36 Apps That Will Save You Money

- Average Car Insurance Prices Expected to Hit $2,500 This Year

- Olympians Can't Pay Their Bills. Celebrities and Crowdfunding Are Coming to the Rescue

- How Much Is an Olympic Gold Medal Worth? Less Than You'd Think

- Credit Scores Fall and Bankruptcies Climb in States With Legal Sports Gambling

- 8 Things People Have Stopped Buying (and Why)

- What the Democrats Winning Georgia Means for Your Wallet

- Joe Biden Is the President-Elect. Here's What It Means for Your Wallet

- H&R Block Wants to Put Your Tax Refund on an Amazon Gift Card. Here's Why That's a Terrible Idea

- MacKenzie Bezos’s $36 Billion Divorce Settlement Makes Her the Fourth-Richest Woman in the World

- The Ultimate Guide to Doing Your Taxes in 2019: What Changed, How to Save and More

- 1 Million Public Service Workers Have Now Had Their Student Loans Forgiven

- As Student Loan 'On-Ramp' Ends, Missed Payments Will Once Again Hurt Your Credit

- How Low Will Interest Rates Go? Experts Predict the Fed's Upcoming Cut

- How to Pay Off Student Loans Fast

- Here's the No. 1 Barrier Blocking Parents From Saving More Money for College

- 5 Financial New Year's Resolutions You Can Actually Stick To

- 5 Moves to Make Now to Lower Your Tax Bill

- Think Your Commute Sucks? Here's Which Cities Really Have It the Worst

- Online Retailers Now Let You Pay in Installments. Proceed With Caution

- This Under-the-Radar Account Can Help You Save for Medical Expenses in Retirement

- 5 Ways Trump's New Budget Plan Could Fail

- The Richest Person at Every Age

- Trump's Budget Eliminates These 19 Federal Agencies. Here's What They Do — and Cost

- Donald Trump's Budget Plan Would Kill a $258 Million Banking Program for the Poor. Here's What it Does.

- The U.S. Runs Its Own Airline For Deportations. Here's How Much It Costs Taxpayers

What's the best way to put your phone to work for you? A team of Money reporters checked out dozens of apps (and websites in places where apps were few) to find 36 top picks across seven areas of your financial life: travel, tracking your money, your home, retirement planning, shopping, college, and investing.

Whatever your circumstances, there’s something here that can make your life easier and help you get more for your money.

Tools are free unless a price is indicated.

Rome2Rio

Rome2rio takes the guesswork out of planning your transportation from city to city. Plug in your origin and destination, and it lays out the choices—plane, train, bus, and car—along with the approximate time each route will take. Use it when traveling around Europe or when weighing Amtrak vs. a flight from, say, Boston to New York. The app factors in the total time it will take door-to-door using each type of transit.

SkipLagged

This app is similar to Kayak and Google Flights for finding airfare deals between specified cities. But SkipLagged can also help you save with a “hidden city” option—a one-way ticket from City A to City B to City C when the stopover is really your final destination. By ditching the second leg of the trip, you may save money and time vs. other tickets from City A to City B. Note that travelers looking for a roundtrip option will have to buy two one-way tickets to take advantage of these hidden-city fares.

Mobile Passport

Before you next head overseas, download this app authorized by the U.S. government. It can get you through Customs faster on your return. You plug in basic personal information and your passport data, along with a selfie, ahead of time. When you arrive back in the U.S. at one of the 21 participating airports (they include most of the major hubs), the app asks a few questions about your trip. It then lets you jump into a dedicated Mobile Passport line.

HERE WeGo

With this app you can download maps of the cities you’re planning to visit and then use the offline mode to view them. That can save on phone charges overseas. And closer to home, the app’s offline version of the New York City subway map makes it easy to double-check your route even when you’re underground. Offline maps are available for 1,300 cities across 110 countries. They take a while to download, so make sure you allow time to get them set up before you take off.

Journy

$15 per day of travel

If planning vacation activities feels overwhelming, Journy can help map out your days and make reservations in more than 60 destinations. You specify your age, types of activities, and a price range. The app taps a network that includes chefs, travel writers, and photographers to help craft an itinerary from breakfast through evening entertainment. You can work with a member of Journy’s concierge team to tweak that further. You get maps and directions, as well as reservation notifications, via the app.

- Download the app for iPhone

Google Translate

There are several translation tools on the market, but Google Translate’s features are still the best among free apps. You can write or even speak words and phrases that the app then translates into more than 100 languages. It even works offline (so you don’t rack up data charges) for more than 52 languages. Bonus: You can take photos with your phone’s camera to translate signs and menu options (although this works best with simple typefaces—it struggles with ornate script).

Level Money

Fight the temptation to overspend with Level Money, which shows you exactly how much you can responsibly spend on a daily, weekly, and monthly basis. It starts with your actual bank balances and subtracts essentials like rent and utilities as well as planned saving. What’s left is your “spendable balance.” You can set alerts for when you have, say, only 25% of that balance left. The app doesn’t have access to your dollars; you’ll have to manually roll the extra money that you accumulate over into savings.

Digit

Updated April 11, 2017: Now $2.99 a month after a free 100-day trial

This app makes saving effortless. It deducts money from your checking account, typically between $10 and $30 two or three times a week, setting aside only what it determines you can spare based on your spending habits. The money goes into a bank account from which you can withdraw funds at any time. Daily texts tell you your current checking balance, and you can text Digit to see your most recent debits. You can also instruct the app to become more or less aggressive with saving if you want.

- Download the app for iPhone

Qapital

Like Digit, this app makes saving an easy, painless task, but Qapital gives you control over how much and how often you save by having you set rules. Keep it traditional by having Qapital transfer a set sum each week from your checking account to a bank account it sets up for you. Or use it like a change jar by telling it to round up all purchases to the next dollar and set the difference aside. Or craft a fun rule of your own, like transferring $5 every time you post to Instagram or buy a cup of coffee.

Mint

The classic budgeting app, Mint allows you to see exactly where your money goes when you link your banking and credit card accounts to it. Track your spending on everything from housing to groceries to coffee-shop pick-me-ups in a multicolored pie chart. The app will suggest a budget based on the average amounts you spend. You can set limits for certain expenses and receive a warning when you’re approaching the max. Mint will also alert you when bill payments are due or your bank balance dips.

Prosper Daily

Spotting fraudulent or erroneous charges on your credit card accounts can be difficult. When you link your accounts to this app, formerly called BillGuard, it flags suspicious or duplicate charges for you to take a closer look. It also notifies you when there has been a data breach at a business you shopped at in the past.

Wallaby

Maximizing your credit card rewards feels almost like a job in itself. This app does the work for you by telling you which card to use at different businesses to earn the most bang on the transaction. For online purchases, download the Wallaby browser extension for the same service. The app also keeps track of how much of your credit limit you have used.

Houzz

Looking to redecorate? Rather than sift through piles of magazines and books for creative inspiration, check out Houzz to search millions of photos from product manufacturers and designers. You click on a photo to see a product’s cost, and you may be able to purchase it directly through the app. Plus, you can store your best ideas in your Ideabook so you don’t lose track of that perfect table or throw rug.

Dwellr

This resource from the U.S. Census Bureau can help you check out neighborhoods you are considering for a move. It uses the American Community Survey, an ongoing demographic study conducted by the bureau that uses 40 factors, such as median home price, total population, and the age and education of residents, to profile towns and neighborhoods. Tap the compass icon to get a reading on your current location. To start, the app asks you to answer 11 questions, and it then suggests your top places to live.

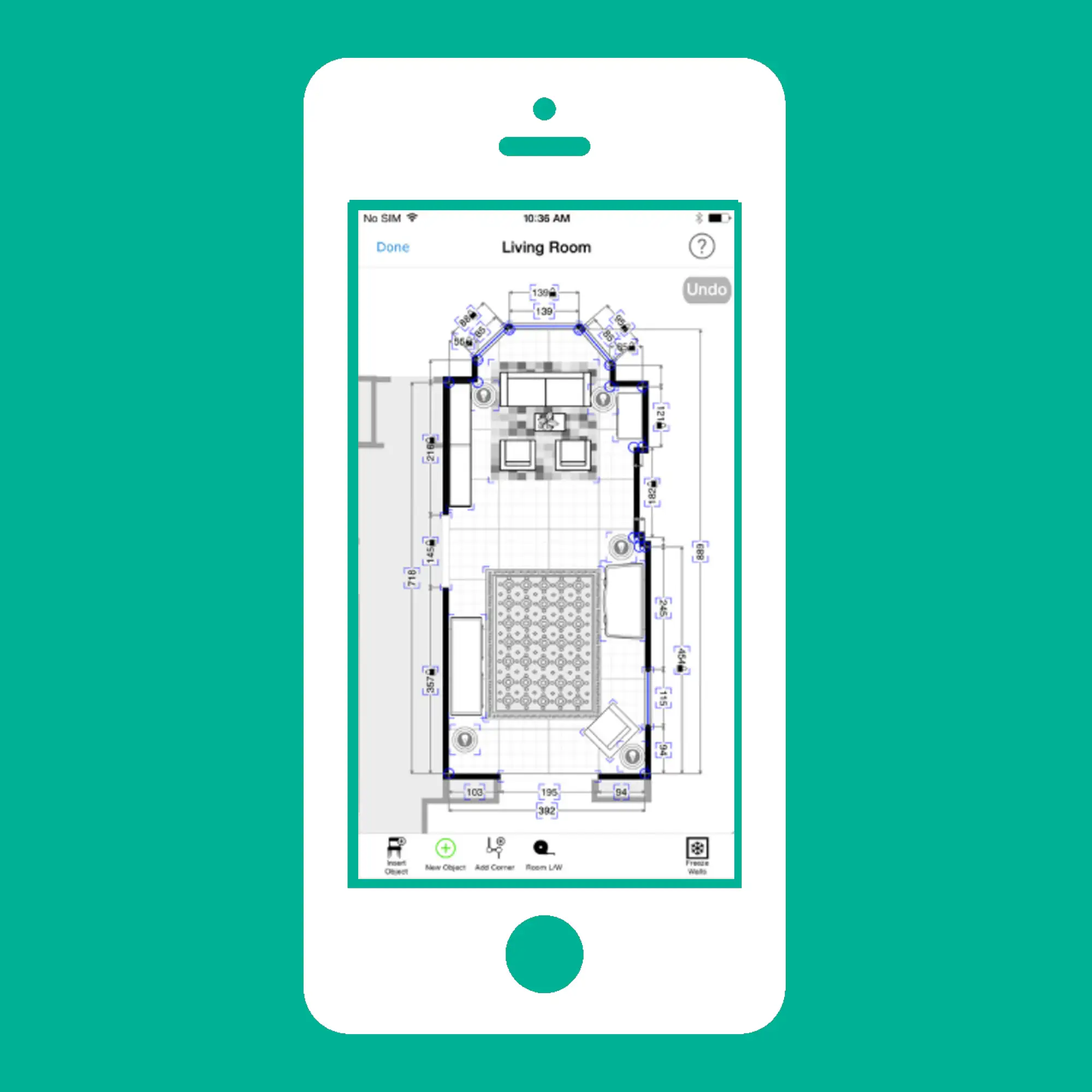

MagicPlan

From free to $9.99 a month

This app can help you figure out if the furniture you are considering is the right size for your room. With MagicPlan, you create a floor plan of a room by taking pictures with your phone. You can then add the dimensions of, say, a couch and chairs, either manually or by photographing them, to see how they would fit. The free version allows you to create a basic room plan and play around with what goes where. If you want to export the plan in a PDF, you pay $2.99 a plan.

HomeZada

From free to $5.95 a month

You probably know you should have an inventory of your possessions in case of a fire or other loss. The free version of this app makes it easy to check that off your to-do list: You upload photos of your possessions and add information on their value. You can also store warranties and other documentation. If you’re doing a big renovation, like remodeling the kitchen, spend $5.95 a month and the app helps you keep track of all your tasks and stay within budget.

Zillow Real Estate

The much-used Zillow is a comprehensive resource to find your first home, upgrade, or keep hope alive for your dream house. See the site’s Zestimate of a home’s worth, check out the listing history, and view photos and, in some cases, a video tour. Zillow has the largest database of homes on the market, including those for sale by owners, according to business consultant Cultural Outreach Solutions. Other apps, such as Redfin, may have more up-to-date listings.

NerdWallet Retirement Calculator

Many retirement calculators generate a big accumulation goal—$2 million, say—which can be intimidating and difficult to relate to. This NerdWallet tool, by contrast, looks at your retirement preparedness in terms of monthly income and spending. On the basis of just five data points—your age, desired retirement age, income, savings to date, and savings rate—it might say you’ll need $6,000 a month to live on in later life and you’re currently on track to have $4,000. It gives you suggestions to catch up. The simple design can quickly engage young people and get them thinking about saving for the future, but workers approaching retirement need a more detailed approach.

T. Rowe Price Retirement Income Calculator

This detailed planning tool asks for information including your current income, savings, and asset allocation, and from them it projects your various sources of retirement income, from investments to Social Security. You can incorporate a spouse’s information as well. The calculator runs Monte Carlo simulations, a tool frequently used by financial planners, to gauge the probability of your savings supporting your desired lifestyle in various financial market conditions. If you’re coming up short, you can see how changes such as delaying retirement and increasing your savings rate will help.

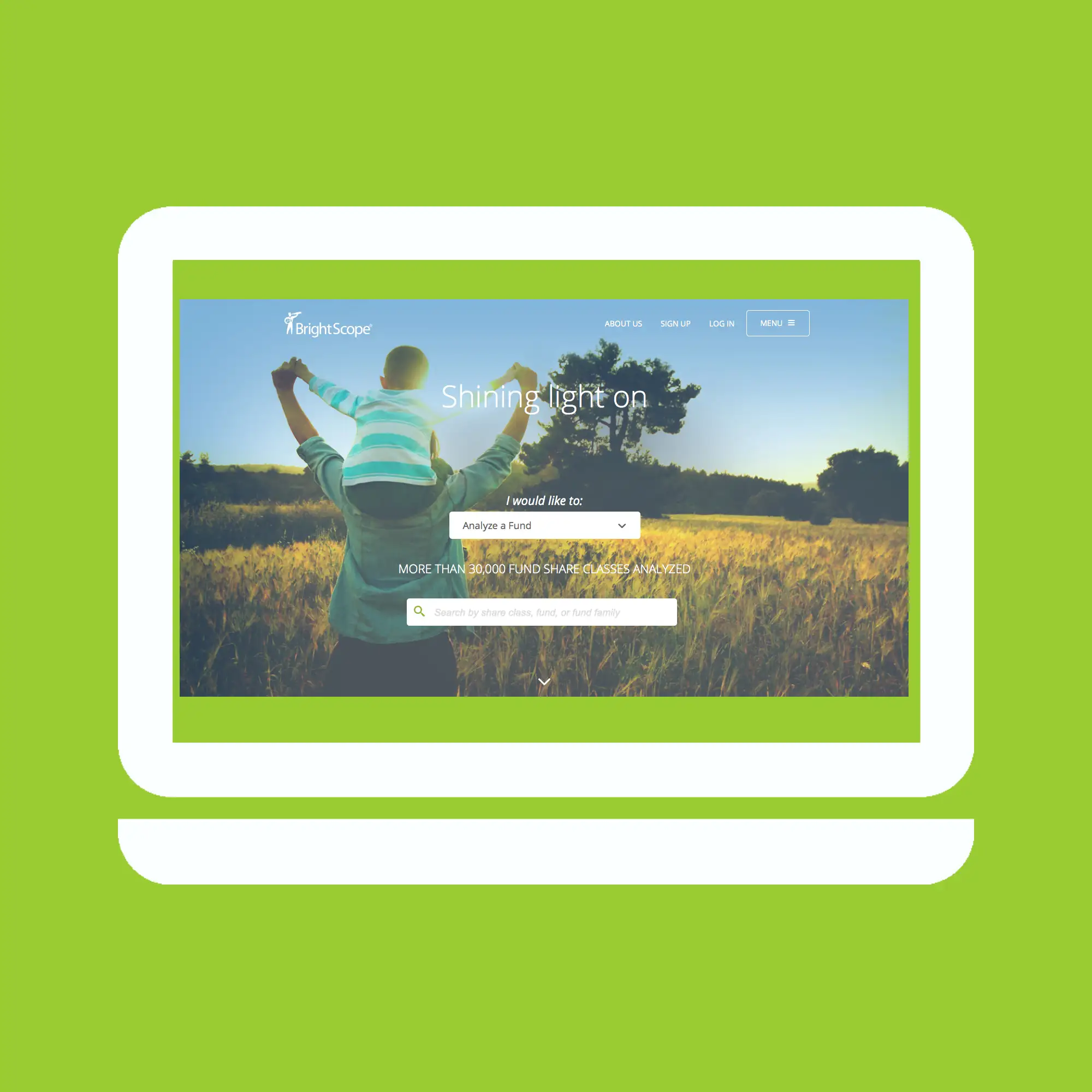

BrightScope 401(k) Plan Ratings

Wondering how a prospective employer’s 401(k) stacks up? This website uses details gleaned from plans’ annual regulatory filings to grade nearly 50,000 401(k) and 403(b) plans against peers. It looks at factors including expenses, investment options, and the employer’s generosity with matching contributions. Among the top corporate retirement plans based on 2015 data: Delta’s plan for its pilots, and those at ConocoPhillips and Amgen. Note that you’ll see few details on the individual 401(k) plans, and the data that BrightScope pulls from filings may be out of date. So also ask the company itself about the match and investment options.

Blue Zones

Although there are a number of life expectancy calculators on the web, this site’s True Vitality Test is one of the most thought provoking. Blue Zones is a project of Dan Buettner, a National Geographic Society fellow who traveled the world to study the habits of people with the longest life expectancies. This online tool asks a series of detailed questions—how many servings of unprocessed grains you ate in the past week and how many religious services you attended, for instance—to give you a more nuanced sense of your life expectancy based on your age, gender, and lifestyle. (Be honest.) Note: You have to register to see your results.

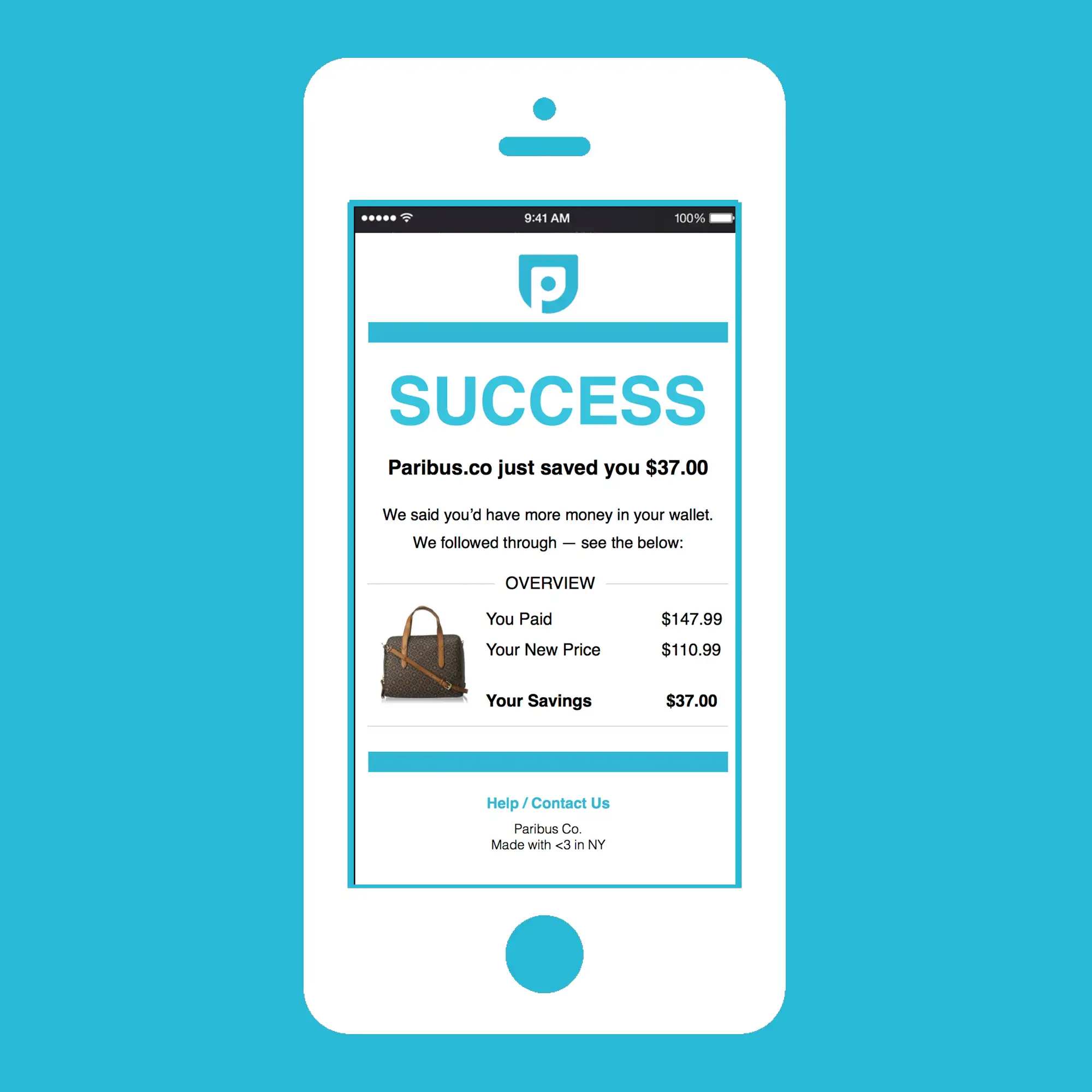

Paribus

Many stores offer refunds if the price of an item drops soon after you purchase it. But no one wants to keep shopping around after buying something, so many potential refunds go unredeemed. Enter Paribus, which not only tracks items you have purchased online but automatically requests refunds if the price drops. Customers don’t pay for the service, but Paribus takes a 25% cut of the refunds it retrieves.

- Download the app for iPhone

Flipp

Far fewer people get the Sunday papers these days. But all the ads, sales, coupons, and other special offers from the Sunday circulars can be browsed with Flipp. The app covers weekly ads from some 800 retailers, including supermarkets, dollar stores, pharmacies, and big retailers such as Target and Walmart. If you add your loyalty-program numbers, some discounts will automatically be applied when your loyalty card is scanned at checkout, without any physical coupons.

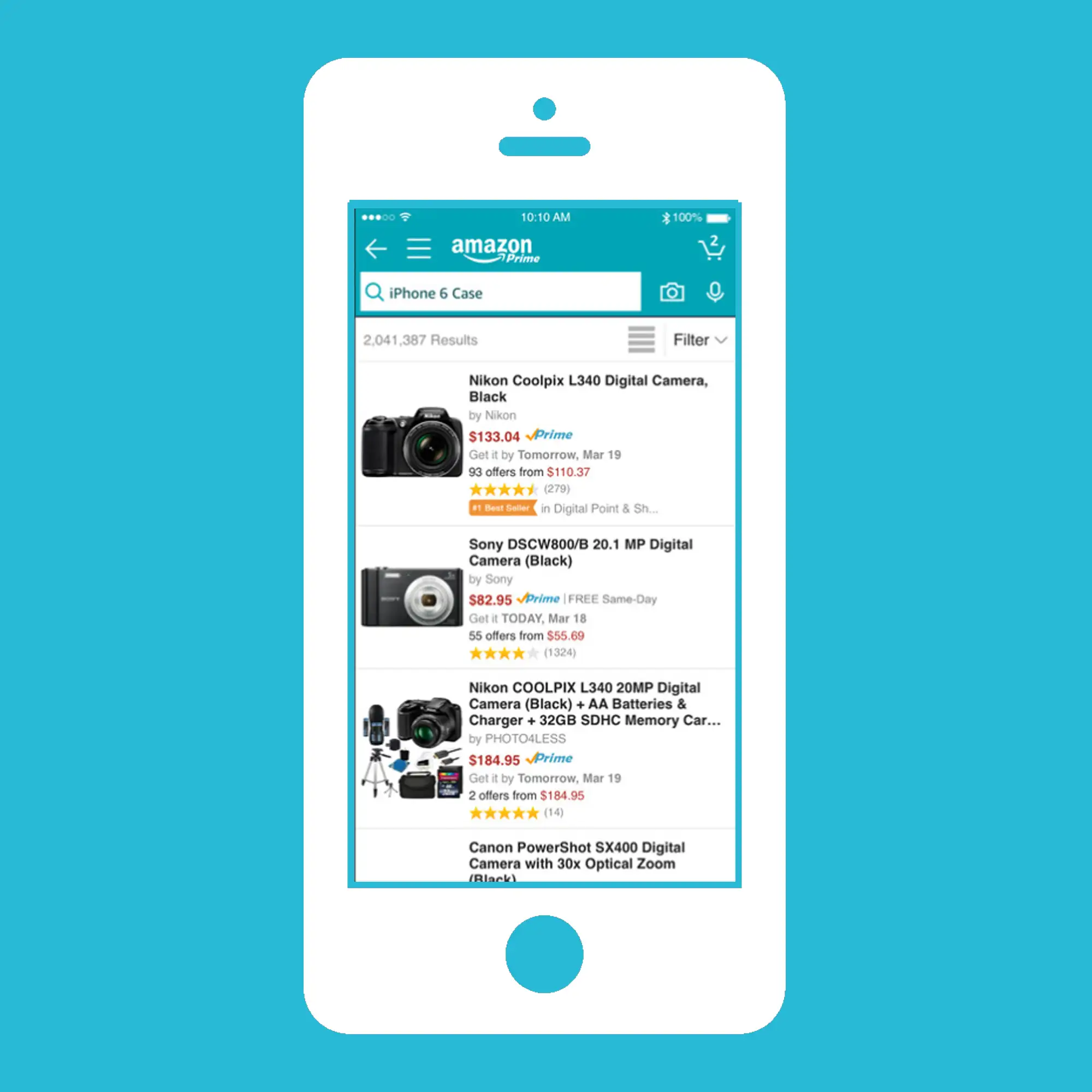

Amazon

The world’s largest e-retailer sells nearly everything you might want to buy. Its app is handy too. You can see prices and product information for items you scan, take a photo of, or say out loud to your phone. In a store or on the go, you can access Amazon’s massive volume of user reviews and side-by-side product comparisons. You can check your Amazon order history, update your Wish List, and browse the retailer’s short-lived Lightning Deals too.

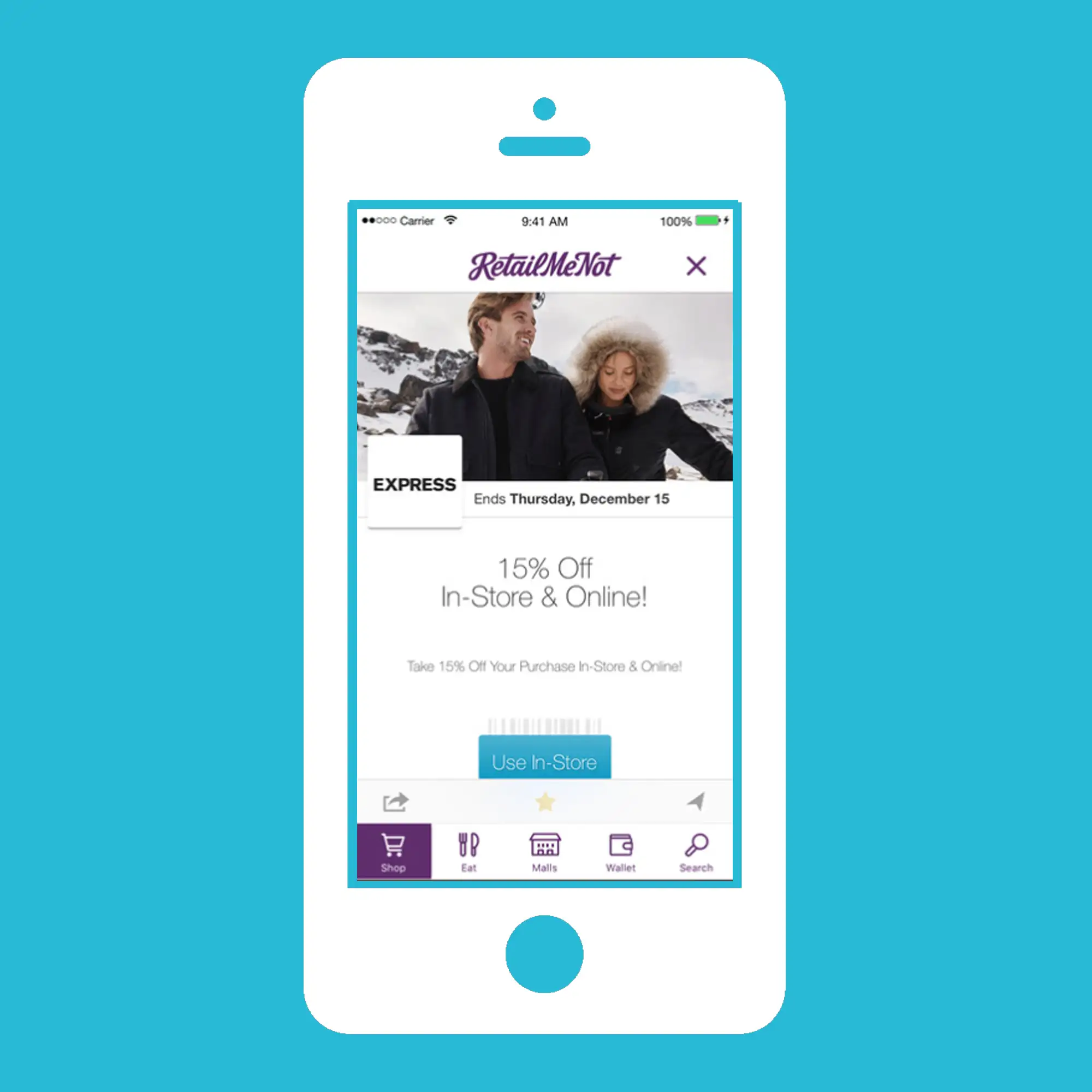

RetailMeNot

Smart shoppers consider the list price merely a starting point that they’ll inevitably be able to beat with a few clicks of a mouse or swipes of a smartphone. The RetailMeNot app is a must-have for savings, with promotional codes, coupons, and other discounts at 50,000-plus restaurants and major retailers, and deals for physical stores and online purchases alike.

ShopSavvy

The ultimate “showrooming” tool, ShopSavvy allows you to inspect merchandise in the store and scan the bar code to compare prices from dozens of online competitors and local stores (but not Amazon, unfortunately). The app offers special cash-back deals from major retailers, and you can set up notifications to alert you when a desired product goes on sale.

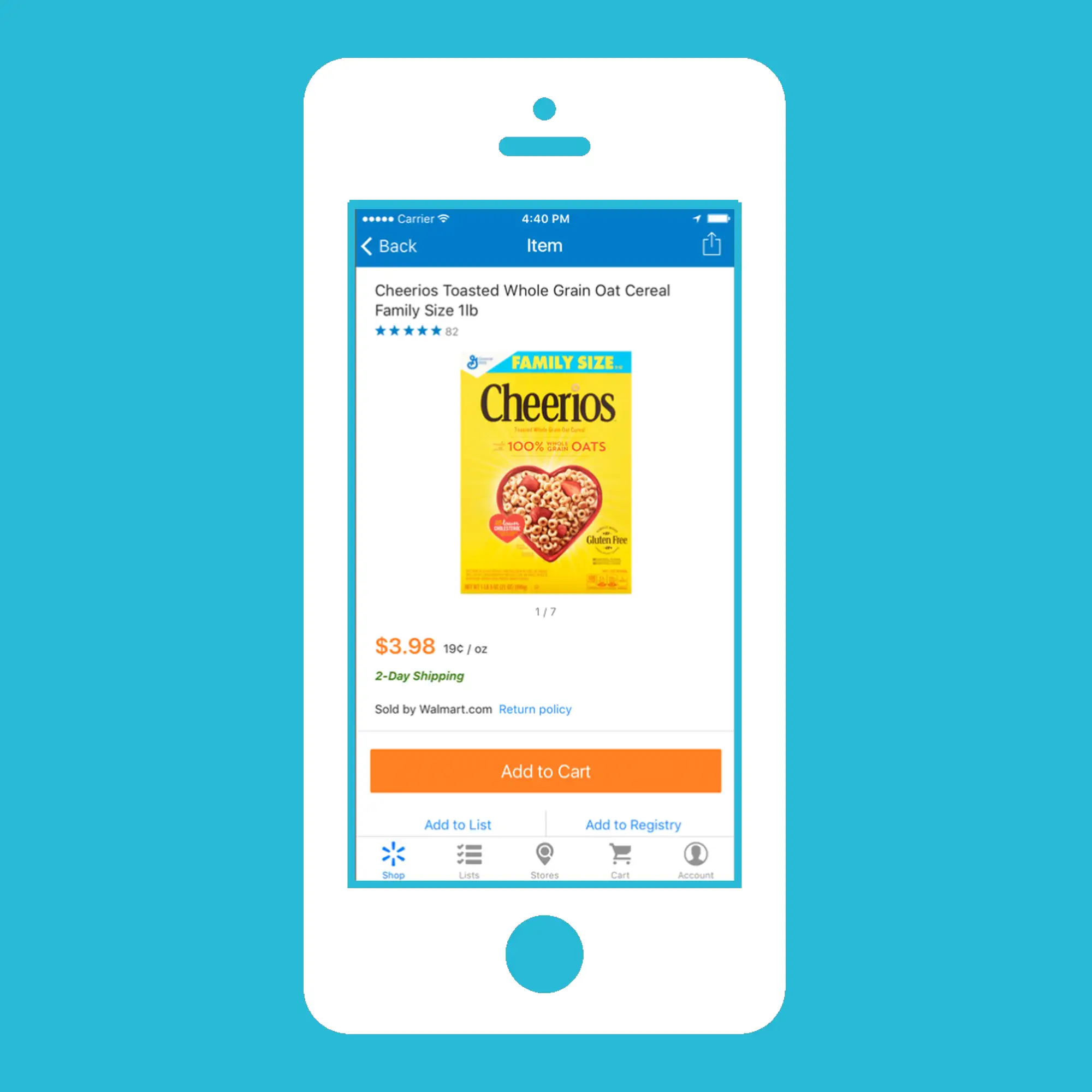

Walmart App

If you’re a Walmart shopper, the giant retailer’s app is invaluable for no-effort savings. Simply scan store receipts, and the Savings Catcher feature checks whether competitors offer lower prices. If they do, you’ll get the difference refunded to you in the form of Walmart credit. The app’s newest feature lets you skip store lines for picking up prescriptions.

WayUp

This job and internship search tool is for current college students—you need a .edu email address to sign up. To be matched with openings for summer and post-graduation employment, you create a WayUp profile that includes your academic accomplishments and career interests. You can also search for opportunities based on location and industry type. Apply straight from your phone or save jobs you’re interested in to pull them up later on your computer.

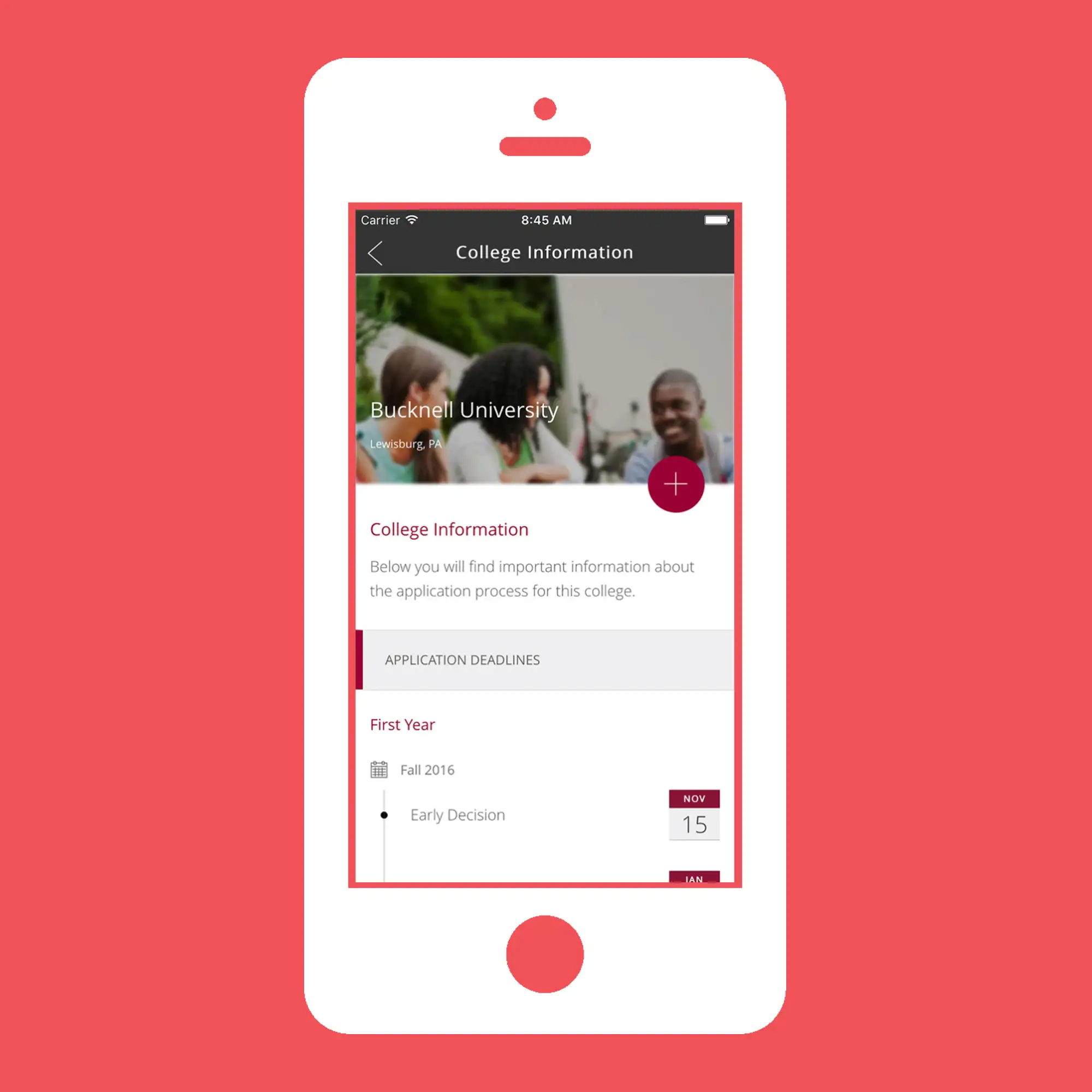

Common App onTrack

High school seniors may apply to many of their picks online via the Common App, accepted by 700 colleges. The website’s companion app is a handy organizational tool, and it allows teens to access much of their application information from their smartphones. You can search colleges’ writing prompts, keep track of deadlines and the status of your applications, connect with teachers who are writing your recommendation letters, and set up reminders for your personal to-do list.

Schoold

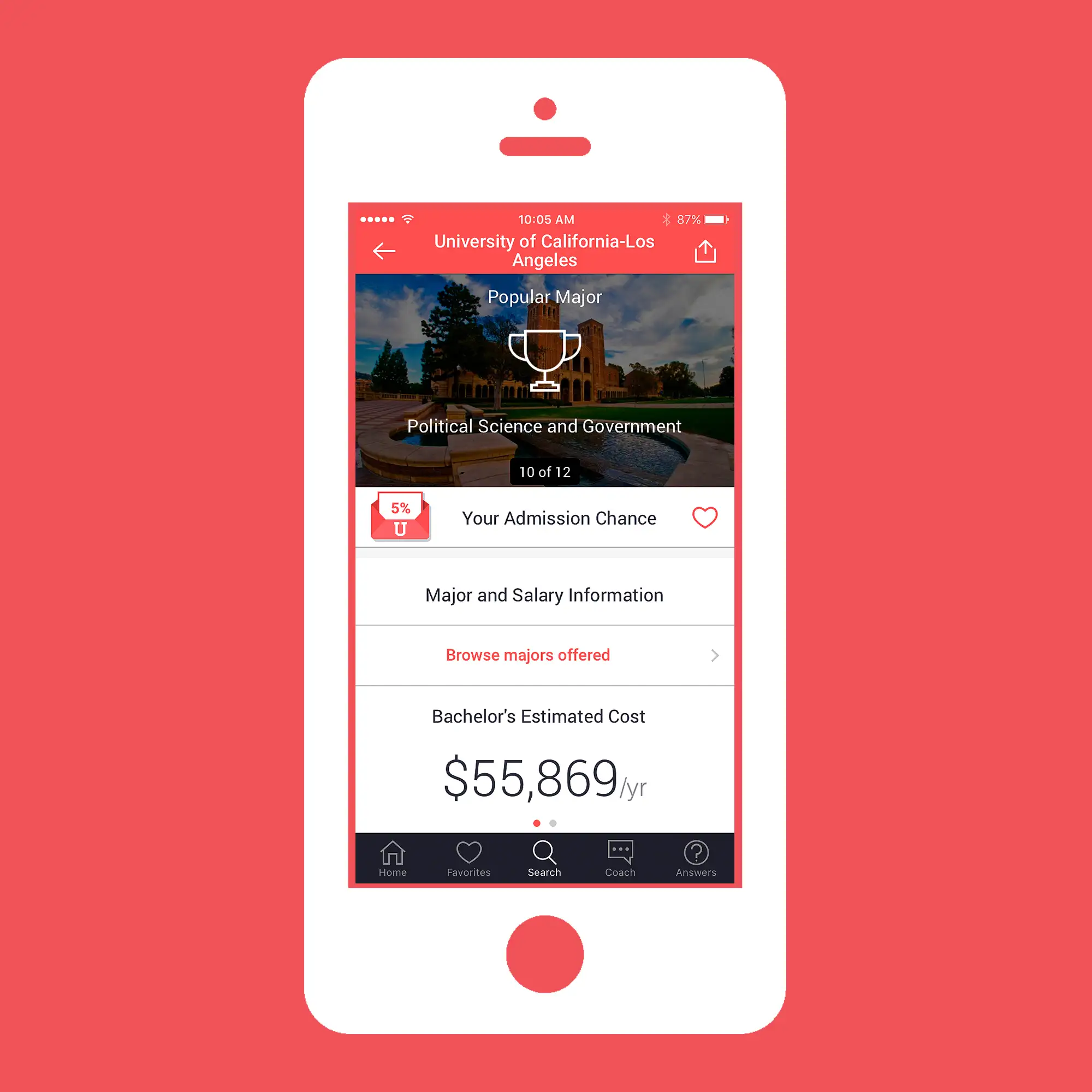

Schoold takes on the role traditionally filled by college guidebooks and search websites and spins it into a sleek, easy to use app. You can search lists of colleges curated by major, careers, or locations, and quickly browse details about costs, student body demographics, and scholarships at individual schools. One of its most engaging features is the “coach” function, through which students can text admissions questions and get responses from experienced counselors.

College Abacus

Colleges are required to provide an online calculator that helps students estimate what they would have to pay after scholarships and grants are subtracted from the school’s sticker price. But those calculators can be hard to find—and to compare colleges, you have to submit the same personal information on multiple websites. College Abacus makes it easy: It incorporates information from the net price calculators of roughly 2,600 four-year colleges so you can check out multiple schools at once.

Get Schooled

You know Mary Poppins’s old trick about the spoonful of sugar? This website uses gamification to teach high schoolers about the college admissions process. Students earn points toward rewards like a backpack or calculator as they prep for standardized tests or learn about financial aid forms. This site was set up by a nonprofit group working to boost college enrollment among underserved populations, but it could be just the ticket for any student who needs a little extra motivation.

BrokerCheck

It’s an investor’s worst nightmare: working with a financial advisor who turns out to be a crook. It’s easy to do a background check at this site run by industry regulator FINRA. You’ll see how long brokers have worked in the industry, a list of past employers, and any black marks—identified as “disclosures”—on their records. You can research firms as well. If you look up someone who is a “registered investment advisor” or an investment advisory firm—which are overseen by the Securities and Exchange Commission or a state regulator rather than FINRA—BrokerCheck will take you to the SEC site for the same type of information.

Betterment

At least 0.25% of assets a year

Are you or someone you know looking to get started in investing? Betterment and other so-called robo-advisors ask you a few questions and then invest your money in a low-cost portfolio of exchange-traded funds. You can watch the progress of your account online, while your holdings are periodically rebalanced back to a target mix of stocks and bonds. Betterment’s fee—which works out to $125 a year on a $50,000 nest egg—is on top of expenses averaging 0.13% of assets a year for the underlying ETFs. Investors with at least $250,000 at Betterment can pay higher fees (up to 0.5%) for unlimited calls with a team of certified financial planners.

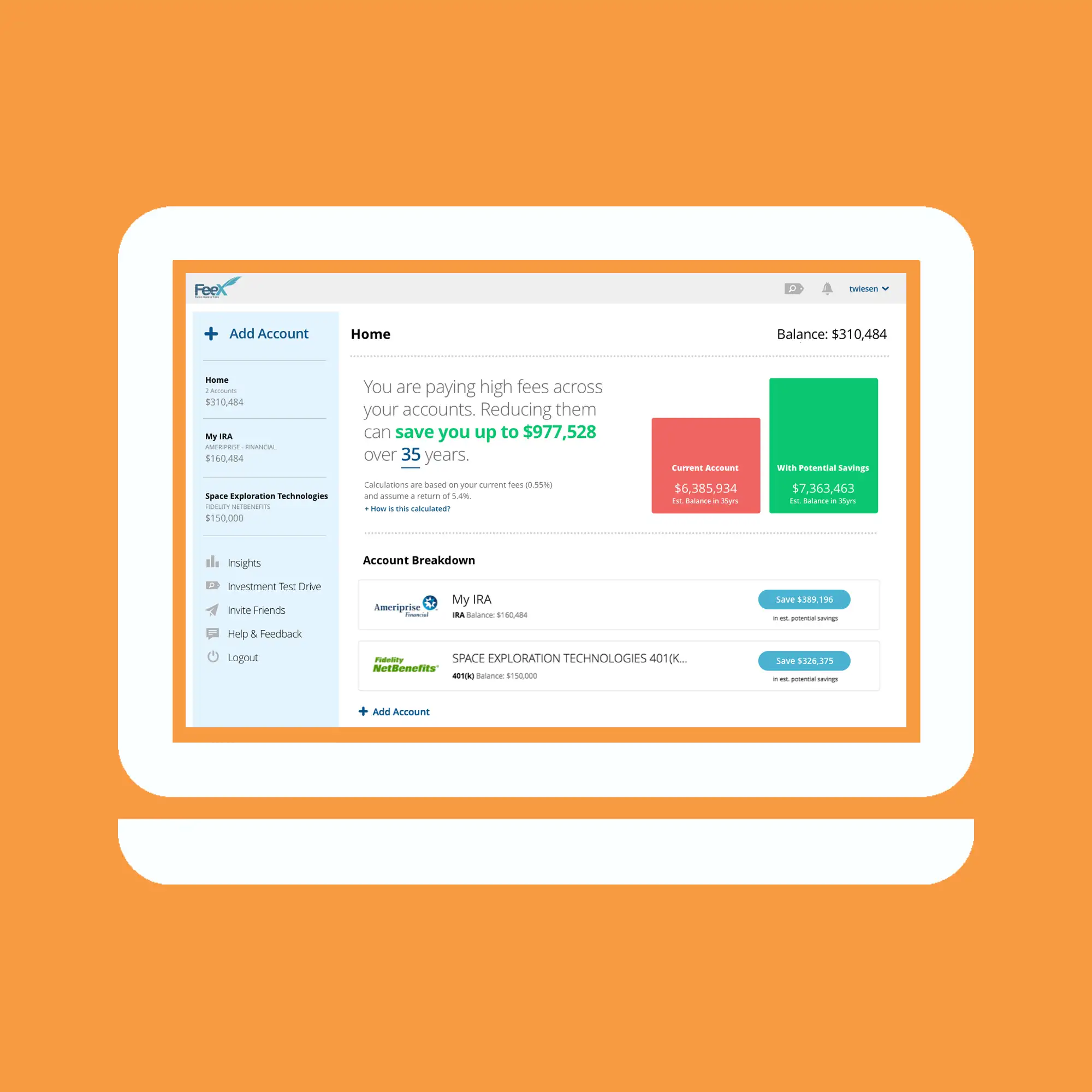

FeeX

Not sure about the costs of your 401(k) or other investments? Link your accounts to FeeX and it will check what you are paying your advisor or retirement plan directly, as well as the cost of individual investments like mutual funds. Each investment portfolio receives a grade—from A+ for total fees of 0.05% of assets a year or less to F for fees of 1% or more. FeeX will also suggest lower-cost alternatives to your current holdings or recommend a rollover if your 401(k) plan or IRA offers what it considers a subpar menu of options. While FeeX’s fee checkup is free, the company receives referral payments from investment companies when it recommends a rollover.

Personal Capital

Free (for the basic tool)

This service’s free “dashboard” lets you see all your investment and other financial accounts—including your 401(k)—on one screen if you share your login information. That means you can check that your overall mix of stocks and bonds is what you want it to be even if, say, you keep bond funds in your IRA and stock funds in a brokerage account. If you sign up, expect the company to pitch you to hire Personal Capital to manage your money for a fee of up to 0.89% of assets a year; in that paid service, it pairs investors with financial advisors online and over the phone.