The Newlyweds' Guide to Financial Success

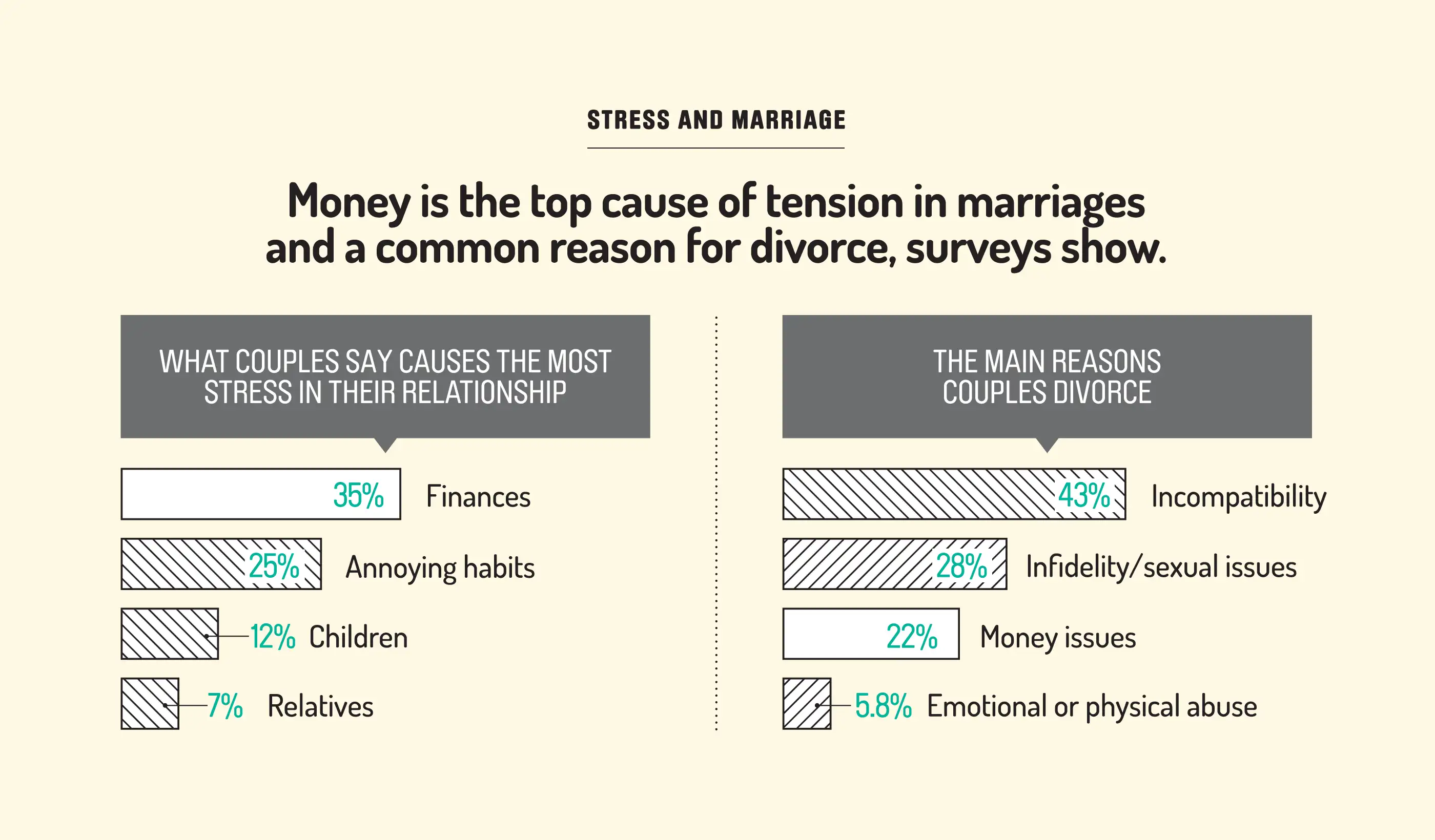

As unromantic as it sounds, finances play a big role in how successful—and how happy—your marriage will be. Money is the No. 1 cause of stress in relationships, according to a survey by SunTrust Bank, and having financial arguments is the top predictor of divorce, a separate study by Kansas State University found. On the plus side, a Money survey revealed that couples who trust their partner with finances felt more secure, argued less, and had more fulfilling sex lives.

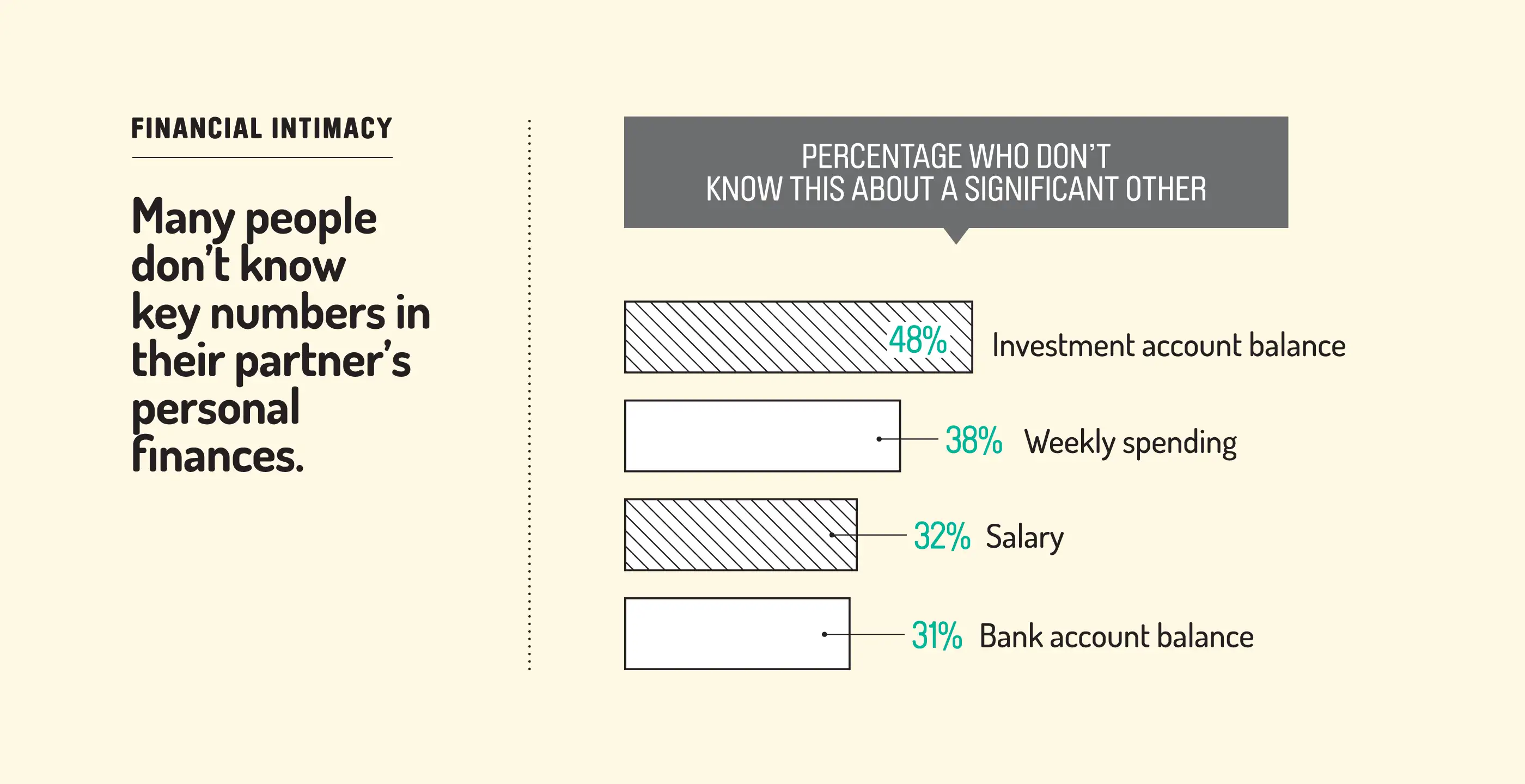

That level of trust, though, isn't common among newlyweds. By your wedding day, you know many things about your spouse-to-be. But if you're like most couples, there may still be big gaps when it comes to his or her finances. "We're intimate with our partners in so many ways before marriage, and yet money remains off the table. That's a problem," says Paula Levy, a marriage and family therapist in Westport, Conn.

Financial intimacy starts with better communication, and that's where this story comes in. We'll tell you how to get your financial partnership off on the right foot, the right questions to ask, and pitfalls to avoid—with the help of anecdotes and advice from real couples. And if this is a second marriage, or if you're approaching or in retirement, we've got extra pointers specifically for you.

For the Two of You

• Bare your assets … and debts.

It's time to have some fun in the sheets—balance sheets, that is. If you haven't done so before, make time this month to discuss all the assets and debts you are bringing into the relationship. Come clean about salaries and other income, as well as your spending over the past year.

A TD Ameritrade survey found that 38% of couples were only somewhat or not at all aware of their significant other's debts. In fact, 43% of people don't even know how much their partner makes, a Fidelity survey found. The irony: 72% of those same couples said they communicate exceptionally or very well about financial matters.

"Everyone in the marriage needs to go in with their eyes wide open. You don't want to be blindsided later," such as by unknown debt, says Damian Dunn, a financial planner based in Auburn, Ind. Part of success in finances is education. You can learn how to invest in stocks HERE.

Being honest about finances was tough at first for Chicago couple Erica and Wade Loewe, 35 and 38, respectively. "We had to overcome a great deal of fear and shame," says graduate student Erica, who worried that Wade might judge her for her debt. Wade, a service technician, felt uncomfortable because money wasn't discussed in his family. But "it wasn't as scary as we thought," he says. "Once we knew what each other owed and had, we could focus on making a plan and tackling our debts." Eight years after the wedding, they have paid off more than half the debt that Erica brought into the marriage.

• Share your family history.

Your upbringing colors how you handle and view money. If you often squabble about finances, try to figure out why your partner saves and spends the way he or she does, says Kathleen Burns Kingsbury, author of How to Give Financial Advice to Couples.

Start off easy, with questions such as "What's your first money memory?" or "How did you spend your allowance?" suggests Kingsbury. Move on to "What's the best thing you learned about money from your parents?" and "What's one thing they taught you that you want to leave behind?"

Kingsbury recalls one client who inherited his middle-class parents' frugality. His wife was raised in a household where money was far tighter; now that she was earning a good salary, she wanted to enjoy the best and provide their children with an experience very different from her own. Understanding their histories helped lessen the frequency and duration of their money disagreements, she says.

Bob Saumur of Champlin, Minn., now 72, says he learned early on in his 48-year marriage that money arguments aren't really abut dollars and cents. "It's about how the person looks at life and what his or her priorities are," he says. The first money clash with his wife, Sue, centered on what home repair they should make with a bonus Bob earned. He wanted a water softener. Sue wanted new carpeting. "We ended up flipping a coin, but I couldn't understand why she didn't agree with me," recalls Bob. "It was only later as we talked it over more that I realized her wanting carpet was really about the health of our child, who was just then starting to crawl."

• Don't be a stickler…

Some spouses pool their money in joint accounts, while others keep their dollars separate. For Ruth Bacher and her husband, Jason, both 40, setting up a joint account and keeping some money separate made more sense. "We both had a lot of financial history prior to marrying," says Ruth, a corporate purchasing consultant, who had already been married once and didn't want to burden Jason with the student loan debt she was bringing into the union.

When Sejal Madhubhai, 26, married Erik Hansen, 31, last year, she was earning a lot less than him. “That pay disparity gets to me,” she says, making her feel guilty at times for spending money. To make it more comfortable, the Orlando couple divvy up the bills so that they share four main categories of household responsibilities. Sejal pays the rent and utilities. If you find yourself renting, make sure to purchase renters insurance. Erik pays more in dollars, taking care of credit card and health insurance payments.

There's no one right approach that fits all newlyweds. What matters is that you agree on a system and—here's the important part—are open to changing later on. You have to be "flexible in the sharing of expenses," says Ruth Bacher.

That's because what seems fair at the outset may not end up being so. Therapist Paula Levy recalls one couple she helped who chose to divide all joint expenses fifty-fifty. The problem? The husband earned significantly less than the wife. "He was maxing out credit cards, struggling to afford his half of the bills, and his wife didn't even know," she says.

• … Or a killjoy.

The top source of financial conflict among couples is "overspending on frivolous purchases," Money found in a survey of millennials and boomers. Ease that tension by deciding on a monthly amount that each spouse can freely spend, no questions asked. Just agree to consult each other on the big stuff. SunTrust found that 36% of partners do not talk to each other about large purchases, while a CreditCards.com poll showed that one in five people in a relationship admits to spending $500 or more without telling the other.

Agreeing on a dollar limit above which you need to clear purchases gives the spouse who spends more some autonomy, while the more frugal partner can rest assured that the other isn't depleting the accounts. The magic number most couples say they can spend without informing their spouse: $154, according to that Money survey.

• Take an early look at taxes.

If the two of you have similar earnings, you might owe more tax as a married couple than you did before. The reverse is true if your pay is very different. Rough that out using tax software. Update your W-2 withholding forms with your employers. Set a little extra cash aside in case there's a first-year shortfall.

• Tackle debt together—as a team.

When you get married, your spouse's debt does not automatically become yours, but how much he or she owes will affect your budget and life choices, says credit expert Jeanine Skowronski of Credit.com.

For instance, a spouse's heavy credit card debt or low credit rating could make it harder for you to buy a home. So make reducing debt a priority. If there are multiple debts, start with the highest-rate obligation first, to reduce the total interest you pay. Alternatively, focus on the smallest one first for motivation-building early success.

Opening joint accounts, applying for joint credit, cosigning a loan, or adding your spouse as a joint account holder will make you both liable for any debt incurred during your marriage, and your credit report could get dinged if it is now associated with negative accounts, warns Skowronski. In community-property states, married couples are liable for any debt that either spouse takes on in marriage, even if only one spouse signed the paperwork for that account or loan.

• Team up to save.

Maintaining one household is typically less expensive than living separately, and paying less for housing is only one of many ways you can save. Cell phone providers and car insurers, as well as facilities like gyms, often offer better deals when you sign up jointly. You don't need multiple Netflix or Amazon Prime accounts either.

• Lay out your financial priorities.

To achieve your goals, you first need to agree on what they are: buying a home, starting a family, declaring yourselves debt-free? Start by each independently listing your top goals, what you think your spouse's top goals are, and what you think your top goals are together, says financial planner Jeff Motske, author of The Couple's Guide to Financial Compatibility. Share your lists to shape a joint plan.

People who identify specific goals make faster progress toward their savings and investing targets, TD Ameritrade has found. "Give yourself a deadline and dollar amount," says financial planner Dunn. "Most people are hesitant to really define goals because they're afraid they will fail, but not having a clear plan makes you more likely to fail."

• Decide on your roles.

Typically, the person with the most aptitude, interest, or time for a particular money task becomes responsible for it. When Erin and Jayson Davis, now 37 and 34, got engaged 10 years ago, Erin discovered a pile of overdue bills and notices in his apartment pertaining to Jayson's $120,000 in student loans. She was worried that he didn't have a good handle on his budget or a clear repayment strategy.

Turns out, Jayson was simply overwhelmed by his 80-hour workweeks. Erin stepped in and continues to oversee the bills today, as a stay-at-home mom to four kids. "I have a sheet on which I keep track of the monthly bills, and I make sure everything is paid on time," she says. Having one person handle a lot of the money tasks is fine as long as both of you have a strong sense of your overall financial situation. Get that by going over your numbers together every month or quarter.

What if you have different approaches to investing? A risk-averse investor and a risk-taker might divvy up their money to manage separately, suggests Rapid City, S.D., financial planner and financial therapist Rick Kahler. "Often they will balance each other's risk exposure out," he says. Still, you or a financial planner should check that all the pieces fit together with your long-term needs.

• Get your paperwork in order.

It's no fun, but you need to update or write wills to spell out your wishes for your assets if something happens to you. Without a will, state law decides. You'll probably also want to appoint your spouse to make medical decisions for you if you can't. And update your beneficiaries on retirement accounts and insurance policies.

• Know when to ask for help.

If you and your spouse find money conversations extremely tough and unproductive, you may need to bring in a financial planner, accountant, or other professional to help.

For DD and Joe Kullman, 56 and 64, hiring a financial coach two years ago was a marriage saver. "We've been married 17 years and have had completely different perspectives and philosophies about handling money for most of it," recalls DD. There were tensions between saving and spending, including about financing things for her two sons from a prior marriage.

The coach helped the Kullmans create a budget and separate accounts for different goals. "It took the emotions out of play" and allowed the pair to pay off $25,000 in debt over the past two years, says DD.

In hindsight, getting help earlier "would have made all the difference," says DD. "I know we would be further ahead on paying off our debt and with our savings."

If You've Got Exes or Children

• Don't be a prisoner of the past.

It's hard enough to blend your financial styles—and finances—when each of you has years of experience of managing your money in a certain way, says Levy. Don't make that harder by bringing in financial baggage from your prior relationship. "When we've been in a relationship that didn't work out, especially because of money issues, there is a tendency to be more guarded," says Levy. Or sometimes we overcorrect and change how we divvy up our marital finances, even if the system we used in the first marriage works fine in the second.

Bringing those biases into your new marriage—or shutting your new spouse out of certain areas of your finances—can backfire by creating trust issues that keep you from working as a team.

• Be grownups about the kids.

How much you spend on your children vs. her children vs. "our" children will always be a touchy subject. Be open from the start, not just about the legal support you pay or receive, but also about extra expenses, such as trips to see your children or contributions to college savings. And be prepared for some rough spots as you negotiate different family traditions around allowance and gifts.

Peter and Lisa Shafer, 53 and 51, respectively, have had some tough conversations over spending on Peter's two sons from a previous marriage and their two daughters together. "Lisa struggled for years with the percentages I had to pay my ex-wife for alimony, child support, health care, and now college costs," says Peter. The pair decided to have frequent money meetings, during which all of the kids' expenses would be laid out, as well as other goals. "We focus on making the spending on all four feel fair. I don't tally how much I spend on one's activities. I just try and ensure they each get what they need and can do what they want," says Peter.

• Bring in the lawyers.

A new and potentially more complicated family financial situation calls for updating estate documents and beneficiary forms. One possibility is using trusts to provide income for your new spouse if he or she survives you, while ensuring that assets flow to children from a prior marriage. A lawyer might suggest a postnuptial agreement to set out how your assets would be divided in case of divorce.

If You're 50 or Older

• Revisit your retirement strategy.

Getting wed later in life can have a big impact on the savings you'll need to retire comfortably, as well as the timeline for when one or both of you quit working, says Marilyn Timbers, a retirement coach at Voya Financial Advisors. "You need to review and reassess your current goals and create a plan for both of you," she says.

You can use a tool such as the T. Rowe Price retirement income calculator to determine how your ages, savings, pensions, and likely Social Security earnings will affect what you'll need for a comfortable retirement. If this exercise makes you feel as if you're behind pace, take advantage of the increased catch-up contribution limits on tax-deferred retirement accounts available to those age 50 and older.

Such planning is especially crucial if you and your partner have an age gap greater than five years, as 44% of remarried men and 38% of remarried women do, according to the Pew Research Center.

For instance, 20% of remarried men have a spouse who is at least 10 years younger. That gap might lead these women to retire earlier than they would have otherwise. Given that women typically live five to 10 years longer than men, these wives need to prepare for what could be many years as a widow.

• Maximize your Social Security.

The closer you are to retirement, the more likely it is you already had a plan for when to start benefits. Revisit that as a duo. It often makes sense for one person, typically the higher earner, to put off collecting until age 70 in order to maximize the potential survivor benefit for the other. Depending on your ages and whether you are both working, it might be advantageous for the other spouse to collect as early as age 62.

To weigh your options, you could use a service such as MaximizeMySocialSecurity.com ($40) or Financial Engines' free Social Security planning tool.

If you were previously married, retirement benefits based on an ex-spouse's work record will typically no longer be available, says Boston University economics professor Laurence Kotlikoff, coauthor of Get What's Yours: The Secrets to Maxing Out Your Social Security. But if you remarry at age 60 or later, you'll still be able to collect survivor benefits if your ex-spouse should die, provided you and your ex were married for at least 10 years.

That means you may have the option at some point to choose among a survivor benefit from your ex, a spousal benefit on your new spouse's record, and your own earned benefit.

• Talk about your future care needs.

Did either of you own a long-term-care insurance policy or decide that it doesn't make sense? That's a conversation to have again—now that you're a couple.

"When you're single, it doesn't matter so much if a health issue runs down your savings," says Kahler. Worst case: Medicaid kicks in once you deplete most of your assets. But if you're married, "it's always the surviving spouse that is most affected when there are significant health costs."

Couples with investable assets between $250,000 and $2 million should seriously mull insurance, he adds. They are the people who may be able to afford the steep premiums but could see their finances undone by the costs of a home health aide or assisted living.

Some policies let spouses share their coverage for greater flexibility. But keep in mind, the older you buy, the higher the premium, which is why the prime age to buy is 55 to 65, Kahler says.