5 New Ways Your 401(k) Will Make You Richer by Retirement

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Over the past 10 years, a quiet revolution has been transforming the 401(k) landscape. As a result, you're probably saving more consistently and investing in a smarter mix of stocks and bonds, maybe without even knowing it. Employers are increasingly automating financial moves that you might otherwise drag your feet on—who really remembers to boost his contribution percentage every year? And they are offering optional counseling and a variety of nudges—such as retirement readiness scores and prompts to use online calculators—to help you avoid coming up short in later life.

The new benefits are not simply an altruistic gesture from your boss, of course. Some 52% of workers feel financial stress, and 20% of those earning $100,000 or more have trouble meeting household expenses, according to a 2016 PwC survey. That can adversely impact the bottom line: Financial pressure is causing some 60% of employees to have difficulty focusing on work, according to the International Foundation of Employee Benefit Plans, and it is also associated with higher absenteeism.

Meanwhile, workplace savings plans like 401(k)s are playing an even larger role in Americans' retirement preparations as old-fashioned pension plans, which require no action on your part, have become rare outside the public sector. Over the 35 years through 2013, the percentage of private-industry workers covered by a 401(k) and not a pension rose from 7% to 33%, according to the Employee Benefit Research Institute. The percentage who had a pension plan, either with or without a 401(k), fell from 38% to 13%. That makes it all the more important for you to make the right moves with your 401(k).

Below, you'll find strategies to take maximum advantage of five key innovations and new services for 401(k) savers, along with advice about when you should override automatic settings to make even better moves for you. The payoff can be tens of thousands more dollars in your accounts to help you live the retirement life you want.

THE INNOVATION: Embracing Autopilot

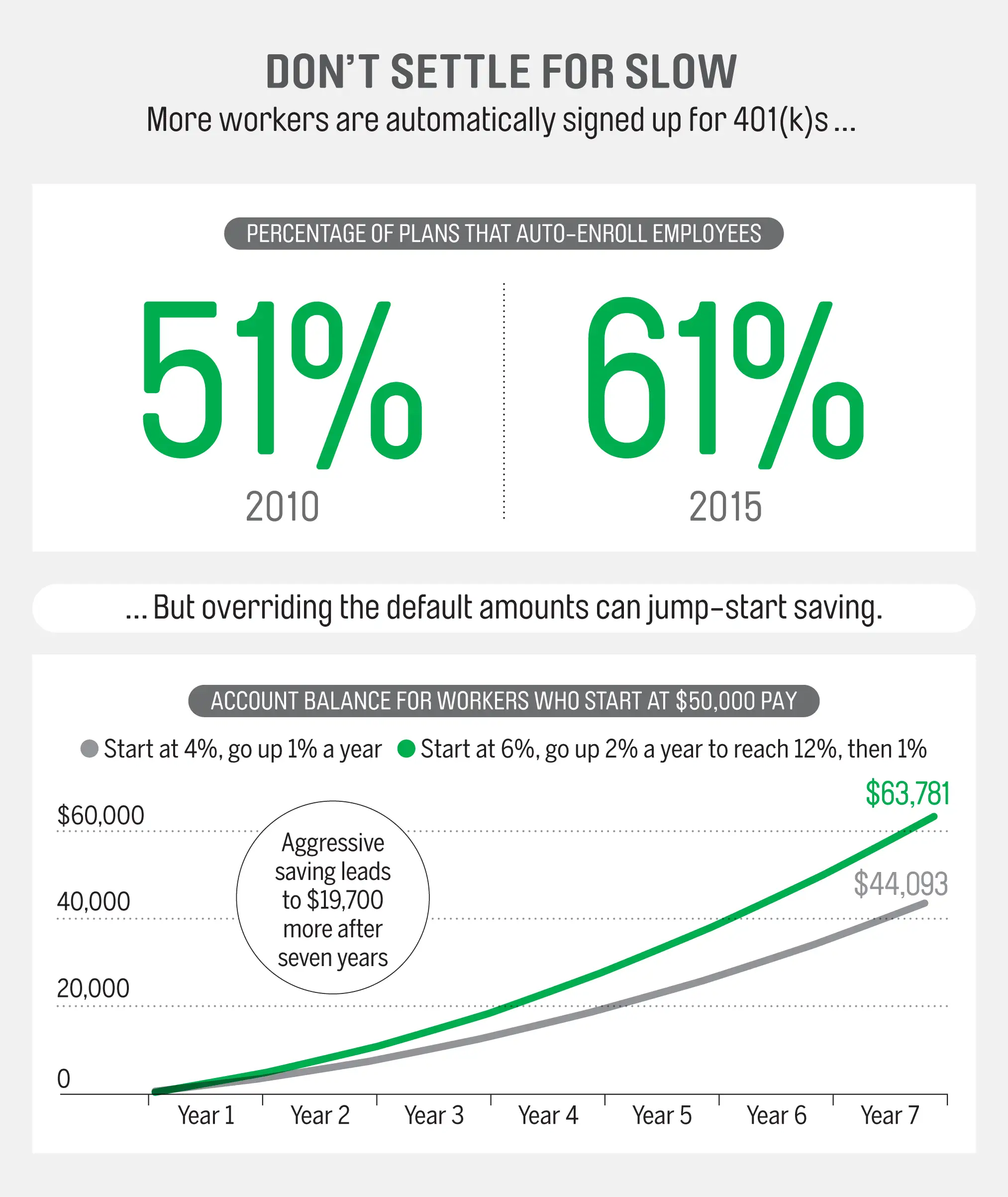

Increasingly, the most critical 401(k) decisions—including enrollment, your initial contribution amount, and future increases in saving—require little or no input from you. Some 61% of 401(k)s auto-enrolled workers in 2015, up from 51% in 2010, according to benefits consultant Callan Associates. So unless you opt out, you will be defaulted into the plan, most commonly with 3% of your pay being funneled from each paycheck, Vanguard data show.

You are typically steered to a diversified investment portfolio based on the year you might retire. And the push doesn't end there: Among plans with automatic enrollment, some 81% will also increase your contributions over time, according to Callan—typically by 1% of your pay a year.

Together, these automatic features are turning 401(k)s into something a bit more like a traditional pension, says Lauren Valente, a principal at Vanguard. Except for the guaranteed retirement income, of course.

What's the thinking here? Decades of research in behavioral finance have found that 401(k) investors fare better when employers free them from decisions they aren't ready or eager to make, including giving up dollars now to have more for a future goal. Problem is, many employers play it too conservatively in setting the initial contribution rate and the speed at which contributions escalate.

Your Best Moves

- Claim all your free money. Auto-enrollment is great to get you in the plan right away, but it can also set you up to leave dollars on the table. Even if you are just starting out in your career, aim to override the default and save enough to get a full matching contribution from your employer, which might be 50¢ for each dollar up to 6% of pay. If you earn $50,000, getting a 3% match rather than 1.5% is another $750 a year.

- Turbocharge those annual increases. Many financial pros say you should aim to save 15% of your pay a year, including the employer match. Even if you need to start at a much lower level, make a point to boost what you set aside each year by more than the typical default of 1% of pay. "You need to get to the right savings level as quickly as you can, to avoid losing out on compound growth," says Rob Oliver, a financial planner in Ann Arbor. As shown in the graphic below, a more aggressive schedule could add almost $20,000 to your nest egg in just the first seven years. Boosting your saving by 2% or 3% of pay a year might sound like a lot, but "if you never see the money, you probably won't miss it," says Eileen Freiburger, a financial planner in El Segundo, Calif. If your plan can't schedule those increases automatically, do it yourself, with a phone call or click, whenever you get a raise or celebrate another birthday.

- Don't stop when auto-escalation stops. Your plan is likely to stop increasing your savings rate once you reach 10% of pay, but don't take that as a message from on high that that is enough for you. Higher-income workers may need to save as much as 20% (including a match) to maintain their standard of living in retirement. So make sure to manually raise your savings rate until you hit the maximum dollar amount you can sock away each year, which is $18,000 for most people in 2017. Starting the year you turn 50, you can add another $6,000 annually, yet only 16% of eligible savers make such contributions, Vanguard says.

THE INNOVATION: Targeting the Right Investment Mix

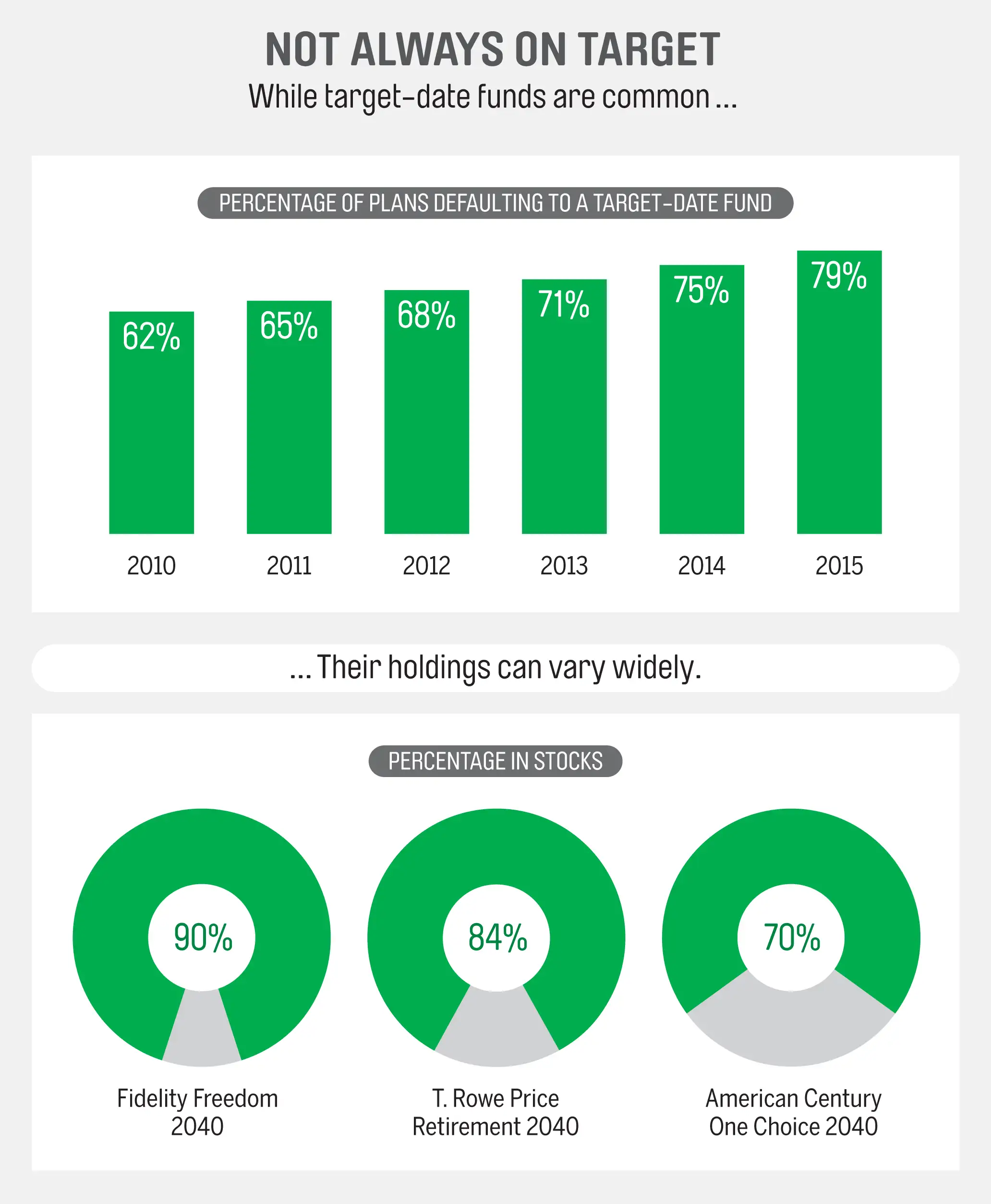

These days your primary investment decision is not what to invest in, but whether to opt out of what the plan puts you in. Some 79% of employers now start you out in a target-date fund as a default investment, up from 62% in 2010, according to Vanguard. A target-date fund gives you a preset mix of stock and bond holdings that shifts to become more conservative as you approach retirement.

New employees aren't the only ones being steered in the target-fund direction. More employers are "reenrolling" existing employees, which means shifting your account into the default investments unless you say no. Some 20% of 401(k)s had done a reenrollment at some point as of 2015, up from 12% as of 2013, according to Callan. It is most common when a plan changes its fund lineup, says Lori Lucas, practice leader at Callan.

Research shows that, on average, investors in target-date funds do as well as or better than DIY investors, typically with less risk. Over the five years through 2015, investors who held a single target fund in a 401(k) at Vanguard earned an average of 7.6% a year vs. 7.2% for people calling the shots themselves. Some DIYers did far better than the average, but others did far worse.

Many target funds have become better diversified in recent years, with the addition of emerging-market stocks, foreign bonds, and other asset classes. Even better, fees have come down—the cost of the typical target-date fund is 0.55% vs. 0.67% in 2010, Morningstar reports. And you are increasingly likely to be offered an ultra-low-cost index version.

Still, you need to be aware that some target funds have very different asset allocations than do others geared to workers of the same age, says Andrew Sloan, a financial planner in Louisville. And a fund's perfectly reasonable portfolio allocation might not be right for you based on your personal risk tolerance and other holdings.

Your Best Moves

- Make it the main ingredient. Target funds are meant to be an all-in-one, stand-alone investment. But only one out of four investors who have a target fund use it for 90% or more of their 401(k) portfolio, according to a recent study by Financial Engines, a 401(k) advice provider. On average, investors who combine target funds with other funds earn annual returns about two percentage points lower than those solely in the age-appropriate target-date funds, says Wei Hu, a vice president at Financial Engines. So either decide to go big on the target fund or just skip it entirely.

- Dig a little deeper. You won't go completely wrong with a target-date fund. But particularly as your nest egg grows and retirement approaches, you should look beyond the year in a fund's name to understand the amount of risk it takes and decide if it fits your goals. The biggest source of both risk and return is its commitment to stocks, and, as seen in the graphic below, some target funds hold a lot more stocks than others. If you want to play it safer, switch to a target fund geared to workers who are older than you. You might ditch the year-2030 fund for the one designed for people thinking of retiring in 2025 or even 2020. Conversely, to ramp up risk, opt for a fund intended for younger workers.

- Look at your 401(k) as one slice of the pie. You've also got to look beyond your workplace plan to decide if a target fund's mix of stocks and bonds is right for you. For instance, the default fund in your 401(k) may be too aggressive for you if you own a lot of stocks and other risky holdings outside the plan. And if you are married, you and your spouse should be looking at your assets together. A financial advisor or a tool such as Vanguard's Investor Questionnaire can help you decide on the right level of stock exposure for you. While target funds are handy for many investors, it's also possible you and your spouse will find it easier to tweak your overall asset mix by using individual stock and bond funds in your two plans, says Sloan.

- Bypass a target-date fund if fees are high. If your plan offers only high-cost target-date funds—with fees of, say, 1% or more—see if you have other options. "Perhaps your plan has a lower-cost S&P 500 index fund or an inexpensive bond fund," says Freiburger. Check the funds' expenses on your plan's website or the annual expense disclosures your 401(k) provides.

THE INNOVATION: Offering Personalized Investing Assistance

Not sure about the right mix of funds for you or how much you need to save? Your 401(k) probably offers a bunch of online tools to help. And that isn't all. Some 36% of plans offer one-on-one financial advisory services, up from 28% in 2013, according to Callan. That is most commonly a free one-time phone consultation with the financial company that administers the plan.

About 9% of plans offer more extensive service, often for a fee, Callan says. That is typically with a company, such as EY or Goldman Sachs's Ayco unit, that is independent of your 401(k) provider. A subsidy from your employer could result in a lower cost to you than the 1% of assets a year that an outside advisor might charge.

Another type of customized help is so-called managed accounts, in which you pay an investing pro to oversee the investments in your 401(k) based on your personal needs and goals. These accounts are offered by a similar 36% of plans, according to Callan. The advice is often provided by an independent company, such as Financial Engines or Morningstar. Fidelity, a big player in 401(k)s, offers this service as well through a separate division. You will likely pay a fee, such as 0.3% to 0.7% of assets a year; that would be $300 to $700 on a $100,000 account.

Your Best Moves

- Free advice? Sure! If you are offered a free sit-down or phone call with a qualified pro, go for it. "Getting a second opinion is always useful, and there's little downside," says Freiburger. Make efficient use of the session by gathering your financial data in advance and thinking about your top priorities.

- Do your part. About half the people who sign up for managed accounts with Financial Engines don't provide information about outside investments and their goals to personalize the service they get. If you are going to pay for added attention, give the advisory firm the information it requests to design the best portfolio it can for you.

- Consider getting extra help if you are within 10 years of retirement. Besides any personalized advice services, your plan probably offers a host of online resources. For instance, some two-thirds of plans offer tools that will help you project your retirement income, an Aon Hewitt survey found. But if you are closing in on retirement, you may benefit from a still more detailed analysis and consultation with a financial planner you hire on your own. For instance, you and your spouse might want help deciding on a possible relocation and a tax-savvy strategy for pulling money out of retirement accounts. (Resources to find an advisor include napfa.org and garrettplanningnetwork.com.)

THE INNOVATION: Helping Heal Your Financial Ills

For many workers, scrambling to cover immediate expenses, let alone periodic emergencies, gets in the way of saving for retirement. Among millennial workers, for instance, some 42% have student loans, PwC found, and 79% of them say this debt has a moderate or significant impact on their ability to meet their financial goals. That's a key reason about 55% of companies offer some assistance to improve your finances, such as debt management and budgeting tips, according to Aon Hewitt.

Some employers are bringing in third-party companies that specialize in financial wellness services, such as Financial Finesse, PwC, and Morningstar's HelloWallet, typically at no fee to employees. The services can range from online budgeting tools to on-site workshops on reducing debt to individual coaching over the phone from certified financial planners or other pros.

Are financial wellness programs effective? Preliminary data are limited but promising, the Consumer Financial Protection Bureau has found.

Your Best Moves

- Tackle a single challenge first. There's little downside to trying out your employer's financial wellness services. You might focus on a small achievable goal such as starting an emergency fund or figuring out how much house you can afford. "For many people, achieving one goal can encourage them to keep up the progress on other issues," says Kent Allison, a partner at PwC.

- Working regularly with a money coach can make a big difference. If your issues are complex, see if your company offers the option of continuing one-on-one assistance from a pro. Most employers foot the bill, but in some cases you may have to pay an additional amount, perhaps $20 a month. Scheduled check-ins and regular encouragement can be a big help. Before signing up, make sure the company providing the guidance isn't selling a service or product.

THE INNOVATION: Making Retirement Income Easier

If you're a boomer approaching retirement age, you are probably starting to think about how you will draw money out of savings to cover expenses after your leave the workforce. Some companies are making it easier for retirees to tap their 401(k)s, such as by letting them sign up for regular monthly checks.

That isn't just to help you. You also have the option to roll money from your workplace plan into an IRA. Some employers are recognizing that a flood of IRA rollovers could shrink the assets in their 401(k) plans, leading fees to go up and hurting younger workers, says Rob Austin, Aon Hewitt's director of retirement research. So they are looking for ways to make it more comfortable for retirees to stay put.

To help retirees make their money last, in 2014 the Obama administration issued a rule intended to nudge 401(k) plans to offer annuities that would provide lifetime income. But so far, employers, who worry about the legal risk if an insurer fails, have shown little interest. Buying an income annuity is generally an irreversible decision; it's a possibility you might want to discuss if you hire a financial advisor.

Your Best Moves

- Don't rush to leave your 401(k). If you work for a large company, you may be paying lower investment fees in your workplace plan than you would in an IRA. If so, look for ways to keep the bulk of your account balance there, even as you start to withdraw dollars. Some 45% of plans let you set up a series of automatic payments, such as monthly checks throughout your retirement, Aon Hewitt reports. If your plan requires you to separately request each withdrawal in a cumbersome process, you might transfer a single large sum to an IRA each year and then withdraw from that.

- Scrutinize rollover recommendations. Rolling your money to an IRA could be a good deal for a financial advisor. Make sure you are getting what's best for you: That's probably low-cost index funds, coupled with tax planning advice from an advisor who isn't swayed by commissions, says fee-only advisor Sloan. Given all the help you received from your 401(k) during your working career, you don't want to blow it just as you reach retirement.