How to Check Your Credit Report

- Inflation-Free Thanksgiving? These Stores Are Slashing Prices Ahead of the Holiday

- How Baby Boomers Became the ‘Wealthiest Generation That Ever Lived’

- Tipping Your Auto Mechanic? Here’s Where People Draw the Line on Adding Gratuity

- Rich People Really Are Happier Than the Rest of Us: Study

- The Hidden Cost of Using Everyday Bills Like Netflix and Rent to Boost Your Credit Score

- 1 Million Public Service Workers Have Now Had Their Student Loans Forgiven

- As Student Loan 'On-Ramp' Ends, Missed Payments Will Once Again Hurt Your Credit

- How Low Will Interest Rates Go? Experts Predict the Fed's Upcoming Cut

- How to Pay Off Student Loans Fast

- Here's the No. 1 Barrier Blocking Parents From Saving More Money for College

- 2025 Tax Brackets: IRS Bumps Up Income Cutoffs and Standard Deduction

- Former College Athletes Can Now Submit Claims for Payouts in $2.8 Billion NCAA Settlement

- Will Inflation Be Worse Under Trump or Harris? Here's What Economists Say

- Trump Wants to Give Americans With Car Loans a New Tax Break. Here's How It'd Work

- Facebook Settlement Payments Won't Go Out Until Early 2025 (or Later)

It’s best practice to frequently check your credit reports, which serve as a kind of financial resume outlining all of your money matters. Credit reports can help you keep track of your debts and check for signs of identity theft.

Thanks to the Fair Credit Reporting Act (FCRA), you can always request one free credit report a year from each of the three big credit bureaus — Experian, Equifax and TransUnion — online at AnnualCreditReport.com. The three credit bureaus typically charge for each additional report beyond the free annual one, but because of the pandemic and the economic uncertainty that ensued, you’re now allowed to pull a credit report for free each week until at least Dec. 31, 2023.

Here’s everything you need to know about getting your credit reports.

Table of contents:

- How to get a free credit report from AnnualCreditReport.com

- How to request your credit report from a credit bureau

- Additional ways to acquire your credit report

- Summary of Money’s guide on how to get a credit report

How to get your credit report

Getting your credit report is fairly easy, and it should be free in almost all cases — especially until Dec. 31. That makes this an easy personal finance task to check off your list. Here’s how to do it.

How to get a free credit report from AnnualCreditReport.com

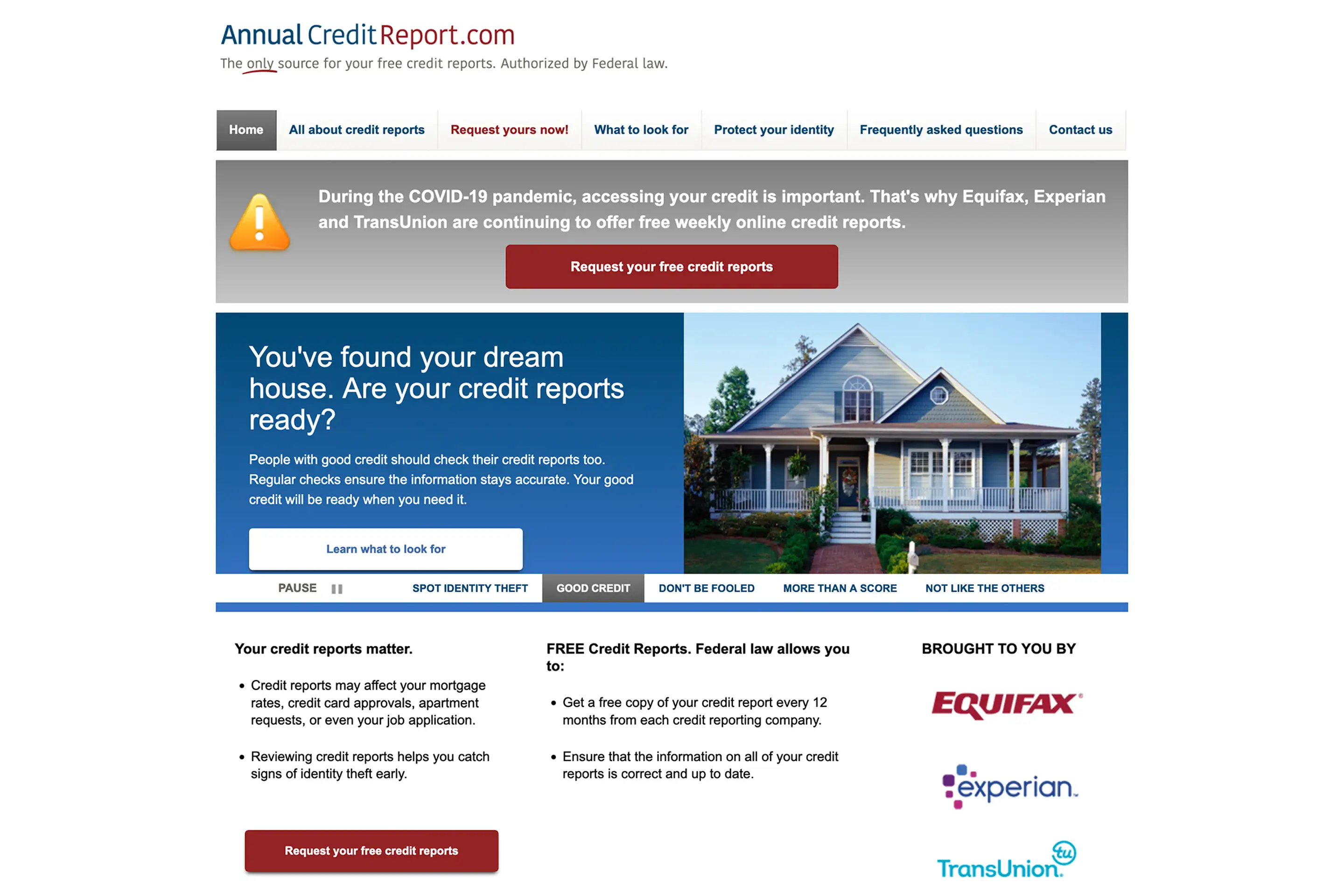

AnnualCreditReport.com is the only website authorized by the federal government to provide you with your free annual credit reports from Equifax, Experian and TransUnion. This website is also where you can access a free copy of your credit report each week until the end of this year.

Once you’re ready, head to AnnualCreditReport.com on a private, secure internet connection. Do not enter sensitive information while connected to public Wi-Fi, even if you trust the website. And do be sure that you’re on the correct webpage, as there are many look-alike sites that will try to harvest your personal information.

From the home page, click on “Request your free credit reports.” You’ll need to complete three main steps to access them, which shouldn’t take you more than five or 10 minutes if you have all of your personal information memorized or have the necessary documents nearby.

The first step is to fill out an online request form. You will need to provide the following information:

- Your full name

- Your Social Security number

- Your date of birth

- Your phone number

- Your current address

- And your previous address if you’ve lived at your current residence for two years or fewer

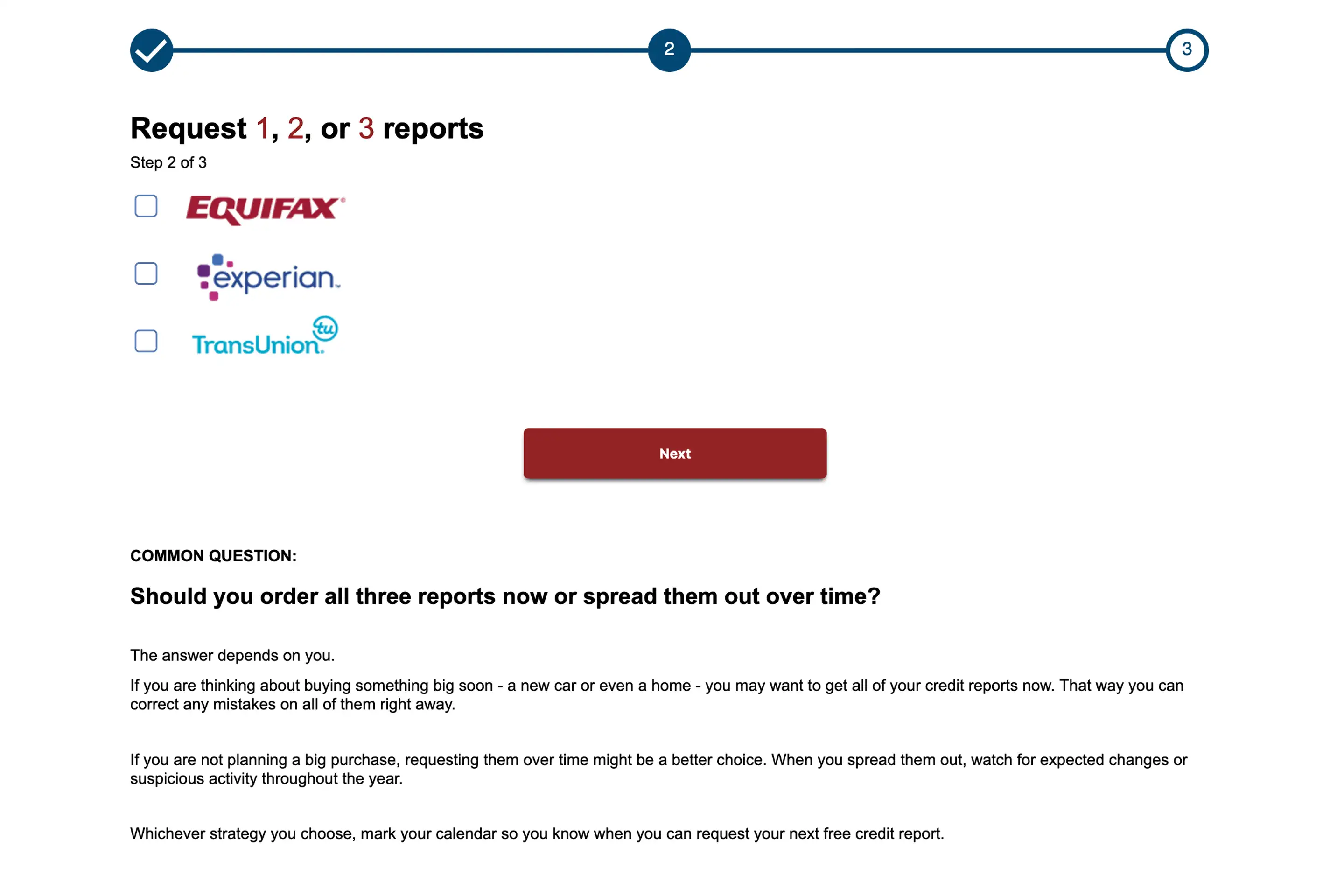

The second step is to select which of the three credit bureaus you would like a credit report from. You can select one or all three, if you’d like.

Since the reports are temporarily free each week, requesting all three at once shouldn’t be an issue. However, once the credit bureaus stop offering this weekly service for free, the Consumer Financial Protection Bureau (CFPB) says it may be a good idea to spread out each request, that way you can better monitor your credit throughout the year.

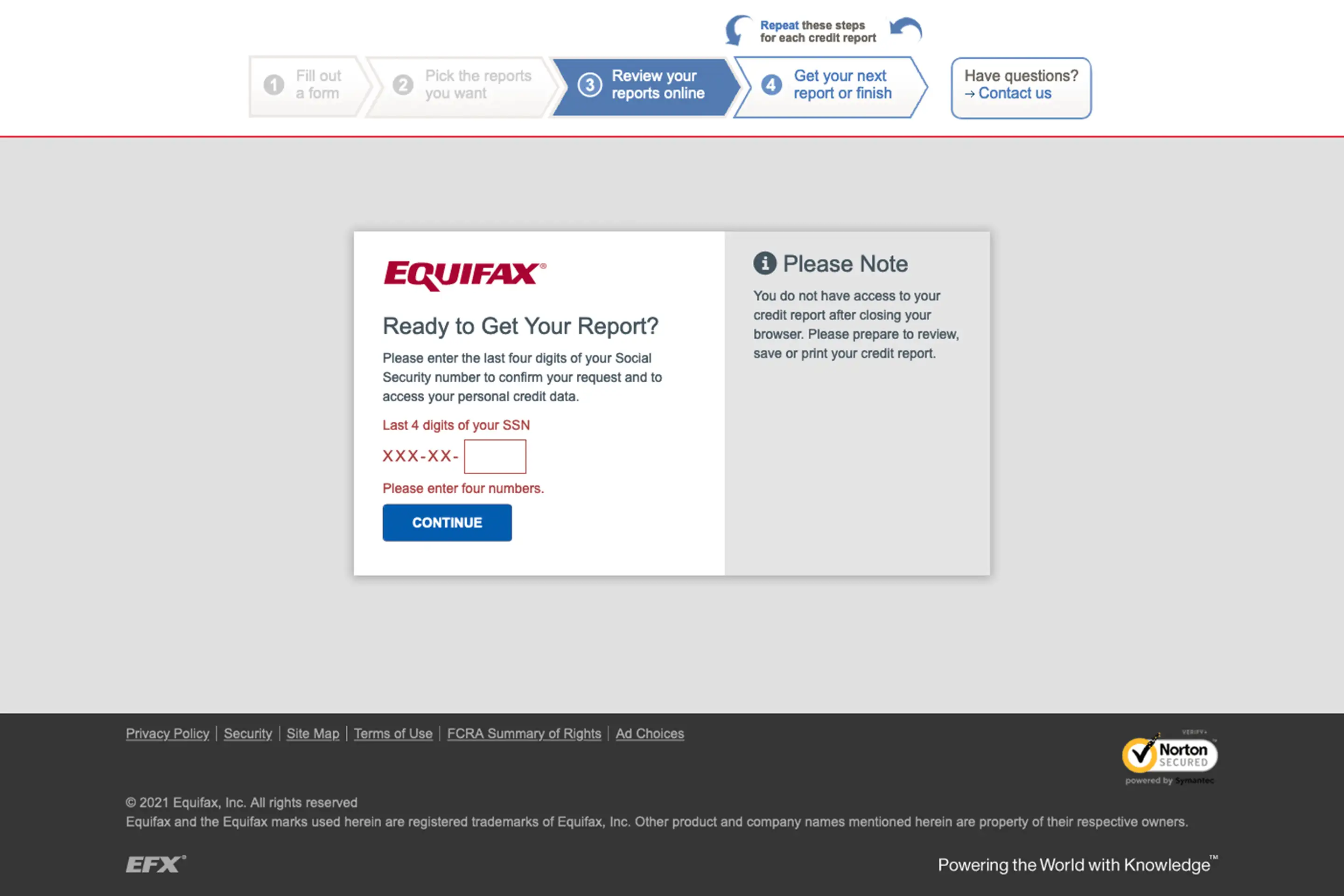

Lastly, you'll need to answer a few questions to verify your identity for each of the credit bureaus you selected.

For example, if you selected the Equifax report, you will be forwarded to Equifax’s website. There, you will need to provide the last four digits of your Social Security number and answer security questions about your credit history, including details about your credit cards, previous lenders, contact information, current or former addresses, previous employers and more. Trick questions are included, so be prepared.

Repeat this process as necessary for each credit bureau.

After completing the verification steps, you'll be able to review and/or dispute your credit reports online. You can also print or download the reports for later use.

If you prefer not to — or you’re unable to — complete the online process outlined above, you can also request your credit reports by mail and phone. The company Central Source, LLC runs the website, and you can call them directly at 1-877-322-8228 to request your credit reports.

Alternatively, you can print out and complete a physical request form, known as the annual credit report request form, then mail it to the following address:

Annual Credit Report Request Service

P.O. Box 105281

Atlanta, GA 30348-5281

Once you've received all of your credit reports, it's important that you review your credit information for any inaccuracies. If you come across errors or any new credit accounts you don't recognize, correct the information with the bureaus immediately.

You’ll notice that your credit report does not include your credit score, neither your FICO score nor your VantageScore. That is not a mistake. Credit reports simply don’t include that information. You can access your free credit score with these methods.

Your credit report does, however, include credit account information (Ex. Types of credit and credit limits), your payment history and info on negative events like bankruptcies. Here’s more on how to read your credit report.

How to request your credit report from a credit bureau

For basic credit hygiene, getting your three free credit reports from AnnualCreditReport.com is a good start.

However, there may be circumstances where you will need to check your credit report more frequently than what’s available for free. For instance, you may be buying a home or starting a new job. Or perhaps you’re doing your due diligence to protect against identity theft. Pulling your credit report in all of these cases would be a judicious move. But in some cases, it may come with a fee.

According to the CFPB, the credit bureaus legally can not charge you more than $14.50 per report. As a reminder, the three major bureaus are allowing you to check their credit reports every week for free until Dec. 31. After that date — or in the meantime if you need to check your credit report more than once per week — you can contact the bureaus directly to buy your credit report.

Equifax

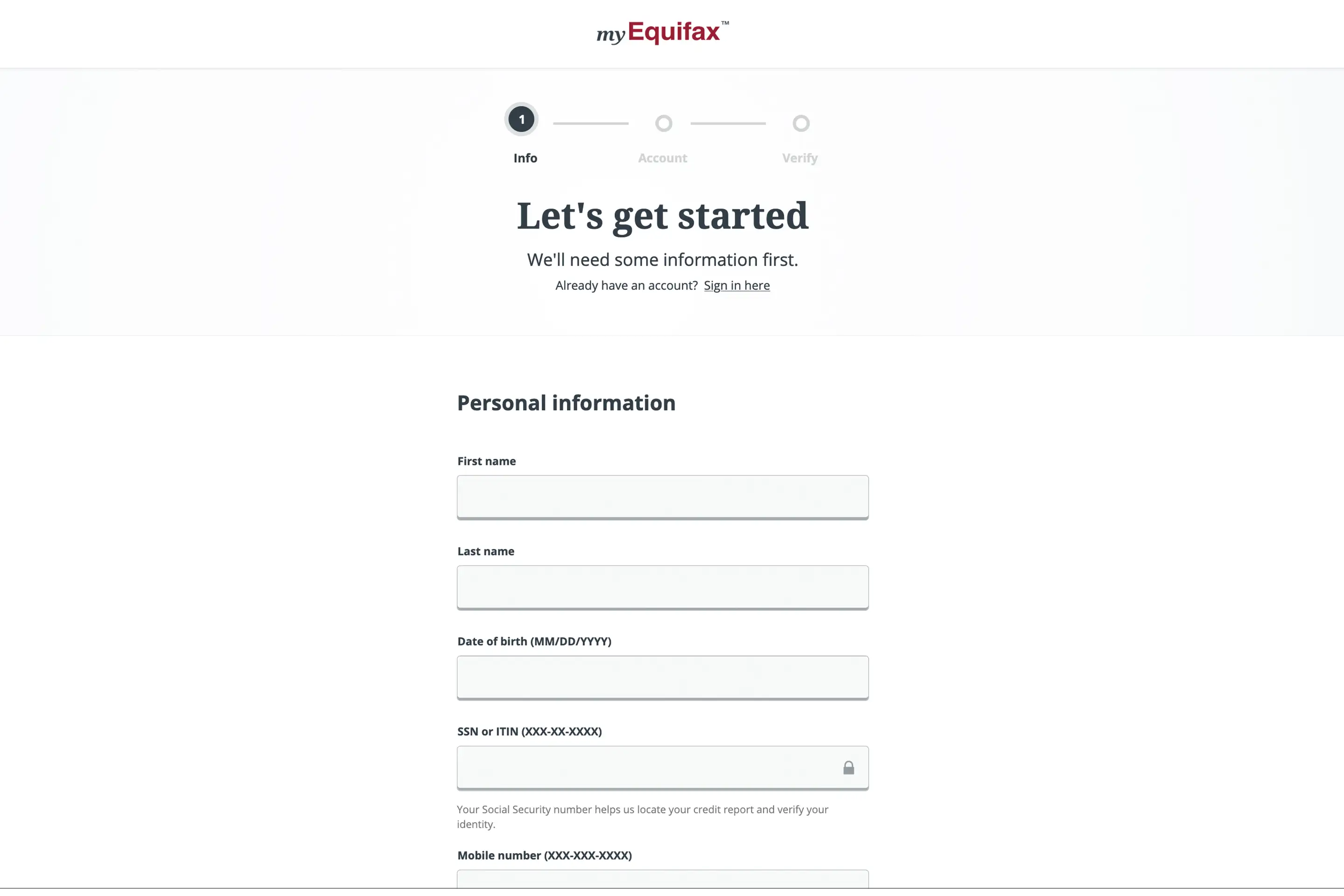

To request a credit report directly from Equifax, you can call 1-800-685-1111 toll free. You can also request one online by creating a myEquifax account. Once your profile is set up, you can request a credit report from your account page.

Experian

To get your Experian credit report straight from the company, either call 1-888-397-3742 or go to Experian’s report-access page, select “Request my Credit Report” and follow the prompts to determine if you qualify for an additional free credit report or if you are required to purchase one.

TransUnion

Finally, you can call TransUnion directly at 1-888-909-8872 if you need additional credit reports beyond the ones that are available for free. To request a TransUnion credit report online, you will need to create a TransUnion account. From your account’s dashboard, you may request a credit report once every 24 hours.

Keep in mind that even though the three credit bureaus are legitimate, they may also try to upsell you. Remember that you’re only there to request a credit report — and not to buy additional services related to credit scores, identity-theft protection or credit monitoring.

By federal law, credit-reporting companies can only charge you up to $14.50 per report. If your total is higher at checkout, double check that there are no additional financial products tacked on.

According to the Federal Trade Commission (FTC), there are several scenarios in which you could qualify for additional free credit reports beyond the free weekly (for now) reports:

- If you have a fraud alert on your credit file and/or if you believe your credit report is inaccurate because of identity theft or fraud.

- If you’re on public assistance, such as unemployment insurance or other welfare programs.

- If you’re jobless and plan to search for employment within the next 60 days.

- If you get an “adverse action notice,” which is an alert that indicates you’ve been denied credit, insurance, employment or other benefits based on information from your credit report.

- If your state’s laws provide additional free credit reports.

Also, as part of the settlement for the massive Equifax data breach in 2017, you can receive six free Equifax credit reports per year until 2026.

If any of the above scenarios apply to you, don’t pay for your credit report. If you’re unsure, try calling the toll free numbers of the credit bureaus to explain your situation.

Additional ways to acquire your credit report

The above strategies are focused on the three major credit bureaus: Equifax, Experian and TransUnion. However, while those three bureaus are nationwide and are likely to have the most comprehensive consumer data on you, they are not the only organizations to compile credit reports.

According to the CFPB, you are also eligible to receive free annual reports from more than 50 additional specialty credit-reporting agencies. These companies compile consumer data in the following areas:

- Checking and banking accounts

- Employment history

- Gaming (casinos and race tracks) history

- Low income and subprime credit

- Medical records

- Personal property insurance

- Retail returns and fraud

- Supplementary credit records (including public records)

- Tenant and rental records

- Utility payments

While it may be overkill to pull dozens of credit reports from these niche agencies on a regular basis, their reports can come in handy in certain circumstances. If a bank denies your request to open a checking account or if a landlord rejects your rental application, you can pull a report from the corresponding agencies to see if something’s on your consumer record.

View the CFPB’s detailed list of credit agencies for contact details of the individual companies and what areas they specialize in. Note that not all of the companies are nationwide, and they might not all have data on you.

What to do if there’s an error in your credit report?

If you spot an error in your credit report, your first step is to dispute the issue with the credit bureau or bureaus showing the inaccuracy. You can do this online with all three bureaus, but you have options also to initiate disputes by mail or by phone. The credit report dispute process takes a few weeks, and the bureaus will notify you of the findings.

You can also send a dispute letter to the company that appears to have reported false information to the credit bureaus. That could be a bank, your landlord or a credit card company — they’re all required to accept dispute letters, according to the CFPB.

If you need to contest collections activity on your credit report, you can follow the steps here.

FAQs about checking your credit report

What is the easiest way to check my credit report?

Is it bad to check your credit report?

How often should I check my credit report?

What's the difference between a credit report and a credit score?

Summary of Money’s guide on how to get your credit report

- AnnualCreditReport.com is the best place to start to get your free credit reports from Equifax, Experian and TransUnion all in one spot.

- Since 2020, Equifax, Experian and TransUnion have all offered free weekly credit reports — also available through AnnualCreditReport.com. This is in place until Dec. 31, 2023.

- If you have exhausted all of your free credit reports from the major bureaus, you may contact them directly to purchase additional reports. They legally can’t charge you more than $14.50 per report.

- While Equifax, Experian and TransUnion are the most popular credit bureaus, they’re not the only places to provide credit reports. According to the CFPB, you are also eligible for free annual credit reports from dozens of other credit-reporting agencies, most of which specialize in a niche credit topic.

Chris Huntley contributed to this article.

More on Credit & Credit Repair

Money’s Top Selection Guides for Improving Your Credit

Money’s Credit Repair Companies Reviews |