4 Ways to Motivate Yourself to Save and Invest Like a Millionaire

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

In the first three installments of the series "How to Reach $1 Million," you learned key investing strategies for millionaires-in-the making, tips for boosting your salary, and strategic ways to lower your taxes. Part Four below offers smart ideas to inspire, cajole, or even trick yourself to save and invest more efficiently.

Visualize yourself in the future

Here's a really simple exercise that can help you save: Imagine what you would look like in your golden years. The fact is, people who see digitally altered images of themselves as seniors are willing to save more for retirement than those who don’t, according to research by Hal Hershfield, assistant professor at UCLA's Anderson School of Management.

One study found hypothetical paycheck contributions rose from 5.2% to 6.75%. In another, people were asked how they would allocate a windfall of $1,000. The researchers found that the people who were exposed to their future selves put almost twice as much into the long-term savings account than those who were not exposed to their future selves.

So go to the AgingBooth app or click on faceretirement.merrilledge.com to see the future—and fix it.

Visualize your future income

A 2014 study by researchers at Stanford and the University of Minnesota found that providing savers with more information — specifically, projections of their future income along with general financial education — can encourage them to save more toward their retirement.

The good news is, this is something that a growing number of 401(k) plans provide routinely in their statements. If yours doesn’t, use the retirement income calculator at Money.com.

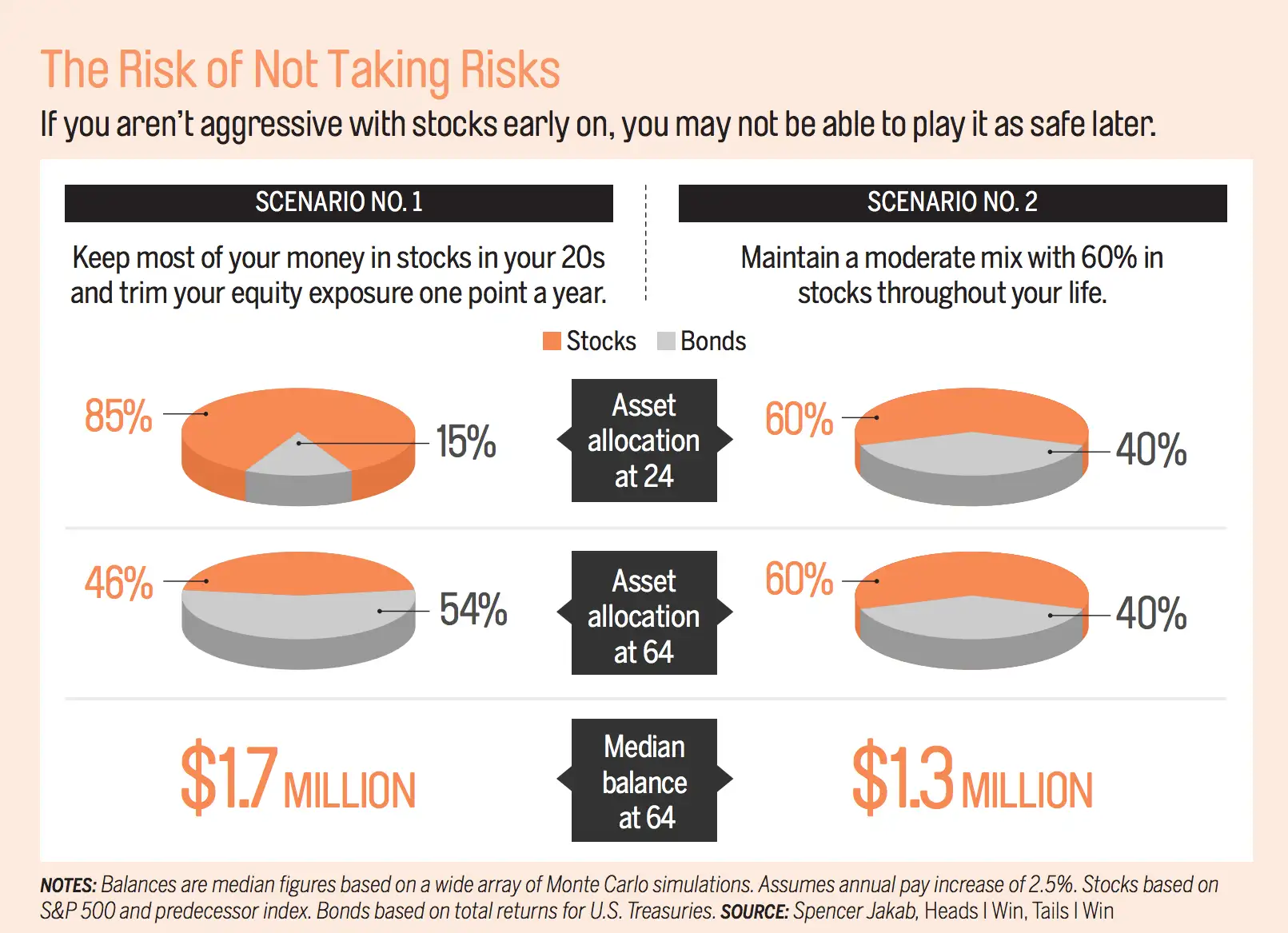

Use risk as a motivational tool

It’s impossible to predict the future, except for this: When you’re five years or so from retiring, you’ll have to cut back on risk by reducing your stocks, perhaps to a 50% stake or less. That’s because if a bear market strikes, you won’t have time to recoup your losses before having to tap your nest egg.

To be able to afford such a conservative stance, though, you have to take risks at other stages of life. “If you embrace risk at the right time, you can actually reduce it over the long term,” says Spencer Jakab, author of Heads I Win, Tails I Win.

Take Our Quiz: Do You Have What It Takes To Be a Millionaire

A perfect example is in the chart below. If you had 85% of your money in equities when you were young—and gradually reduced that over time—you could afford to keep less than half your money in equities at retirement. And you’d still be better off than investors who kept 60% of their portfolios in stocks throughout their lives. The takeaway: If you want the flexibility to play it safe later, you must take a fair amount of risk while you’re young.

Own up to your mistakes

There are going to be times when you make the wrong decision. The key is accepting responsibility and moving on appropriately. "Investors too often have difficulty acknowledging their mistakes," says Meir Statman, a finance professor at Santa Clara University. In stock picking, this can lead to hanging on to laggards out of pride rather than cutting losses.

Emotions can also creep in when you fall short of a goal. Say you're 45 with $200,000 saved and you're socking away $10,000 a year. Maybe you were hoping to hit $1 million by 65 by earning 7% a year. But what if you wind up gaining just 5.5% annually?

You could try to make up for this shortfall by ramping up risk. But a more rational response is to boost your annual savings by about $2,500, which will get you back on track for seven figures with far more certainty.