Why You Should Be House Hunting for Foreclosures Right Now

- Selling An Upscale Home? You're in Luck. Sales Remain Strong.

- Where Are The Most Underwater Homes? These 13 Cities

- Swimming Pools: Valuable Home Upgrade or Just a Pain in the Wallet?

- The Cities Where Zombies (Foreclosures, That Is) Are Still Lurking

- Good Luck Getting a Mortgage on a Condo. Here's What You Need to Know

Last year, if you went shopping for a bargain foreclosed home, chances are you were thwarted by investors – some of them Wall Street-backed firms with massive bank accounts – thrusting wads of cash at every decent under-$200,000 home in sight.

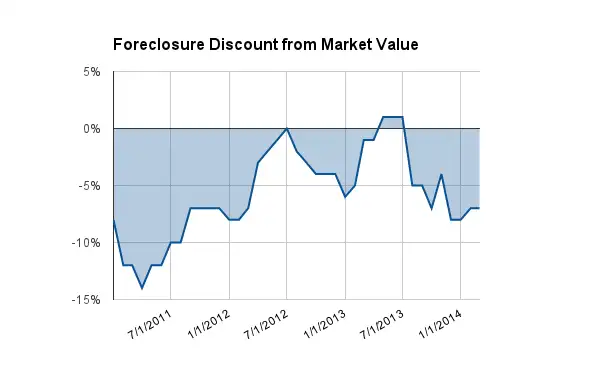

And, in fact, investors were buying up so many homes, so fast, they pushed prices of foreclosures past what they were worth, according to new data from RealtyTrac. For three months last summer, the average foreclosure sold at a premium to its market value.

Well, looks like it’s safe to go shopping again. As investors have pulled back on their buying, discounts on bank-owned homes have drifted up again this year to 7% in March, RealtyTrac says.

That’s good news for buyers willing to put in the effort on some renovations in exchange for a deal. After all, that’s the whole point of buying a foreclosure. Sure, it often needs work – maybe even a lot of work if it’s one of those “anger management” homes exited by a bank-hating owner – but if the subsequent gain in home value exceeds the cost of improvements you’ve just set yourself up for a nice profit whenever you sell.

Back in 2011, those discounts got as high as 15% (this is for bank-owned property listed on the open market, not foreclosures sold at courthouse auctions – those discounts are much steeper). Such values lured investors onto the scene seeking to tap increased rental demand.

Over the last year, institutional investors (defined generally as investors buying 10 or more properties) have cut back, though not in all markets. They’ve generally shifted out of boom-bust hotspots like Phoenix and southern California into more stable areas in the Midwest and South.

So too, the discounts vary by city. The best deals tend to be found in places where the number of foreclosures remain relatively high and economies are struggling—Ohio, for example, and Rochester, N.Y. and Scranton, Pa. But they're pretty juicy in some large metropolitan areas too, like 11% in Chicago, according to RealtyTrac data.

| City | Discount |

|---|---|

| New York City | 10% |

| Los Angeles | 2% |

| Chicago | 11% |

| Philadelphia | 10% |

| Houston | 21% |

| Washington, D.C. | 2% |

| Miami/Ft. Lauderdale | 5% |

| Atlanta | 9% |

| San Francisco/Oakland | 2% |

| Detroit | 18% |

| Riverside, Calif. | 4% |

| Phoenix | 5% |

| Seattle | 8% |

| Minneapolis | 7% |

| San Diego | 3% |

| St. Louis | 21% |

The trend toward bigger discounts, notes Chris Clothier, co-owner of Memphis Invest, may reflect the quality of the foreclosures now on the market: The more renovation they require, the higher discount they need to offer to attract buyers.

Plus, he says, more banks are making repairs themselves before putting them on the market. Such nicer properties might not even be listed officially as foreclosures and therefore wouldn’t show up in the numbers, Clothier says. “They’d rather fix them up and sell them at a higher price than take the steep discount,” he says. “You might be buying a foreclosure and you don’t know it.”

It’s certainly true that the number of foreclosures on the market has declined significantly, to 9.2% of sales in April, according to RealtyTrac, though it really does depend on the area. Take California, says vice president Daren Blomquist. Foreclosures are way down in hot markets like San Diego and Los Angeles, but in inland California cities (Modesto and Stockton) the percentage of sales that are bank-owned top 20%.

“Distressed property may be more rare, but you’re also buying in a housing market that’s improving and growing,” so it’s not as risky, Blomquist says. “Arguably the best time to buy a distressed property is in a market more like the one we’re entering right now.”

More from Money: When Wall Street Becomes a Landlord