The Comprehensive Guide to an Early Retirement

- A Growing Cult of Millennials Is Obsessed With Early Retirement. This 72-Year-Old Is Their Unlikely Inspiration

- This Millennial Couple Is Saving $150,000 a Year and Plans to Retire by 2029. Here’s How They Do It

- This 39-Year-Old Saves 75% of Every Paycheck and Is Almost Ready to Retire. Here’s How She Does It

- Can I Tap My Retirement Savings Penalty-Free at Age 55?

- What Is Medicare and How Does it Work?

Maybe you've always dreamed about retiring when you hit 60—or even before you get your AARP card at 50. Or perhaps you have watched the stock market climb for the past eight years in a row, with the S&P 500 index more than tripling since its 2009 low, and suddenly an early exit from the workplace seems as if it might realistically be within reach.

Grab this opportunity to think about what "early" and "retirement" mean to you—and set yourself on a path to bring that vision to life. Some successful early retirees who now blog about their experience prefer the term "financial independence" to "retirement": The essence is that you, and not an employer, get to call the shots on how you spend your days. That might be a pleasant schedule of travel and community service or maybe working as hard as—or harder than—before on a new business venture you've always hoped to pursue

On average, men stop paid work at age 64 and women at 62, government statistics show. Nearly half of retirees end up leaving the workforce earlier than they had planned, according to a recent report by the Employee Benefit Research Institute. That is often due to a layoff or an illness. But, encouragingly, a third speed up their exit because they can afford to.

Having a clear focus and a plan to retire early can be empowering. "It feels good to have a purpose and a strategy," says Maggie Mistal, a career and executive coach in New York City. As you see your savings grow, "even the process of getting to your dream is fun and exciting," she says.

That's not to say that making an early exit is easy, though. The more ambitious your vision, the more important it is to start saving and planning as soon as possible and the more compromises between your current lifestyle and future goals you'll likely need to make. Here are 12 key moves to make—from early in your career to your departure from the office—to turn your early-retirement dream into reality.

LAY THE GROUNDWORK

To buy yourself the freedom to retire early, adopt the right mind-set and financial plan as early as possible in your career.

1. Amp Up Your Savings Strategy

The first and probably most critical step if you really want to retire early is to assume a whole new attitude toward your finances. Every decision to spend money has to be a conscious tradeoff weighed against your goal. A little belt-tightening won't do it. It's saying no to big-ticket expenditures that makes the difference, not swearing off your daily latte. "Making your coffee at home is not going to get you to early retirement," says Arielle O'Shea, investing and retirement specialist at NerdWallet.

The goal, in short, is to live far below your means so that you can shovel away an outsize portion of your income. How much? Aim for at least 30%, financial planners say, vs. the conventional target of 10% to 15% for a typical 40-year career. To do that, make savings a nonnegotiable item in your budget, says O'Shea, and funnel all tax refunds and bonuses into your nest egg as well.

Get creative about other money hacks that can help. Jennifer Owens, 39, of the Sacramento area, hopes to retire by age 45. The corporate strategy worker gets pretax money deducted from her paycheck for childcare expenses, and when she gets reimbursed, that money goes straight into savings. "You spend what your budget allows," Owens says. While she and her husband recently bought a new Honda Accord, it was only because his 1997 BMW, purchased used, had finally given out.

2. Avoid Lifestyle Creep

There's a natural tendency to increase your spending as your earnings increase, which financial advisors call "lifestyle creep." Certainly you should treat yourself when you get a big raise or promotion. But also direct at least half of those additional dollars to savings, by having more money deducted from your paycheck or transferred from your bank account.

The aim is to spend your dollars carefully but not feel deprived. Lesia and Al Riddick, both 42, of Fairfield Township, Ohio, say they have managed to live well and still save $1 million. The couple, who have no children, enjoy traveling but meticulously research the best deals and even pack food from home to whittle their travel meal bill. "There are things we value and things we don't value," says Lesia, who hopes to retire by age 50 from her job in information technology. Al, an entrepreneur and author, plans to keep working but scale back to spend more time with his wife.

3. Cut Your Housing Costs

If you're like most Americans, your biggest expense—and thus your biggest opportunity to save—is your home. Housing costs devour a third of the average budget, according to the U.S. Bureau of Labor Statistics. Thinking of buying new digs? Stay put if your home is big enough, or at least say no to buying the biggest house you can afford.

Consider a hypothetical family in the Minneapolis area, where prices are in line with the U.S. average. They would save more than $50,000 over 10 years by staying in a starter home vs. upgrading to one 30% bigger, according to Keith Gumbinger, a vice president at mortgage-information website HSH. That estimate includes mortgage, property tax, insurance, and utility and maintenance costs.

HSH and other firms offer online calculators to help you determine the maximum mortgage you can swing based on your income and other financial details. But "you don't have to borrow the max," Gumbinger says. If you are looking to power-save, keep your housing spending to 30% or less of income, he says.

Wanda Crossman, 52, of Wyandotte, Mich., and her husband have found another way to limit housing costs. They own a two-family home and their tenant pays $950 a month. That covers most of the Crossmans' $1,060 mortgage; the remainder is less than what many Americans pay for cell phone service.

4. Take Advantage of Tax Savings

This much is certain: If you really want to quit early, you have to commit to putting away the maximum allowed in tax-favored accounts where Uncle Sam helps your money grow faster. This year, Owens and her husband plan to max out their 401(k)s to the limit of $18,000 per person and their Roth IRAs to $5,500 each. Married couples who file a joint tax return can fully fund Roth IRAs if their income is less than $186,000, regardless of whether they have a savings plan at work; the contribution is limited above that income and ends at $196,000. If you're 50 or over, you can add an extra $6,000 to a 401(k) and $1,000 to an IRA.

If you have a side hustle as well as your regular job, use a retirement plan such as a SEP-IRA to save a portion of that income. In 2017, you can fund a SEP with 20% of adjusted profit, up to $54,000.

Another smart move, if you have a qualifying high-deductible health plan, is to pump as much as you can into a health savings account. An HSA can deliver a richer payoff than your 401(k) under certain circumstances, says Greg Geisler, a professor of accounting at the University of Missouri at St. Louis. Earnings contributed to HSAs aren't taxed and can also be withdrawn tax-free—as long as the money is used to pay for qualifying medical expenses now or later in life. If the HSA is for one person under age 55, the worker and firm can put in a combined $3,400 this year.

BEFORE YOU LEAP

Getting close to your hoped-for departure? Here are the key elements of your plan that need to be locked down.

5. Put a Price Tag on Your Dreams

When you are within five years of your desired early exit, think hard about the lifestyle you want and tote up how much it will cost. That includes putting some specific figures on where you will live and the activities you will engage in. Many people mistakenly think their expenses will go down when they stop working, says Ron Weiner, managing director of RDM Financial Group at HighTower. In reality, many new retirees spend about 20% more than before, he says.

After all, you will have the time and energy to pursue hobbies and take trips, which costs more than sitting at a desk all day. The younger you are when you leave the workplace, the more years in which you are likely to have the energy and good health for an active (and potentially costly) retirement lifestyle.

Know that some items in your budget may increase at a higher rate than overall inflation. Health care expenses, for example, could rise by as much as 7% to 10% annually, says Andrew Murdoch, president of Somerset Wealth Strategies in Portland, Ore.

Tools like T. Rowe Price's Retirement Income Calculator can help you see if your portfolio is on track to support your projected spending. If not, you'll have some choices to make: boost your savings, scale back your lifestyle expectations, or push your retirement out a few years.

6. Line Up Medical Coverage

Having access to medical insurance when you leave the workforce can be a make-or-break factor for would-be early retirees. You'll need a bridge until the Medicare eligibility age of 65. The gold standard: coverage through a spouse's job or a former employer of you or your spouse.

Darrow Kirkpatrick, 56, author and publisher of CanIRetireYet.com, was able to retire at age 50 thanks in part to the health coverage his wife had as a teacher. When she retired a few years after him, that insurance morphed into retiree medical coverage for the couple. (In private industry, just 16% of people worked at companies that offered retiree coverage in 2015, says the Employee Benefit Research Institute.)

If you won't have coverage through a job, you'll have to purchase individual insurance. Start researching current offerings through a broker such as eHealth.com. Nationwide, the average premium for a 2017 silver plan on the Obamacare exchanges is $574 a month for a 50-year-old nonsmoker who doesn't qualify for government subsidies, according to HealthPocket; at age 60, that average is $872. Silver plans come with high out-of-pocket costs, including an average deductible of $3,572 for individuals, according to HealthPocket.

Keep in mind that the options and costs you'll face are up in the air as President Donald Trump and congressional Republicans move to dismantle Obamacare. Some proposals would boost the costs of people approaching retirement by allowing insurers to charge older buyers up to five times what the youngest ones pay, vs. three times now.

7. Play It Safer With Your Portfolio

If you plan to retire at age 50, say, you should be more conservative with your portfolio in your late 40s than your peers who plan to stay in the workforce until 65 or later. This is to avoid what advisors call "sequence of return risk," or having a series of down markets clobber you when your finances are particularly vulnerable.

Consider an example from fund company MFS of two hypothetical 61-year-old retirees who begin taking $12,500 a year from their $250,000 portfolios, with their withdrawals indexed 3% for inflation. Over a 30-year period, returns average 6.6% a year for both. Investor A, who starts off with three years of losses in a row, runs out of money at age 80. Investor B, who experiences early positive returns, sees his portfolio grow to $632,606 by age 91.

As a very general rule of thumb, you should have 40% to 50% of your portfolio in stocks at retirement, says Wade Pfau, professor of retirement income at the American College of Financial Services in Bryn Mawr, Pa. By contrast, for a 50-year-old who plans to work to 65, he suggests 50% to 60%.

Similarly, David Blanchett, head of retirement research at Morningstar, says a 55-year-old early retiree might keep 45% of his money in stocks, compared with 55% for someone the same age who plans to work until 65.

One way to gradually lower your portfolio's stock risk is to use the new dollars you invest mostly to buy bonds, Pfau says. That could include building a "ladder" of Treasury securities by buying one 10-year note each year at TreasuryDirect.gov in the decade leading up to retirement.

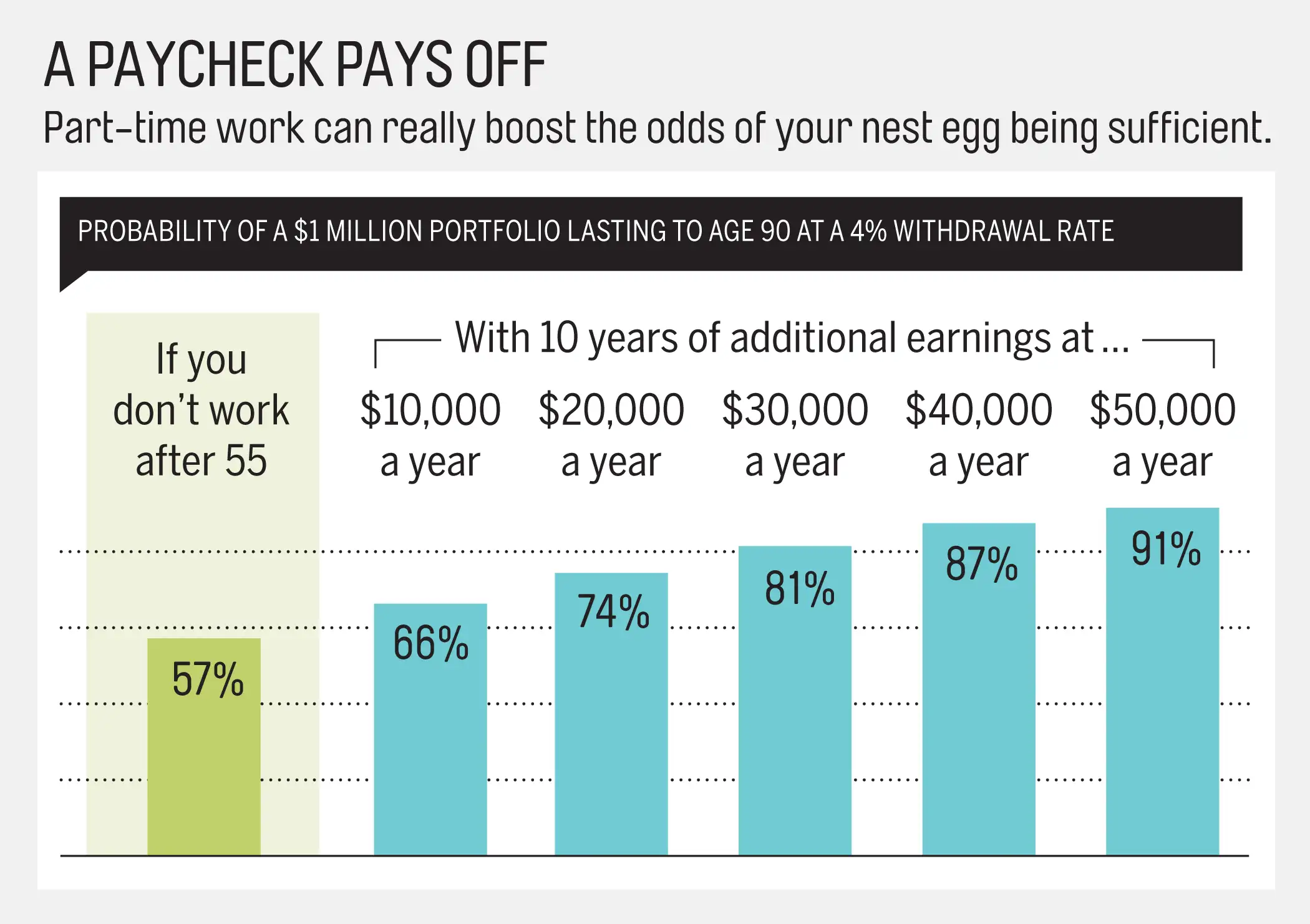

8. Plan for a Paycheck

You may have a clear vision for a deeply satisfying retirement life of social activities, travel, and volunteering. But in most cases, unless you are truly wealthy, you should also have a concrete plan for some type of paid work. While part-time labor gives retirees of all ages a financial cushion, earned income is essential for those who retire young, experts say.

As shown in the graphic below, a 55-year-old retiree who is paid just $10,000 a year for 10 years will increase the chances of his portfolio lasting until age 90 by nearly 10 percentage points, according to a calculation by Blanchett of Morningstar. This math assumes the man has a $1 million nest egg and withdraws 4% of that the first year; after that, he boosts the dollar amount each year by the rate of inflation.

Part-time income can also help you delay claiming Social Security until age 70, a move that will boost your payout by up to 8% a year. Another consideration: Your Social Security payout is based on your top 35 years of earnings, so you want to have at least that many years of work income.

9. Get a Head Start on Gig Work

If you don't explore your options for retirement jobs now, "you are wholly unprepared to pivot" from full-time to part-time work in retirement, says Mark Gasche, vice president of career strategy at SoFi, an online finance company. This holds particularly true for those who have worked for decades in the same role or company, he notes.

Plan to consult in your field? Start doing small jobs for friends or nonprofits, says career coach Mistal. You might not charge them, but ask for a testimonial when you're done, she says. Websites such as VolunteerMatch .org can help you find nonprofits in need of volunteer help with grant writing and other professional tasks. If you'd like to explore paid options, firms such as Patina Solutions match experienced executives with companies looking for project-based help.

For another type of income, a friend of Kenn Tacchino, professor of financial planning at Widener University in Chester, Pa., started renting out a room in his home to out-of-town executives visiting a nearby company. One person ended up staying for two years on an extended assignment.

SUSTAIN YOUR EARLY YEARS

You did it! But keep an eye on your compass and be ready to course-correct as you navigate your way in the initial stage of retirement.

10. Stay Financially Flexible

Financial planners typically run annual checkups on their clients' finances. If you don't work with an advisor, do your own yearly review of your spending, which you can track with an app such as Mint. Revisit the financial-planning tool you used previously to update how long your portfolio might last given your actual spending and reasonable assumptions of investment returns.

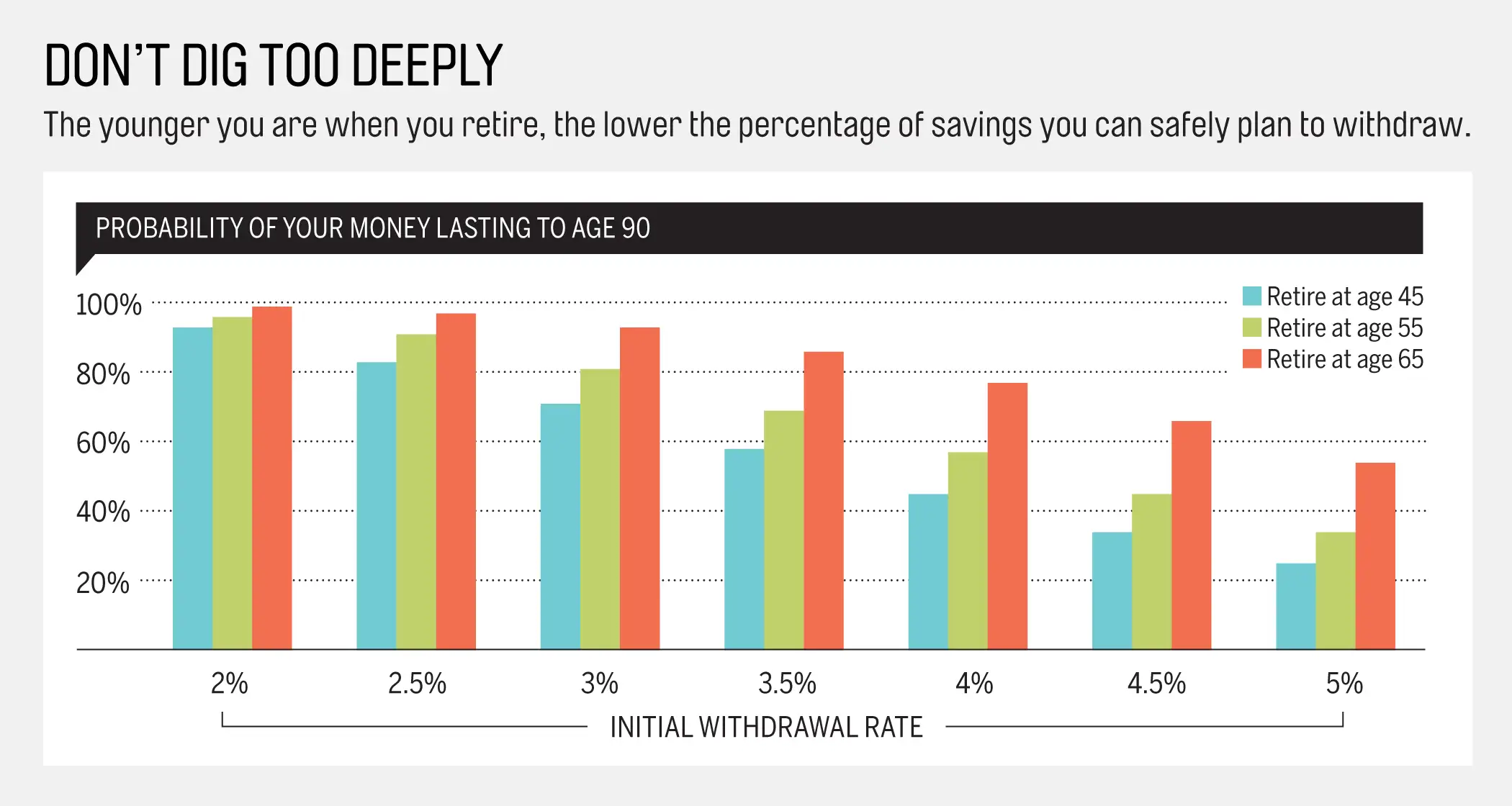

You may go into retirement with a plan to withdraw a certain percentage of your nest egg in year one, and then adjust the dollar amount for inflation each year. For eight-in-10 odds of your money lasting to age 90, Blanchett of Morningstar says to use a 3.8% withdrawal rate if you retire at 65, 3% at 55, and 2.6% at 45. (Those percentages correlate with the required nest eggs in "What It Takes" graphic near the top of the story.)

If a spending shock leads you to withdraw a lot more one year—maybe it's for a granddaughter's destination wedding—cut back the next year, Blanchett says. Similarly, he says that if you skip the inflation bump to your withdrawals in any year the market goes down, you will boost your chances of your portfolio lasting until age 90 by nearly 11 percentage points. That calculation assumes an initial withdrawal rate of 4%.

11. Tweak Your Portfolio

As you move further into retirement, you might boost your stock exposure once again—say, to 60%—to benefit from the higher returns stocks have provided over time. For protection, you could couple that with buying a so-called longevity annuity that guarantees a set income stream later on. A 55-year-old man who invests $50,000 today can get $3,115 monthly for life starting at age 85, according to Murdoch of Somerset Wealth Strategies.

12. Be Flexible on the Nonfinancial Part Too

Early retirement can be amazing, but it can also take a little time to adjust to.

One challenge: "If you're 50 and retired, there aren't a lot of people like you," says Ken Moraif, senior advisor at Money Matters in Plano, Texas. You might meet working friends during their lunch hour. Look to make new pals, younger and older, through groups you get involved with.

Murdoch finds that his early-retiree clients benefit from a "goal-focused approach." One man, who retired as a chiropractor at 52, joined the Travelers' Century Club, for people who have visited 100 or more countries. He takes pleasure in crossing countries off his list as he travels.

Early retirement involves some experimentation on how you want to live, Mistal says: "You're giving your dreams a chance."