Waiting for Baby: $55,000 and Counting

Carrie and Dan Zampich have been struggling with infertility for

five years. Their debt is mounting and the biological clock is ticking,

but the couple remain hopeful as they pursue costly treatment

while trying to limit the financial damage.

Carrie and Dan Zampich went to the fertility clinic almost on a whim. The Atlanta couple, then 36 and 41, had been trying unsuccessfully to get pregnant for nine months, so when Carrie spotted a billboard for the center on her drive home from work one day, she figured it would be a good idea for the two of them to get checked out. The specialist’s blunt diagnosis stunned them: Dan had a congenital condition that blocked the release of his sperm, and the couple had less than a 1% chance of having a baby naturally.

The doctor recommended a procedure to extract Dan’s sperm, followed by in vitro fertilization (IVF) to try to create an embryo Carrie could carry to term. The Zampiches agreed on the spot and were whisked off to the clinic’s business office to make the arrangements. That’s when they received their second shock. The procedures would cost $18,000, they were told, plus another $2,000 for medications—and their health insurance wouldn’t cover any of it. When the Zampiches replied that they didn’t have the money, the business manager handed them an application for a medical loan—at an interest rate of 25%. They walked out. Says Carrie: “We couldn’t afford it.”

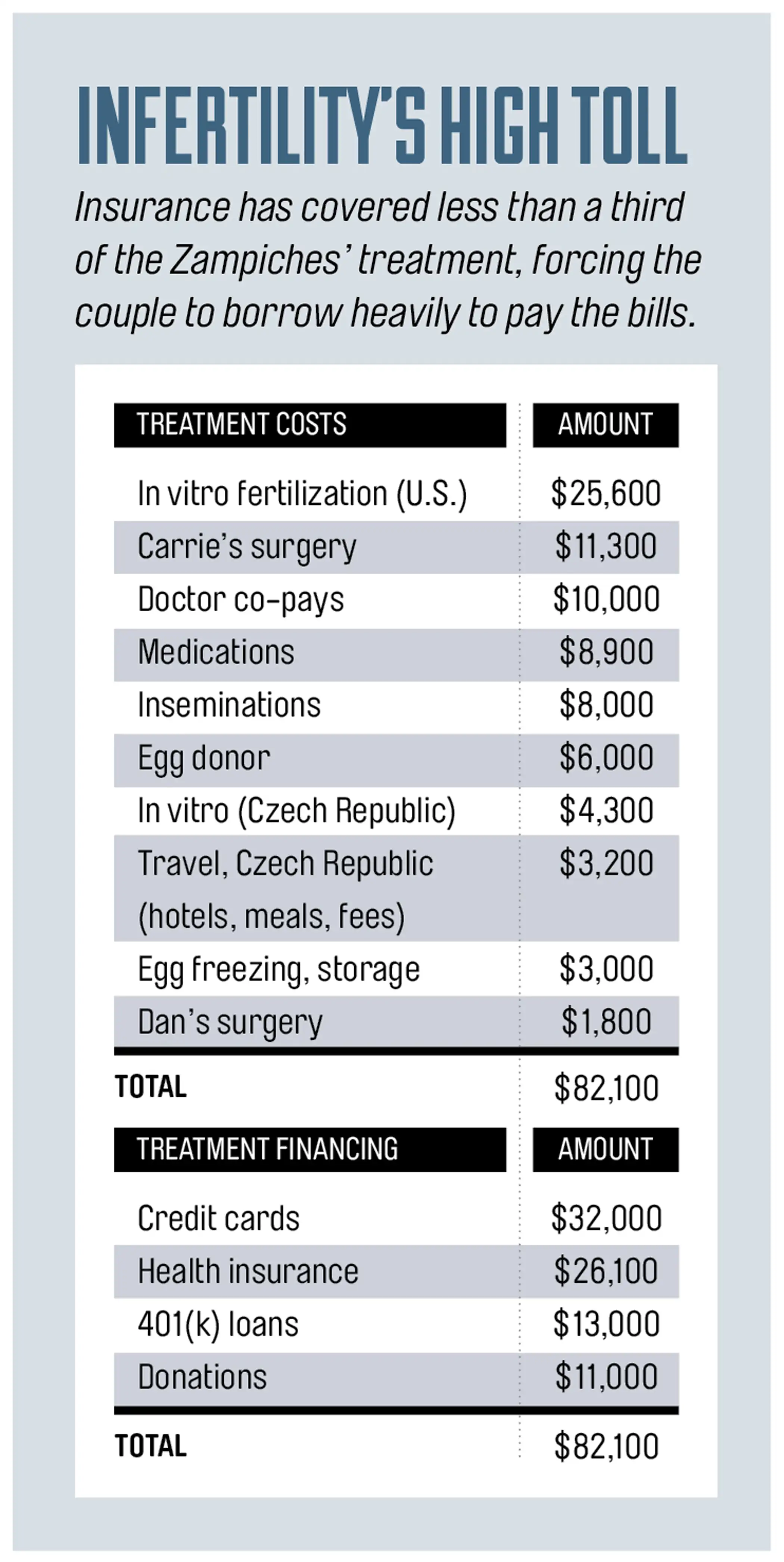

That moment marked the beginning of the couple’s long struggle to have a baby, which has taken an enormous emotional, physical, and financial toll on their lives. Over the past 4½ years, Carrie, a media promotions specialist, and Dan, a graphic designer, have seen seven specialists and undergone 11 medical procedures costing more than $80,000; of that total, $55,000 has come from their pockets. Stretched thin by medical bills, the couple have struggled to pay for treatment: They’ve borrowed against Carrie’s 401(k) plan, maxed out their credit cards, taken donations from family and friends, and routinely worked side jobs for extra cash. “We aren’t ready to give up, but if we do,” says Carrie, “it will be because of money, no other reason.”

Like the Zampiches, about one in five couples in the U.S. has difficulty conceiving (one in three if the woman is older than 35). Yet only about 25% of health plans provide coverage for infertility treatment, according to Resolve: the National Infertility Association.

Even plans that offer fertility benefits often exclude medication and other related expenses and cap the amount covered or limit the number of IVF cycles allowed (two to four is common). Considering that couples often do three or four cycles before conceiving, at an average cost of $12,600 for each, insurance can run out fast. Couples who have coverage typically end up spending only about $2,100 less than couples who don’t, according to a recent study by James F. Smith, a urologist and a director at the Center for Reproductive Health at the University of California at San Francisco. “The high costs are a significant burden on household finances,” says Smith, “and play a major role in fertility treatment decision-making.”

Financial considerations have certainly driven many of the treatment choices that Carrie, now 41, and Dan, 46, have made. But rather than saving them money, the decision early on to pursue lower-cost options that possibly had less chance of success may wind up costing them more in the long run. Meanwhile, they are deeply in debt, including $43,000 on high-interest credit cards, which has forced them to put on hold other goals, such as buying a house and saving for retirement, despite their $126,000 combined annual income. “We don’t go out because we need to save money; we don’t shop because we need to save money,” says Carrie. “Our lives are being held captive by this quest.”

[time-anchor title="Going Abroad for Baby"]

When the Zampiches were first told how costly fertility treatment would be, the timing could hardly have been worse. Nine months earlier they’d tapped all their savings and charged another $10,000 to pay for their wedding. Shortly after, Carrie was laid off. Though she was rehired a few months later, the bout of unemployment meant they’d been unable to pay off the credit cards or replenish their savings. So adding $20,000 to their debts to pay the fertility clinic’s fees seemed out of the question.

Instead they went home and Googled “low-cost IVF.” Carrie’s search turned up an Atlanta company called My IVF Alternative, which arranges trips to the Czech Republic, where in vitro treatment costs substantially less than in the U.S. Carrie contacted several clinics to compare pricing, but the Czech program turned out to be the most affordable: $3,500 for the entire bill. She contacted several couples who’d posted about their success stories on the company website, all of whom confirmed positive experiences that had resulted in conception. She and Dan decided to move forward with the program, not considering that online testimonials provided by the company might not be entirely representative.

In addition to the program fee, the Zampiches needed money for plane tickets and hotels. At her friends’ encouragement, Carrie began blogging about their experience and set up a personal crowdfunding website at GoFundMe.com for friends reading the blog who wanted to contribute. That brought in $3,000.

At Christmas, Carrie’s parents and her two sisters, brother, and their spouses surprised the couple by forgoing gifts for one another and instead giving the cash they saved on presents—$2,000 in all—to the Zampiches for their trip. “Every box we opened had money,” says Carrie. One of Carrie’s sisters and a friend donated their miles for the plane tickets. On their second anniversary, in March 2011, they were on a plane to the Czech Republic.

“We thought it would be one and done,” says Dan. Then Carrie didn’t get pregnant. “It shook me to the core,” says Carrie. “I couldn’t go 12 hours without crying.”

[time-anchor title="Trying Some of Everything"]

Looking to find out why the IVF didn’t work, Carrie went to her gynecologist when they returned from the Czech Republic. The exam turned up a polyp on her uterus that could make it harder to conceive. Hopeful that removing it would boost the chance of pregnancy, Carrie had surgery in May 2011. Because it was a medical issue, not an infertility treatment, the couple’s insurance paid for all but about $700, which Carrie put on a credit card.

Then the Zampiches returned to the clinic that first diagnosed Dan’s problem. They asked whether there were any lower-cost options they could pursue, such as being part of a clinical trial. No luck. The center had just finished an IVF trial offering free care to participants and didn’t have another one scheduled. And the couple’s income was too high for them to qualify for one of the grants that the facility offered to help defray costs.

One other option, they were told, was artificial insemination, which would cost just $2,000 and offer them a one-in-three chance of conceiving. The catch: They’d need to use donor sperm.

Dan was initially reluctant. “We felt so desperate because with our ages, time was running out,” says Carrie. “It was a miserable time for us.” The strain sent the couple to marriage counseling, which led Dan to have a change of heart. He realized, he says, “I wanted to be a dad more than anything.”

To pay for the procedure and get rid of their remaining wedding debt, Carrie took out a $16,000 loan from her 401(k), using $10,000 to pay off their credit cards and $6,000 for three rounds of artificial insemination over several months in 2011. None, though, resulted in a pregnancy.

The next step, they decided, was for Dan to have surgery to correct his blockage. Then they could try to conceive naturally. They hadn’t considered the operation earlier because the doctor they’d originally consulted had said it could take up to two years after surgery for the problem to resolve completely—time the Zampiches felt that they just didn’t have. Now, though, fresh out of money and other low-cost options, the couple decided to go ahead. Their health insurance from Dan’s employer wouldn’t cover the operation, but Carrie’s work plan would, so they switched during open enrollment.

Just days before the operation, however, Dan’s urologist refused to submit a claim to the insurer, saying the procedure was elective, not medically necessary. That meant the Zampiches would have to pay the $1,800 bill out of pocket.

For Carrie, who’d put on 40 pounds during the couple’s struggle to conceive, the stress proved too much; her blood pressure shot up, and she had to be hospitalized. In the end, though, they moved forward with the operation. “Very few doctors do the procedure in our area, so we felt like we had no choice,” says Carrie. She charged the surgery on her American Express card, planning to pay off the balance when the bill came due. But she and Dan came up short. Her dad stepped in, signing over his Social Security check to cover it.

Nine months after the surgery, however, Carrie still hadn’t gotten pregnant. Says Dan: “It felt like we just wasted so much time and so much money.”

[time-anchor title="Back to Square One"]

By the fall of 2012 the Zampiches decided to try IVF again, the procedure they’d originally been told offered them the best chance of conceiving a baby. Working with a list of centers recommended by her ob/gyn and searching Google againfor low-cost IVF, Carrie this time researched success rates as well as pricing. She found a well-regarded clinic in Augusta, 2½ hours away, that charged half as much as the centers she’d contacted in Atlanta. They did their second IVF round in November 2012, putting the $8,000 bill on two credit cards. A friend gave them $3,000 to pay for the hormone meds Carrie needed to take prior to in vitro to stimulate egg production and control ovulation. Still, no pregnancy.

Reluctant to take on any more debt or accept money from friends and family, Carrie contacted the human resources department at her company to lobby for infertility coverage. Much to her surprise, her employer had another plan that did provide fertility benefits. She had just missed the enrollment window but was advised to write a letter to the insurer, and she was accepted into the plan.

The news was both reassuring and upsetting. Thrilled that she had coverage, Carrie was also angry that she hadn’t discovered this option sooner. The plan would cover the entire bill for IVF except for the medications needed to stimulate hormone production.

To help defray those costs, the Zampiches got creative. They applied for scholarship assistance with the drug manufacturers but were turned down because their income was too high. Undaunted, they began paying cash for the meds in exchange for discounts of 15% to 30% at pharmacies that specialize in fertility treatments. They also turned to the infertility “black market,” buying leftover medications from women who donated through online support groups, which let the couple pay as much as 80% less than retail prices.

Their third round of IVF in early 2013 didn’t result in pregnancy. But their fourth try last November, at a new clinic closer to home that a friend recommended, finally did. The joy didn’t last long: Just seven weeks into her term, Carrie had a miscarriage. Devastated, Dan said that was the first time he thought about giving up: “I felt like I could come to grips with not having children. But Carrie didn’t.”

“It was our lowest point,” admits Carrie, who still wanted to keep trying. “I want to know we did everything we could, even if it means going bankrupt.”

[time-anchor title="New Approach"]

In January the Zampiches went back to their fertility specialist, who told them bluntly that Carrie’s age, then 40, was becoming more of an adverse factor. He put their chances of having a baby with her older eggs at only about 9%. If they used donor eggs from a younger woman, however, the chance of conceiving shot up to 64%. Both Carrie and Dan were willing. “We can’t just keep rolling the dice,” says Carrie. “I get to carry the baby. That’s enough for me.”

The process, which they’ll undergo this summer, involves trying to create an embryo through in vitro using the donor’s egg and Dan’s sperm; if successful, the embryo will then be implanted in Carrie, allowing her to see the pregnancy through. Health insurance won’t cover the $15,000 cost of the egg donor, but it will cover the IVF. The couple did get into their clinic’s scholarship program, so they are paying $5,000, which they once again charged on credit cards. That brought their total infertility-related debt to $45,000, including $32,000 in credit card balances.

The strain on their resources has left the Zampiches living paycheck to paycheck and occasionally charging expenses unrelated to infertility. Since they don’t have an emergency fund, unexpected bills have been problematic. Among them: $275 to replace Dan’s windshield after a tree limb fell on his car; a $1,300 vet bill when their dog Minnie fell on a tree branch that went through her shoulder; and $450 when their other dog, Mylo, was bitten by a snake. As a result, they have another $11,000 in credit card charges on top of the IVF.

To keep up with their debt payments—$600 a month goes to the 401(k) loans and $1,300 to credit cards—the Zampiches spend much of their spare time doing side jobs. Carrie babysits for friends and family, plus does freelance marketing work. Dan takes on graphic design projects for small businesses and earns about $100 a month dog sitting. All told, the extra work brings in about $1,000 a month.

The couple say they don’t mind using so much of their free time working. “Practically everyone we know has kids, and their lives revolve around their kids, their activities, their school vacations,” says Carrie. “That’s hard to be around sometimes.” Things that used to make them happy often trigger sadness now. Carrie says she no longer attends when children of her family and friends are in Easter and Christmas shows. “The pageants kill me,” she says.

While they are open about their struggles, they get weary of well-meaning advice from friends. “Everyone has an opinion,” says Dan. A flash point is when people ask if they’ve considered adopting. “I have to bite my tongue,” says Carrie. “Of course we have considered it. It’s very costly too and not something we are ready to do now.” In addition to wanting to experience pregnancy, she says, “we want to try to have a child that shares one or both of our DNA. But if that’s not in the cards, so be it, and we will go the adoption route.”

For now they’re focused on their latest attempt at pregnancy—and getting out of the hole they’ve dug for themselves. One thing they know: The financial strain won’t go away if they finally do have a baby, considering the cost of pregnancy, diapers, child care, camp, and, one day, college. Admits Carrie: “We have created a financial mess and really need help.”

[time-anchor title="The Advice"]

To get that help, Money turned to Lee Baker, a financial planner in Atlanta, and Davina Fankhauser, president of Fertility Within Reach, which helps couples navigate insurance benefits. Both Baker and Fankhauser struggled with infertility for years before becoming parents, so they bring their experiences along with their expertise. Their suggestions:

Press for more coverage. So far, Carrie’s insurance has paid $15,500 for treatments, but her infertility coverage is capped at $20,000. After the next IVF cycle, they will have just $4,500 left—not enough for another round if needed.

The Zampiches have one strong negotiating point that they may be able to leverage into a higher maximum, says Fankhauser. She notes that couples who feel financial pressure often opt to have multiple embryos implanted to increase the chances that a single IVF cycle will result in pregnancy. Indeed, that’s the plan for Carrie and Dan. Transferring several embryos at once, however, raises the likelihood of multiple births, a higher-risk pregnancy, and medical complications, which could result in higher costs for the insurance company.

Fankhauser recommends that Carrie and Dan write to the insurance company asking for a higher dollar cap on coverage or to be allowed up to two more rounds of IVF. The letter should lay out the fact that they are using donor eggs, which increases the odds of success, and that if coverage is increased, they would consider a single embryo transfer this time. “Knowing they would have enough to cover future IVFs if the next one doesn’t work gives them less pressure to transfer multiple embryos,” says Fankhauser.

Appeal for reimbursement. Treatment for the same condition may be covered by insurance if it’s characterized as a medical problem but not covered if infertility is cited as the reason for care, says Fankhauser. She believes the Zampiches have a good case to show that Dan’s surgery to remove the blockage should have been covered because he was being treated for a congenital condition.

Fankhauser recommends writing a separate letter to the insurer requesting an appeal; if denied, the couple should file an external appeal with Georgia’s state department of insurance. She says 80% of the people she works with get their denials overturned using one of these two methods.

Melt the plastic. The Zampiches owe $43,000 on 13 credit cards at rates ranging from 18% to 25%. Ouch. Baker urges the couple to earmark an additional $700 a month to paying down this debt, on top of the $1,300 they pay now, which is barely more than the cards’ minimums.

Baker advises putting the extra money toward their lowest-balance, highest-rate cards first—five have balances under $1,000 but rates of 20% to 25%. At that rate, those balances will be erased by year’s end.

Once Carrie’s 401(k) loan is paid off next June, the $600 now deducted from Carrie’s paycheck for repayment can also go toward the credit cards, Baker adds.

Be stingier. To help identify places the Zampiches can cut back to free up the money for debt repayment, Baker had them write down their monthly spending and expenses. He identified nearly $1,000 a month going to discretionary items—mostly spending on entertainment (Dan occasionally splurges on concerts and tech gadgets) and gifts for other people.

That’s too much fun and too much generosity for their budget, Baker says. Case in point: Last Christmas, Carrie let one of her siblings charge $2,000 worth of presents on her Best Buy card. “I get a lot of joy giving gifts, but I know I need to be more realistic about spending,” Carrie admits.

Get priorities straight. The couple’s No. 1 goal, says Baker, must be to build an emergency fund that would cover at least six months’ worth of their expenses. Currently they have no money set aside. Once Carrie’s car loan is paid off later this month, the planner suggests redirecting the nearly $400 in monthly payments into a discrete account earmarked as their rainy-day fund. Dan is up for a raise soon and should apportion part of that extra cash toward their emergency fund as well. Also critical: boosting contributions to their skimpy retirement accounts (only $24,000 invested so far).

The Zampiches also need to budget with an eye to future costs, says Baker. If and when they become parents, they will have child-care bills (both Carrie and Dan plan to continue working) and will need life and disability insurance. That would add at least $1,700 to their monthly budget.

Carrie and Dan say they’d be only too happy to be in a position where they’re budgeting for a baby. And for the first time in a long time, they’re hopeful that may be the case soon. “I see a light at the end of the tunnel,” says Carrie. “I keep telling myself one day it will all be worth it.”

Related:

- Three Ways to Cut the High Costs of Infertility

- How High-Tech Baby Making Fuels the Infertility Market Boom

- Trouble Conceiving? These Resources Can Help