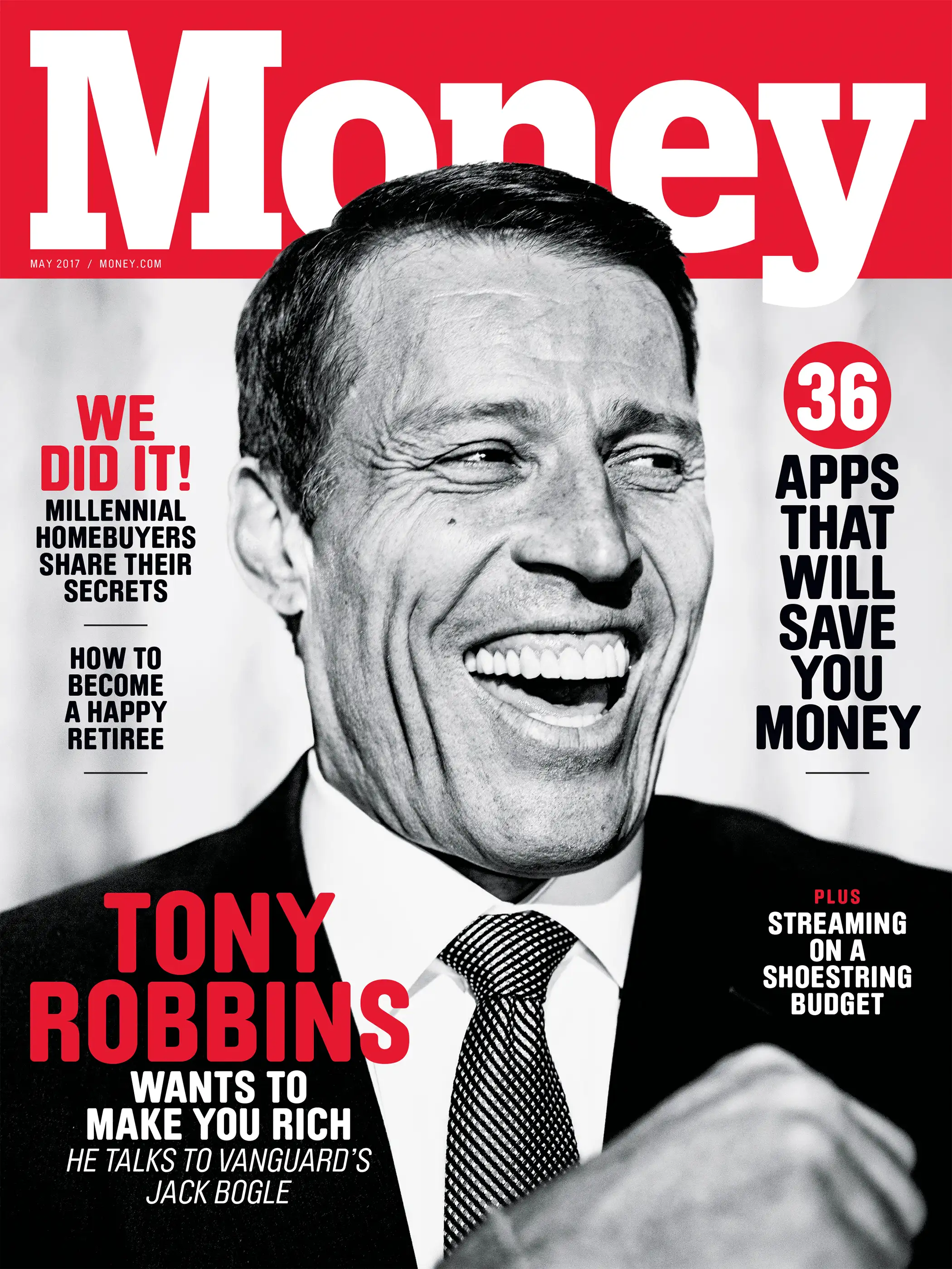

Tony Robbins: What I Learned From the World's Greatest Investors

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

It has been one of the more remarkable career arcs in business.

Tony Robbins came to fame in '90s infomercials, pitching 30-day programs with slogans like "personal power." Over the next two decades, through entrepreneurship and a message of self-transformation delivered with zeal, he won the ears of some of the most influential people in the world. He advised Bill Clinton during the impeachment scandal, has counseled hedge fund billionaire Paul Tudor Jones for years, and was dubbed "the CEO Whisperer" by Fortune for his work coaching executives.

Last year's Netflix documentary I Am Not Your Guru went behind the scenes of his popular seminar "Date With Destiny," a six-day event in which thousands of paying attendees hang on to his every word.

Now Robbins, 57, is bringing his brand of gut-level life and business strategies to the mainstream investor. His book Unshakeable draws on conversations he has had with some the best-known investors in the world. It aims to coach the masses that trying to outperform the market is, for the most part, a bad idea.

Better, he writes, to be average—invest in low-cost index funds, which give you exposure to the entire market, and keep investing through the market's inevitable spikes and corrections. And he cautions against letting fear or anxiety steer your decisions.

"You're not jarred by winter when you know it comes every year," Robbins likes to say, referencing the market's long-term pattern of boom and bust. (For the record, he says the bulk, but not all, of his own portfolio is in index funds.)

Robbins is also promoting showmethefees.com, an online tool offered by America's Best 401k (ABk), a company he has partnered with that designs and administers retirement plans. The site lets you see an estimate of the fees charged by your workplace retirement plan—expenses that Robbins says are usually way too high—vs. what ABk might charge.

Coaching others has certainly been good for Robbins' own fortunes: His net worth is reportedly half a billion dollars. And he has a financial interest in this latest endeavor. Robbins' son, Josh Jenkins-Robbins, serves as ABk's chief marketing officer. He and his son are also affiliated with Creative Planning, a registered investment adviser with $22 billion in assets mentioned frequently in Unshakeable. The book was cowritten by Creative Planning's president and owner, Peter Mallouk. Robbins is the firm's chief of investor psychology and a board member. He receives compensation from the company "based on increased business derived by Creative Planning from his services. Accordingly, Robbins has a financial incentive to refer investors to Creative Planning," according to a legal disclaimer. (Robbins says his proceeds from the book will go to the charity Feeding America.)

Along the way, Robbins has won the backing of one of the most respected figures in the financial services industry: Jack Bogle, the 87-year-old founder of the Vanguard Group and an early champion of index funds. Bogle calls Robbins a "voice for good"—perhaps one who can help spread the gospel of low-cost investing to an even wider audience than Bogle ever could.

It's a fascinating pairing: one an industry insider, the other a charismatic outsider who has worked his way in. What they share is an investment philosophy that may soon face a critical test at the next market downturn.

At Money's invitation, Robbins and Bogle recently sat down to talk about the book what it takes to be an investor in today's market. This transcript of their conversation has been edited for length and clarity. We began by asking how they met.

Jack Bogle:

I got a note from David Swensen—manager, as everybody knows, of the Yale endowment fund. And he said would I be willing to talk to Tony Robbins.

I'm a nice guy. David's a nice guy. So Tony and I got together. We allowed 15 minutes, maybe half an hour. But we were completely gripped by the conversation. It must have gone on for over an hour, and it's pretty clear from the way Tony's [first investing] book came out that I—I guess I was persuasive. [Laughs.]

Tony Robbins:

Actually, Jack, I came for a 45-minute interview, and it was 3½ hours!

One of the things you did was educate me to the realities of the market and the tyranny of fees. I did 50 interviews, but you were the one who said, "Tony, if you really want to help people, you gotta look at these 401(k) fee structures." Ninety million Americans have a 401(k) [or related accounts]. It's where most Americans have their money, and it's where most Americans are being taken advantage of.

And one of the challenges there, Jack, as you know, is that 80% of 401(k) plans are at small to medium-size businesses, and most of these plans are "pay to play." They don't even offer index funds. So that's one of the reasons I started doing research. We now have a place online, showmethefees.com, where people can put in their numbers and find out not only what the fees are, but what they cost [after] compounding.

Bogle:

Well, it's all about the cost. Investing is the one business in the world where you not only don't get what you pay for, but you get what you don't pay for. [Both laugh.]

Robbins:

That's awesome. I'll tell you something else you taught me—the metaphor of 1,000 gorillas flipping quarters. One flips 20 heads in a row and we all think, What a lucky gorilla. But when it's in the financial business we go, What a genius. [Laughs.]

You have a way of cutting through the bulls--t, Jack.

Bogle:

It's actually a lot like a lottery. I can't remember how much you touched on it in your book, but one of the most powerful ideas in investing is reversion to the mean. A fund does very well, then it does badly. A fund does very badly, then it tends to do well. Costs play a big role.

To the extent that a fund is doing badly because of its costs—[annual] expense ratios, sales loads, portfolio turnover rate—it's not going to revert to the mean. It can't do it. It's stuck in the bottom.

So it's reversion to the mean for the good guys, and a little reversion, but not nearly as strong, for the people who have not done a good job because of their high costs.

Robbins:

The other piece that relates to that is the average investor. When they're trying to figure out what [fund to invest in], maybe they go to Morningstar [and try to look up] five-star funds, not understanding reversion to the mean.

But it's just like you were talking about. If you look at the research, out of 428 five-star-rated funds, four are still five-stars 10 years later. People are buying at the peak. They're being sucked into doing the very opposite of what the greatest investors do.

Bogle:

In investing, you're better off learning from the experience of others than learning on your own [because] it's an expensive way to learn.

Robbins:

Well, that's why we both write the books we write. Tell me something: What would you tell me now? Because I'm talking to a lot of people right now, and there are a lot of people very fearful that the market's valuations are extremely high, and they're extremely concerned.

Bogle:

Well, let me first say that waiting until the weather clears in the stock market probably means you started waiting when World War II started. [Laughs.]

My next thought comes out of [your book]. The book is excellent—and I read it before I did the endorsement. But it had, to me, a little too optimistic cast looking at past returns and things of that nature. So in my introduction, I wrote this, and I'm very glad you kept it in:

"We live in an uncertain world and face not only the risks of the known unknowns but also the unknown unknowns—the ones that we don't know we don't know. Despite these risks, if we are to have any chance for meeting our long-term financial goals, invest we must."

Benjamin Lowy for Money

Benjamin Lowy for Money

And I would stick by that. This is the time to really emphasize risk. Valuations are clearly high, dividend yields are low, earnings growth will probably be less than the long term [average], which is around 5%. It could be as low as 4%, and inflation will take a little bit out of that now. So it's a time for some caution.

The index [fund] is not a panacea. It's participation in a risky business that eliminates the risk of individual stocks, eliminates the risk of picking managers, eliminates the risk of picking the hot sector of the day, and leaves only the risk [of] the stock market itself.

But that risk is not to be disregarded. It's always been high. It always will be.

Robbins:

By the way, [that sense of optimism] probably comes from Warren Buffett's "Don't bet against America" mentality. But we put in additional cautions throughout, so you know.

And I'll send you—last time I sent [the book] to you, you wanted, like, 80 to 100 copies. You want me to send you a bunch, to be able to hand out the new one as well?

Bogle:

Are you gonna do it free?

Robbins:

Course!

Bogle:

Why don't you send me 50 copies?

Robbins:

Okay. I'll send you 50. The man is always cost-conscious …

Bogle:

Live it or you don't live it, Tony. [Both laugh.]

Robbins:

You're right, brother. I understand. You know, I give Warren Buffett's argument based on the past and based on the fact that every bear market we've had has been followed by a bull. I show all those numbers.

But then I also look at what's happened in Japan. There is no guarantee in life. You just said, "It's not a panacea. It's participation." That mind-set is really, really, really helpful.

The overall concept is just helping people to understand that there's risk in whatever you do, and it's really about increasing the probabilities to your side. That's the essence of what the book is about.

Benjamin Lowy for Money

Benjamin Lowy for Money

Bogle:

But invest your money.

Robbins:

That's exactly right. Jack, what do you tell people right now who are on the sidelines? Especially younger millennials. Those are the ones I'm really focusing on right now, because they have such an opportunity if they just start to get in the game.

Even if they take some hits, they're young enough to see that [long-term] impact.

Bogle:

Well, I can tell you what I say to them, but you'll have to figure out what they actually do.

If you're not investing, now is the time to start. The best single thing that can happen to [young] investors who are accumulating money is a major and sustained market decline. Think about that. And that's not the best thing that can happen to somebody who already has their capital in.

There aren't any easy answers. We will eventually get to the place where the consumer—the investor consumer—understands what Tony and I are talking about here today and behaves accordingly. Regular investing, diversified investing, and above all, low-cost investing.

[Economist] Paul Samuelson wrote in his preface to my first book in 1993, saying that Bogle "has changed a basic industry in the optimal direction." He knew it before anybody else did.

Robbins:

Which one was your first book?

Bogle:

It was called Bogle on Mutual Funds: New Perspectives for the Intelligent Investor. And, boy, did that stand the test of time. Probably my best one, which is awful to say because that means I've gone downhill.

Don't put that in. [Both laugh.]