4 Smart Ways to Fund Your New Business

This story is part three of a five-part series on the best way to launch your own business.

Technology has made it much cheaper to start a business than it was just a few years ago. You can use inexpensive cloud-based software programs to manage tasks that once required people on the payroll. You can set up a website on your own. You can tackle credit card processing inexpensively on an iPad or a smartphone. And when you need project help, job-posting sites such as Upwork and Fiverr make finding contractors easy.

“What used to cost you $1 million or $2 million to start, will now cost you less than $100,000,” says Sanjeev Sardana, who advises many entrepreneurs as CEO of BluePointe Capital Management. Great, but a hundred grand is still serious seed money. Take these four steps to tackle that nut.

Save up to put skin in the game

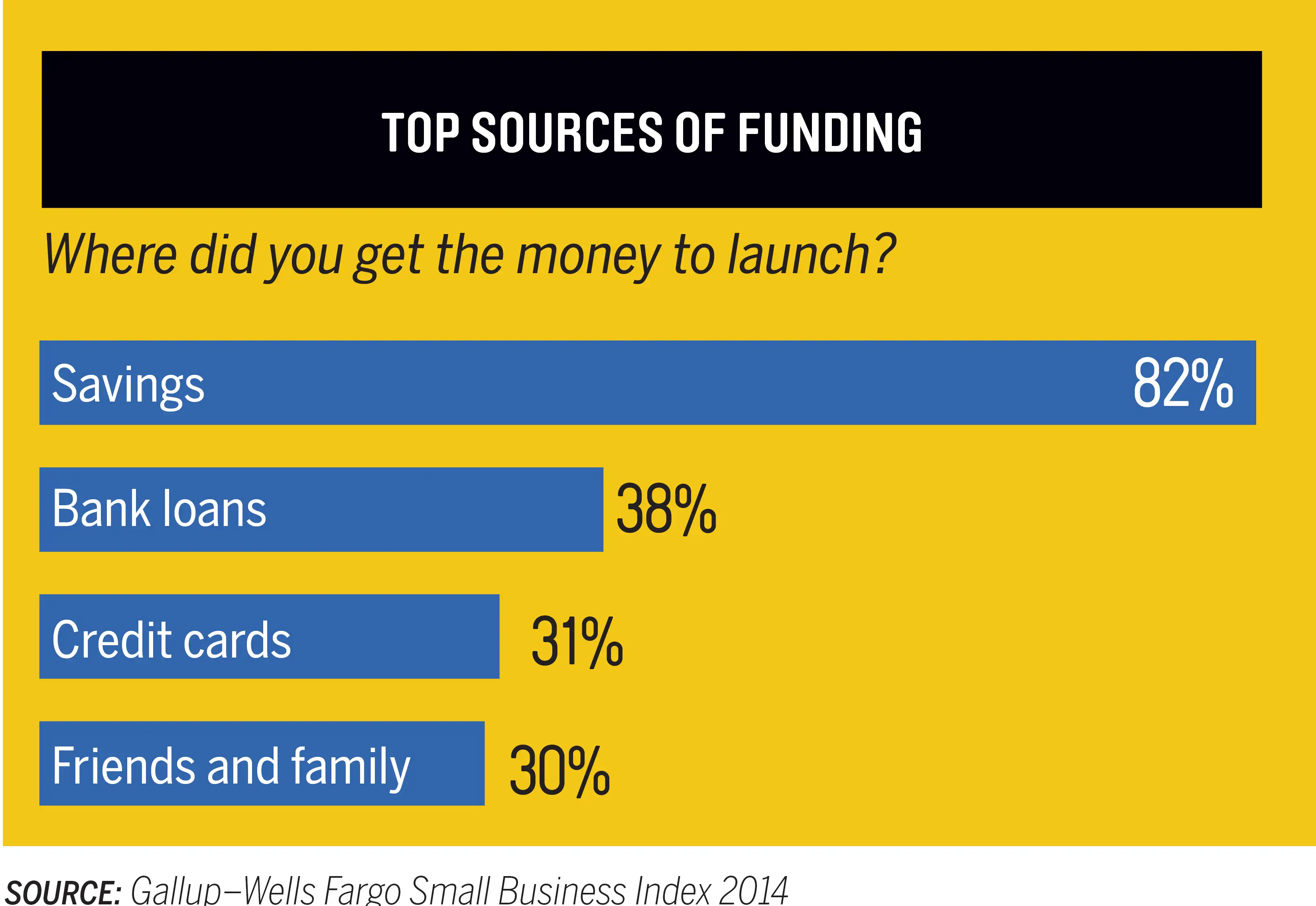

Don’t count on outside investors to bankroll your idea until you’ve built a track record. Self-funding is the most popular form of financing, so sock away as much as you can in advance. Barbara Roberts, an entrepreneur in residence at Columbia Business School and a co-author of The Owner’s Journey, says it is “virtually impossible” to find an investor until you’ve put in at least $250,000 of your own sweat equity, or rounded up that much cash from friends and family. Even on Shark Tank, she notes, “if you watch who gets the money, it’s typically someone who has some revenues or has lined up customers.”

Be realistic about crowd support

You can try pitching your idea on crowdfunding sites such as Kickstarter and Indiegogo; many inventors ask for donations to fund preorders of a product they want to create. But crowdfunding takes social media savvy. You generally need to have a decent-size presence—typically 6,000 or more followers—on social media to run a successful campaign, says Roberts. “If you’re talking about someone who ran social media for Pepsi or Coke, they could do this in their sleep,” she says. “If you’re talking about the CFO who doesn’t have a LinkedIn presence, then no.”

Know how much to save

It usually takes small-business owners 12 to 18 months to generate steady cash, so you need a cushion that will allow both your family and your business to get through that period, says Rohit Arora, CEO of Biz2Credit, an online matchmaker for small businesses and lenders. “You should have 18 months of dry powder to survive,” he says.

With no other income to live on, Sardana goes even further, recommending putting aside at least two to three years’ worth of living expenses so that financial stress doesn’t force you to close shop prematurely. And even if you have already lined up customers, take into account potential dry spells. Cut your revenue projections in half and double your expenses, says Arora. “Then you’ll see if you can survive,” he says.

Build in a buffer

What if you can’t come up with a couple hundred thousand dollars? Line up another source of income. If you need to quit a demanding corporate job to make time for your startup, that doesn’t mean you can’t take a part-time job or freelance consulting work to help pay the bills. Even renting a spare room on Airbnb can help.

Next in this series: How to Launch Your Dream Business Without Going Broke