3 College Grads With $100K in Loans Get Advice on Their Debt

- How to Pay Off Student Loans Fast

- How Student Loan Borrowers Can Prepare for Big Changes Coming in 2023

- Here's Exactly What the Student Loan Forgiveness Application Will Look Like

- Student Loan Payment Pause Extended Through End of 2022

- Millions of Borrowers Just Got a Quicker Path to Student Loan Forgiveness

Our experts give three very different borrowers advice on paying off their student loans.

Student loan borrowers tend be young and inexperienced when it comes to debt, credit, and even basic budgeting.

That can make the transition to repayment after graduation challenging at best. It doesn’t help that student loans carry unfamiliar terms, that there are different rules for different types, or that an array of repayment options can drastically affect your monthly payment, the total amount you pay, and your tax bill.

That’s where Money comes in. We found three borrowers who needed guidance on repaying their loans and matched them with experts: a financial planner, a student debt counselor, and a lawyer who specializes in student loan laws. (See more about the experts at the end of the story.)

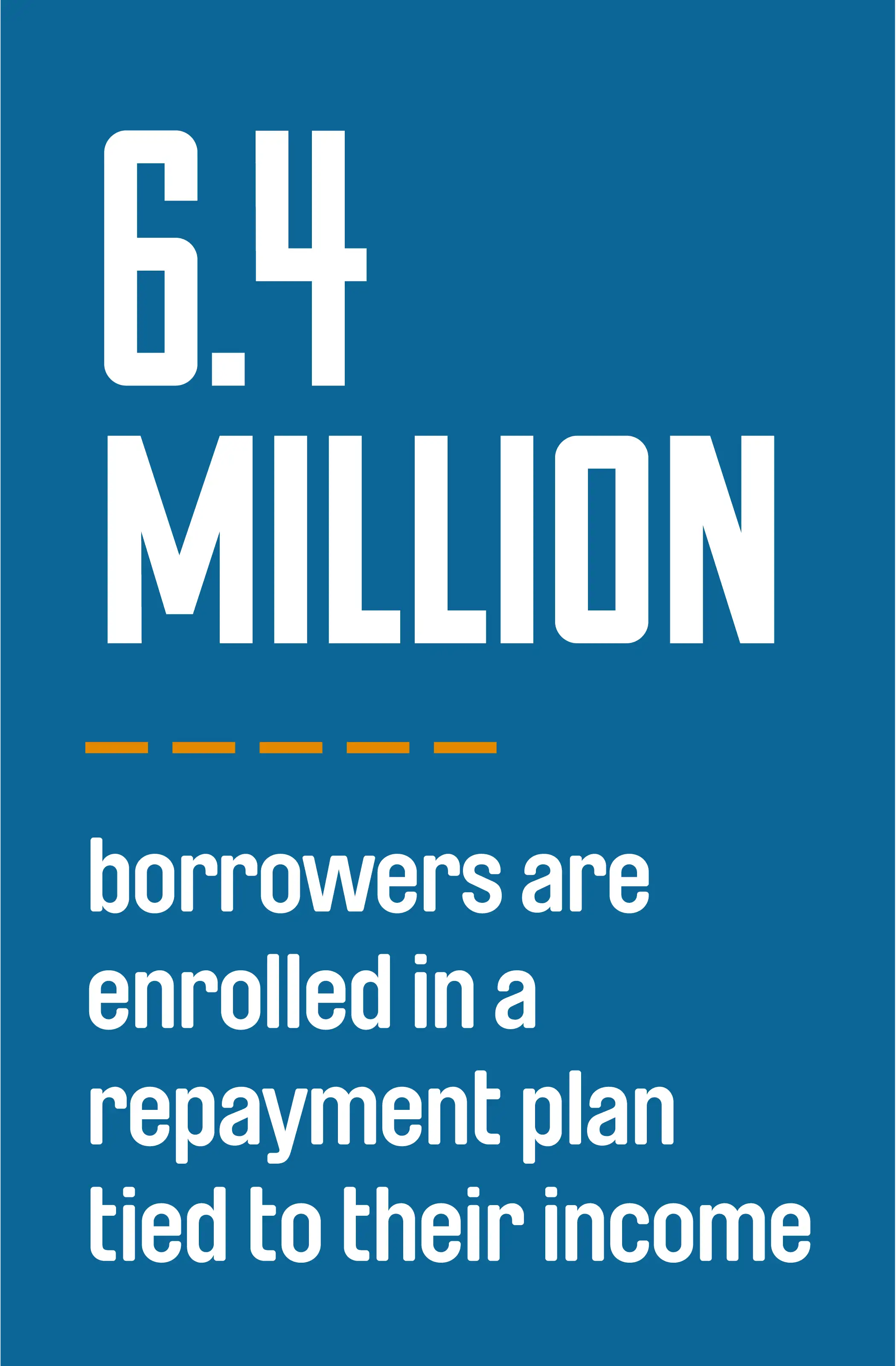

The borrowers are at different stages of the repayment process and have distinct questions about their loans. But their stories are common enough that many of the 41.5 million Americans with student debt—including perhaps you—can find some useful advice in what our experts had to tell them.

[time-anchor title="Mattie Talbert"]

Above: Mattie Talbert (left) and her mother pose for a photo last May before Talbert graduated from the University of South Carolina. She switched majors before ultimately deciding to be a teacher and complete a one-year master’s degree program at USC.

A New Teacher Learns How Get Her Loans Forgiven

–––––

AS AN UNDERGRADUATE, Mattie Talbert committed a common but costly error: Unsure what she really wanted to do in the future, she switched academic programs multiple times.

She spent a year taking classes at a community college before transferring to the University of South Carolina-Columbia. She thought she wanted to be a nurse but quickly discovered science wasn’t her strong suit. She then took some speech pathology courses and found that field wasn’t right for her either. She ultimately graduated with a degree in English.

“I come from a long line of teachers, and I wanted to do something different,” Talbert says. “But the more I thought about it, I realized [teaching] was my calling.”

At 27, she’s now about three months into her first teaching job, happily working as high school English teacher in Columbia, S.C.

In all, it took her some seven years to earn an undergraduate degree. That, along with a one-year master’s degree program, also at USC, left her with a debt load of $112,348 in federal loans, plus about $44,000 in private loans.

Now, despite her efforts to learn about her options, she’s confused about the best way to pay those debts down.

THE EXPERTS' ADVICE Teachers often qualify for multiple loan-forgiveness programs. The best known are the federal government’s 10-year Public Service Loan Forgiveness (PSLF) program, designed for any public sector employee, and the federal Teacher Loan Forgiveness program, which forgives up to $17,500 after five consecutive years of teaching in schools that serve low-income students. There are also dozens of city- and state-sponsored teacher forgiveness programs. (The American Federation of Teachers has a list of teacher-specific forgiveness programs here.)

You can’t take advantage of both federal forgiveness programs at the same time. In most cases, including Talbert’s, Public Service Loan Forgiveness will be a better financial deal than the Teacher Loan Forgiveness.

Under PSLF, Talbert has to work in a qualifying job (in her case, at any public school) for 10 years and make on-time monthly payments during that period. After a decade of payments, whatever debt is left over will be forgiven.

“The sooner you start payments, the sooner you get forgiveness,” notes Fred Amrein, a financial planner in Wynnewood, Pa.

Talbert has 17 individual loans, and only some of them automatically qualify for the income-driven plans that lead to loan forgiveness. So her first step is to fill out a form to consolidate all her federal loans into one new loan under the Direct Loan program. (For Talbert, there’s little downside to consolidating her loans, but that’s not always the case. Read more about that here.)

“You don’t want to be surprised years later if you switch jobs and were planning to have your loans forgiven… only to find out that you don’t qualify”

Next, Talbert has to figure out which of the five income-driven plans she qualifies for and should enroll in.

Amrein says Talbert may qualify for the Pay As You Earn plan, which is open only to borrowers who took out loans after Sept. 30, 2007. There are a couple of advantages to that plan, but for Talbert, the main one comes into effect if she gets married in the next 10 years, Amrein says. That’s because her spouse’s income won’t affect her loan payments under PAYE as long as the two of them file separate tax forms.

If she doesn’t qualify for the Pay As You Earn plan, Talbert should enroll in the newer Revised Pay As Your Earn (REPAYE).

Finally, Talbert should fill out a form for the Department of Education to certify that her teaching job is qualified. (You can download it here.) This isn’t required in order to collect public service forgiveness, but it can help borrowers make certain that they qualify and establish a paper trail for when it's time to claim forgiveness.

Jessica Ferastoaru, a student loan counselor with Take Charge America, recommends Talbert and other potential applicants fill out the form every year, or at a minimum, any time they change jobs.

“You don’t want to be surprised years later if you switch jobs and were planning to have your loans forgiven… only to find out that you don’t qualify,” Ferastoaru says.

There are some important ongoing steps in pursuing PSLF that Talbert needs to be aware of. For one, she has to remember to recertify every single year to remain in a qualifying income-driven plan. That means she needs to update her annual income, based on her most recent tax return, with her loan servicer. Monthly payments under income-driven plans can change each year because of this, which means as Talbert’s income increases, so, too, will her monthly payments.

Regardless, those complications don’t outweigh the benefits—namely that Talbert would save at least $100,000 in loan repayments under the forgiveness plan.

It’s hard to pinpoint exactly how much Talbert will have forgiven, since it depends in part on her take-home pay over the next 10 years and which plan she enrolls in.

But to demonstrate the savings PSLF will give her: If she were to earn the same salary for the next 10 years, she’d pay less than $30,000 total. If she were to pay off her entire debt in that same 10-year period, she’d pay close to $150,000 based on her principal plus interest.

“You’re a perfect candidate for the (PSLF) program,” Ferastoaru told Talbert. “It’s supposed to reward borrowers for staying in public service jobs.”

As for Talbert’s private loan, Ferastoaru and Amrein both recommend she devote any extra money to paying it off as quickly as possible. The loan carries a 10.5% interest rate, which means it is significantly more expensive that her federal loans.

MATTIE'S PLAN, IN BRIEF

Talbert should consolidate her federal loans into one new loan so she’s eligible for an income-driven repayment plan, for which her monthly payments would be less than $175 a month. Then she should take advantage of a benefit for public school teachers by pursuing 10-year federal Public Service Loan Forgiveness. Finally, she should prioritize paying down the costly private loan.

[time-anchor title="Taylor Villanueva"]

Above: Taylor Villanueva graduates from the University of Southern California in December and hopes to find a job in public relations, but she’s worried about earning enough to afford her student loan payments.

A Daughter Wants to Pay Off Her Family’s Parent PLUS Loans

––––––––––

WITH TWO MONTHS TO GO before her graduation, Taylor Villanueva is at a stage that will be familiar to any recent college grad—excitement mixed with uncertainty.

Villanueva, though, is facing significant financial unknowns, namely what kind of work she’ll pursue after graduation, how much she’ll earn, and how she’ll manage her massive monthly debt burden.

Villanueva will graduate in December from the University of Southern California owing $123,451. If she goes on a standard 10-year repayment plan, her monthly payments are likely to be over $1,400.

(That debt load is not representative of most undergraduates, who finish college with debts closer to $30,000. But Villanueva financed her undergraduate degree through federal Parent PLUS loans, which allow you to borrow up to the full cost for every year of school, unlike undergraduate loans, which max out at $31,000 total for dependent students.)

“I got a little overwhelmed when I saw how much I was in debt,” Villanueva says. “My whole life I’ve been a saver.”

In fact, she made several payments over the course of her two years at USC—contributing about $10,000 from her savings. But she felt that hardly made a dent given how quickly interest was accruing.

THE EXPERTS' ADVICE Villanueva, unfortunately, is in a tough position for an undergraduate borrower. Parent PLUS loans are more expensive than undergraduate loans, with higher interest rates that start accruing the day you take them out. Parent loans also don’t qualify for the same income-driven repayment plans as loans designed for students.

Legally speaking, the Parent PLUS loans, which are in her mother’s name, are not Villanueva’s responsibility, says Adam Minsky, a lawyer in Boston who specializes in student loan repayment. And because of that, even if Villanueva will be the one providing the money to repay them, all loan forgiveness and reduced payment opportunities will be based on her mother’s employment and income, Minsky explains.

One of the easiest ways Villanueva can make her monthly payments more manageable is by consolidating her five loans and enrolling the new loan in an extended payment plan, which offers lower monthly payments in exchange for a longer repayment period, says Jessica Ferastoaru, a student loan counselor with Take Charge America. Choosing a “graduated” extended plan, in which payments increase gradually, would reduce her payments to $735 a month for the first two years, the lowest payment she can get, Ferastoaru says. Villanueva could also enroll in a fixed extended payment plan, in which her payments would be the same each month for all 30 years, although they’d be about $80 a month higher than the graduated plan at the beginning.

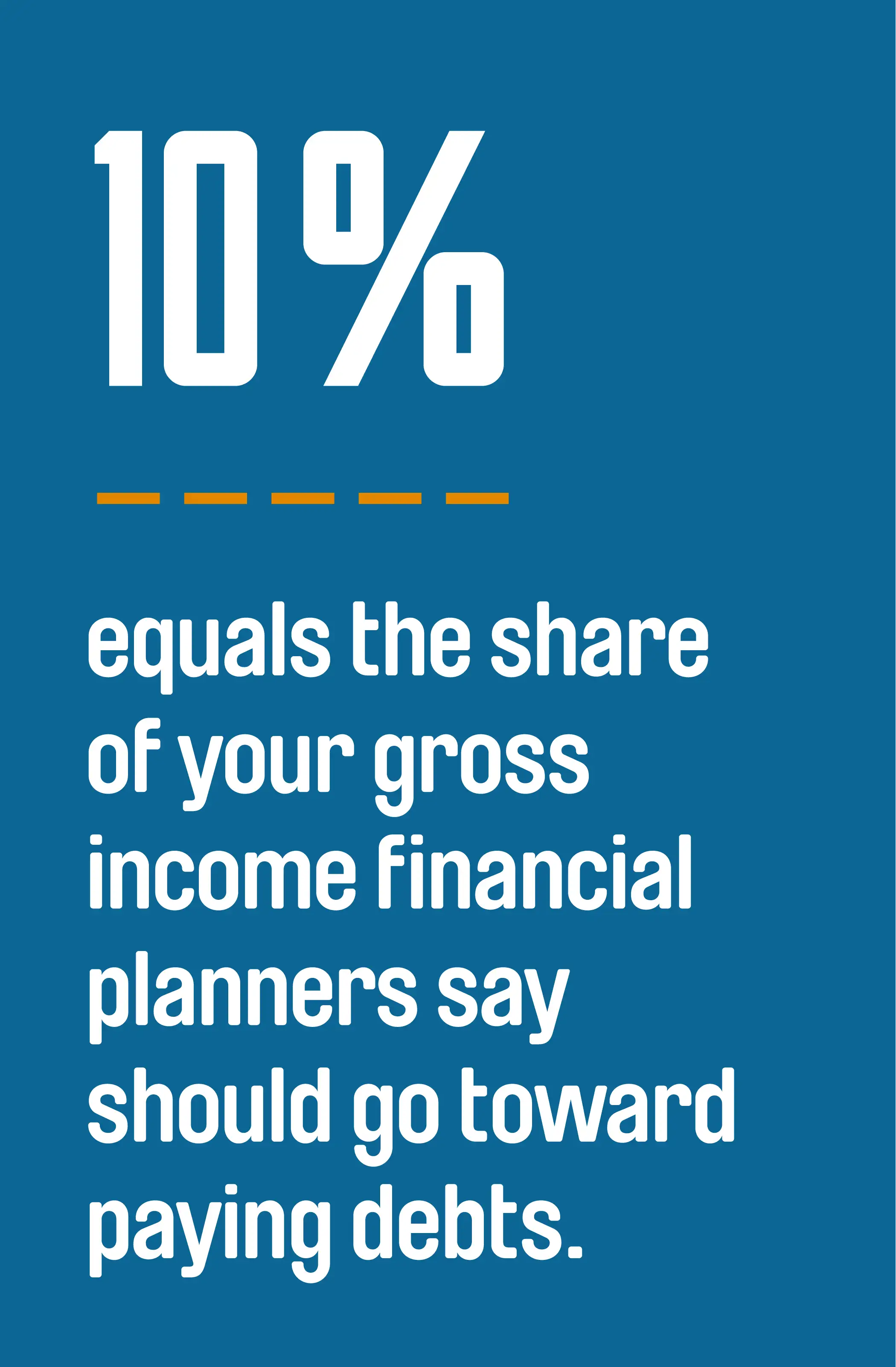

If Villanueva chooses the graduated plan, she’d owe $8,820 a year to start. She doesn’t expect to make more than $50,000 annually in her first years in the workforce. That means her payments would be about 18% of her gross income. While that’s above the recommended amount (most planners suggest closer to 10%) Villanueva says she thinks she can handle it by living at home.

There is a significant downside to drawing out payments over 30 years, though it’s one Villanueva likely can’t avoid. Under a 30-year plan, she’ll pay close to $300,000 on her student loans, more than half of it in interest.

A second option Villanueva could consider is an income-contingent repayment plan (ICR), the only income plan that’s available to Parent PLUS borrowers. And ICR could be an especially attractive option for the family, because Villanueva’s mother, Rose Villanueva, works at a public school, which means her loans can qualify for Public Service Loan Forgiveness (PSLF).

To access ICR, Parent PLUS borrowers first have to consolidate into the Federal Direct Loan program. Monthly payments can then be set to 20% of discretionary income, defined as how much your take-home salary exceeds the poverty line. Under that plan, Ferastoaru estimates Villanueva’s monthly bill would start at $1,178, based on her mother’s income. After 120 payments on this plan, the outstanding debt would be forgiven.

“In the long run, it’s cost effective to do that,” Ferastoaru says. “It’s just a question of whether it’s affordable now.”

One hiccup in PSLF for the Villanueva family is that Rose Villanueva still has some of her own student loans, and those also may qualify for an income-driven plan and loan forgiveness.

If the family does decide to consolidate the Parent PLUS loans, it’s vital that the parent loans be kept separate from her mother’s own loans, Minsky stresses. Because parent loans are locked out of the more generous income-driven plans, combining the two sets of loans would effectively exclude Rose Villanueva’s own loans from those more flexible plans as well.

TAYLOR'S PLAN, IN BRIEF

Villanueva has several options, but no matter what, she’s looking at a minimum of 10 years of payments likely to be over a $1,000 a month. Her options are complicated, since they also depend on her mother’s employment, income, and tax-filing status. Minsky recommends the Villanueva family run the numbers of each scenario using the federal government’s student loan repayment estimator.

[time-anchor title="Evan Bolick"]

Evan Bolick stands with his newborn daughter, Madelyn, and son, Ridley, at a rodeo in Arizona. Evan says that becoming a father motivated him to figure out his finances.

A High-Earning Lawyer Debates Whether to Stay in an Income-Driven Plan

–––––

EVAN BOLICK HAS PAID his monthly student loan bill on time every month for about five years. He even makes a habit of overpaying—sending in $625 each month for his $564 bill.

Still, Bolick watches as his principal, now at about $125,000, continues to grow.

That’s because like a lot of borrowers in an income-driven plan, Bolick’s minimum payment—determined by a formula that accounts for his take-home pay, family size, and the federal poverty line—doesn’t cover the monthly interest on his loans. In finance lingo, he’s negatively amortized.

“You’re paying interest on interest now,” says Fred Amrein, a financial planner and expert in college financing based in Wynnewood, Pa.

Bolick, 32, was able to complete his undergraduate degree from James Madison University with roughly $5,000 in loans. But law school was a different story.

After he earned his degree from the University of North Carolina at Chapel Hill School of Law in 2010, Bolick worked as a clerk for a judge. His salary was low compared to his six-figure law school debt, so he chose to defer some of his loans.

“It so vastly increased the amount of money I owed,” he says. “But I’d never had real debt before. At the time, I thought it was a real blessing.”

Now Bolick is trying to make progress on his loans while also paying a mortgage, saving for retirement, and contributing to his children’s college fund.

THE EXPERTS' ADVICE Like most borrowers, Bolick has several options for continuing his loan repayment, each with its own strings attached. He’ll have to decide which strategy he’s most comfortable with.

Bolick’s current monthly payment is based on his salary prior to two recent raises, so when he completes the required annual recertification in February, his monthly payments are going to jump significantly. Amrein estimates they’ll be closer to $1,000 a month going forward if he remains on the same income-based repayment plan.

The main question for Bolick is whether he should remain in an income-driven plan or switch to a balance-based plan, in which he’d make equal monthly payments based on his loan balance for the rest of his repayment term.

Under an income-driven plan, his payments would change each year with his income, and if his wife begins working again full-time after their kids start school, that additional income would be counted unless the couple do their income taxes as married filing separately. If Bolick remains in an income-driven plan, though, he’d be eligible for loan forgiveness after another 20 years of payments.

"Under current rules, any debt that’s forgiven through an income-driven plan would be counted as income in the year it’s forgiven."

But there’s a potentially important consequence to that detail: Under current rules, any debt that’s forgiven through an income-driven plan would be counted as income in the year it’s forgiven. Most borrowers, Bolick included, are surprised to learn that. Amrein estimates that at the rate he’s going now, Bolick could have as much as $100,000 forgiven, meaning he’d owe the IRS tens of thousands of dollars.

Minsky recommends Bolick go online to the National Student Loan Data System (nslds.ed.gov) to see how much unpaid interest is currently accruing and to figure out how much he’d have to pay each month to start chipping away at the principal. Then he needs to compare those monthly payments with what he’d pay on a balanced-based plan, or a plan with equal monthly payments based on the amount owed.

“The fact that you’re able to overpay tells me you have some flexibility there,” Minsky says.

If it turns out that Bolick’s payment increases so much under his income-driven plan that it’s close to the amount he’d pay under a balance-based plan, then it may make sense for him to switch to the latter. (If his income drops in the future, Bolick can always go back to an income-driven plan.)

However, if Bolick decides his income-based plan is a better fit, Minsky says he could ease his worries about a massive future tax bill by setting up a long-term savings plan to pay that bill. It’s also possible Congress will pass legislation in the next 20 years to remove the tax penalty for forgiven student loans, Minsky says. But if that doesn’t happen, Bolick would have a contingency plan.

“Don’t not pick a good plan for you because you’re worried about this possible tax bill,” Minsky says.

Finally, if Bolick continues to pay more than the minimum each month, Minsky recommends that he direct any extra money to the loan with the least amount of accrued interest, or in other words, whichever one he could start reducing the principal on the quickest.

Amrein and Minsky also both advised Bolick against two other repayment strategies he was curious about: taking a loan from his 401(k) retirement plan to pay down his student loans and refinancing his debt with a private company. If Bolick were to leave his job, a loan from his 401(k) would have to be repaid within 60 days or it would be taxed as income, Amrein says. And while Bolick would probably qualify for a lower interest rate through refinancing, he wouldn’t be able to return to one of the federal government’s income-driven repayment options if he were to switch to a lower-paying job.

EVAN'S PLAN, IN BRIEF

Overall, Amrein says Bolick has made some good decisions balancing his financial priorities so far, whether by accident or by design. “Probably both,” Bolick says, laughing. Now, he needs to decide whether his rising income means his income-based payments have reached a level where he’d be better off in a balance-based plan. Big life changes, including a move back to the East Coast and a new job for Bolick, could also change which plan is best for him.

[time-anchor title="Meet Money's Loan Experts"]

Fred Amrein

Amrein founded his own financial planning and college financial consulting firm, where he specializes in helping clients build a long-term plan, from undergraduate programs to graduate school through to repayment. He’s the author of Financial Aid and Beyond: Secrets to College Affordability, and has developed a software program that helps families analyze college costs, financial aid opportunities, and student loan repayment options.

Adam Minsky

When Minsky graduated from law school and started paying off his loans, he found his loan servicer was of little help in answering his questions. He turned that into a career, and he’s now one of the few attorneys in the country devoted exclusively to helping student loan borrowers. He’s also the author of three guidebooks on student loans, and contributed to the National Consumer Law Center’s 2015 edition of Student Loan Law.

Jessica Ferastoaru

Ferastoaru is a student loan counselor with Take Charge America (TCA), a national nonprofit credit counseling agency. She works with student loan servicers, guarantors, collection agencies, and the federal ombudsman to resolve borrowers’ issues. She also oversaw research and development of the student loan counseling curriculum for the Student Loan Alliance, as well as the Financial Counseling Association of America.

Graphic sources: The Institute for College Access and Success, Federal Student Aid data center, New York Fed Consumer Credit Panel, American Bar Association.