules and fluctuations in your income. So revisit these strategies regularly. "This is not "Set it and forget it," " says Michael Berry, head of the advanced planning team at Voya Financial.