An Opaque Web of Credit Reports Is Tracking Everything You Do

Liam Downey remembers the first time he heard about ChexSystems. It was December 2021, not long after he moved to Mancos, Colorado, a tiny mountain hamlet with a population under 1,500.

The only bank in town had just barred the 52-year-old flight paramedic from opening an account because his so-called ChexSystems score was too low. The teller gave him the contact information of the agency but not much else. He walked out of the bank perplexed.

ChexSystems, as Downey would soon find out, is a national consumer reporting agency — abbreviated CRA — that specializes in gathering data on how Americans use checks and bank accounts. It distills this information into a score similar to a credit score. Some 80% of banks rely on such information to screen people who want to open new accounts.

On a scale of 100 to 899, Downey’s ChexSystems score was 553. As far as the sole bank in Mancos was concerned, those three digits — regardless of his 15-year-long relationship with his current out-of-state bank — meant he was too risky to take on as a customer.

“I think this is complete nonsense,” Downey says of the reporting system. “People don’t even recognize it exists. It’s not easy to interpret, it’s not easy to change, and it’s completely arbitrary.”

Critics of ChexSystems note the agency generally tracks only negative information like account closures and overdrafts, essentially making it a bank-account rap sheet. The company is just one of a large — and largely unknown — sum of CRAs that actively monitors the financial and nonfinancial behavior of more than 200 million Americans, including many children.

Most of us are familiar with Equifax, Experian and TransUnion, the big three credit bureaus behind our credit reports and scores.

But that’s barely scratching the surface.

“There is a very large web of these different types of consumer reporting agencies,” says Ariel Nelson, a staff attorney at the National Consumer Law Center (NCLC) who specializes in consumer reports.

Nobody knows exactly how many agencies there are because there’s no federal registry overseeing them, Nelson says. Her best guess? It’s likely in the thousands — at least.

Our ‘financial surveillance’ system

Rent a home. Bounce a check. Return an item to a retailer one too many times. Miss a utilities payment. Make a utilities payment. Change jobs. Apply for health or property insurance. Get a raise.

In any one of these everyday scenarios, there’s a good chance your information is being logged, cross-referenced, bought, sold and scored among a sprawling network of consumer data brokers. And that data can be used against you when it comes time to apply for a loan, land a job, rent a place to live and even innocuous things like sign up for a new phone plan.

For Downey, ChexSystems stood between him and a local bank account. When we spoke in the spring — months after he first ran into these problems — Downey still hadn’t gotten a hold of ChexSystems despite several phone calls.

Since cash is king in Mancos (this is Smalltown, USA, after all) he had to max out his ATM withdrawal limit for daily expenses using his out-of-state account. Inconvenient, yes. But he was grateful for the workaround. Others in his position — like the millions of unbanked Americans who don’t have a checking or savings account at any bank, out of state or otherwise — don’t have this option.

Recent research from San Francisco’s treasury department shows that bank scoring disproportionately restricts low-income and Black Americans from opening accounts, amounting to what the authors call “systemic financial exclusion.”

The federal government is taking note, too. The Consumer Financial Protection Bureau, or CFPB, is cracking down on consumer reporting agencies, and not just at the big three credit bureaus. Niche companies like ChexSystems are now getting scrutinized, too.

Director Rohit Chopra, who’s helmed the CFPB since October 2021, has worked to shift the federal agency’s tone towards consumer reporting. In news releases and advisories, it now calls CRAs “financial surveillance companies.” And the reports they peddle? Those are “dossiers.”

Nelson, of the NCLC, welcomes the change in rhetoric.

“These companies are becoming the gatekeepers to essential things in our lives,” she says.

Your every move, logged and scored

You probably never asked to be a part of this financial data matrix, and you can’t fully opt out, either. What you can do is watch the watchmen, so to speak. But you’d better clear your schedule.

To get a better sense of how daunting this task is, I pulled several of my own reports. The CFPB keeps a list of roughly 60 of the largest consumer-reporting companies. I chose six of them: “the big three,” ChexSystems, The Work Number (an employment-history agency owned by Equifax) and LexisNexis (a data firm that tracks property, bankruptcy and other public records).

Pulling these six reports took about five hours. I had to ace timed multiple-choice questionnaires. Answer wrong, and I'd get locked out. I had to send multiple emails to company help desks because the web pages to request my reports did not work properly. To access my employment-history report, I had to send in scans of a recent pay stub and my driver’s license over an encrypted email service.

In most cases, I received a digital copy of my report once I cleared the gauntlet. But some companies only send reports through snail mail, so it can easily take weeks to compile everything.

The breadth of my consumer files was eye-opening. The reports included past jobs, about a dozen previous physical addresses, email addresses, phone numbers, salaries, past and present debts, assets and more. In some cases, the information was incredibly specific: My employment report, for instance, included a breakdown of the number of hours I worked each week when I was a server at a quasi-French restaurant in 2013.

What was missing was just as troubling: eight years of employment in the meantime.

Attorney Daniel Cohen, a founding partner of a New York-based law firm that specializes in suing CRAs for violating federal law, says he’s represented hundreds of people who have had issues with their consumer reports.

For the most part, by the time Cohen’s clients reach him, they’ve already lost a promising job opportunity or apartment due to something an employer or landlord found in their report.

“You now got denied a job. You now got denied an apartment,” Cohen says. “What are you supposed to do?”

This is where your limited legal rights come into play. Under the federal Fair Credit Reporting Act, you are allowed to dispute incorrect, incomplete or outdated information on your report, and the reporting agency is obligated to investigate and correct the issues, usually within 30 days.

In reality, the agencies are notoriously slow to act. If the error results in monetary damages — say, you were denied a job over a mistake on your report — Cohen says you can sue to recoup those losses plus legal fees.

Getting to that point can be a slog that will likely require legal aid. One of the first hurdles is figuring out why, exactly, your application was denied. If you were rejected due to something on your consumer report, the company or person who pulled it is legally required to tell you why and give you the information of the reporting agency they used.

So when Downey was denied a bank account, the teller who mentioned ChexSystems wasn’t doing him a favor. That’s the bare minimum required by federal law. Without this disclosure, he would’ve never heard of ChexSystems at all.

It’s a similar story for Lynn, a Florida resident who’s been coping with the financial fallout of an eviction in 2020. (Money has chosen to refer to her by her middle name because she fears being publicly associated with eviction will only make her hunt for an apartment harder.)

Lynn was evicted right before COVID-19 ravaged the U.S. In January 2020, she fell a few days behind on her rent, court records show. By Jan. 7, her landlord terminated her lease, “effective immediately,” and a judge signed off on the eviction soon after.

The eviction doesn’t show up on her regular credit report, but it does blemish her tenant report — a category of CRA files that tracks rental history, job history, credit scores, evictions and lawsuits. They also cross-reference terrorist watchlists and sex-offender registries.

When landlords pull these reports, even a whiff of a prior eviction can lead to a denial. For one, court decisions — including those in the favor of the tenant — often show up on tenancy reports. Landlords might look at the report, see a court judgment and conclude the applicant could be too much of a headache.

And if they spot a full-blown eviction? Denied. Often without a second thought.

Once an eviction makes it on a consumer report, it can stay there for seven years, leaving applicants like Lynn with little to no recourse. (Consumer advocates sometimes refer to eviction as a “Scarlet E” because of its long-lasting consequences.) Only a handful of states have laws that seal eviction-related court records, effectively preventing them from showing up on a tenancy report. Florida, where Lynn lives, isn’t one of those states.

“That has made it impossible to find anywhere to rent,” she says.

For two and a half years, Lynn has been staying in a hotel room, paying about $2,000 a month. When she’s not working or taking classes toward her master’s degree, she’s hunting for a place to live.

This saga has given her an unsolicited crash course in consumer reports.

“Now I know that just because it's not on your credit,” she says, “doesn't mean it's not on some sort of behind-the-scenes system.”

Big data, bigger mistakes

Besides tracking our every move, consumer reporting agencies are also really good at convincing landlords, employers, banks and insurers that they need the dossiers they’re selling.

More than 90% of employers — and nearly as many landlords — rely on reporting agencies to run consumer background checks, according to Nelson from the National Consumer Law Center.

Sure, it makes sense that the person screening my job or apartment application would want to know if I have an open felony. But do they really need to know my credit score, or my past four telephone numbers, or the fact that I got a traffic ticket in 2015 (which I contested in court and won, by the way), or how many hours I logged in that part-time job a decade ago?

It gets even creepier. According to a new paper in the spring issue of the American Business Law Journal, CRAs and financial technology companies are gathering more behavioral and lifestyle information — everything from SAT scores to social media posts — to make inferences about how credit-worthy people are.

“The scope of data that’s out there,” says Lindsay Sain Jones, a legal studies professor at the University of Georgia and co-author of the report, “is sort of mind-blowing.”

Jones refers to this as “alternative fringe” data collection, and she says it’s sometimes dubiously sourced and scraped right from the web without consumer consent. The use of this data is often draped under the guise of helping unbanked or “credit-invisible” populations, which tend to fall along racial and class lines.

Thankfully, this practice has yet to be widely adopted, though that could soon change as more CRAs adopt an “any data is credit data” mentality.

“We're concerned about how more and more information is making its way into these models,” says Sophie Sahaf, a deputy assistant director at the CFPB, “and what that means for surveillance risk for consumers and intrusion into their lives."

One of the biggest hurdles in keeping this underground financial surveillance system in check is that most people don’t even know it exists. Until something goes wrong, that is.

As reporting agencies vacuum up more information, they also tend to get sloppier with the data. Nelson, of the NCLC, says files are often automated and almost never checked by human eyes. The inevitable result? Widespread errors.

Name-only matching, a particularly error-prone technique reporting agencies use to inflate their consumer files, is one example.

The CRAs that use this technique run your name against public records, and then they add whatever information comes back to your file. Sometimes, they’ll run shortened versions or variations of your name — even if you’ve never gone by that name before. And if it just so happens that there is someone out there who does go by that name, their data could end up on your report.

“So if your name is Robert Smith, maybe they are [matching data with] Rob Smith, Robbie Smith, Roberta Smith — all these different names,” Nelson says. “That leads to big inaccuracies.”

Following a deluge of complaints, the CFPB took several actions recently, including issuing an advisory opinion in November 2021 that stated name-only matching violates the Fair Credit Reporting Act. It also put out an interpretive ruling in late June, clarifying that individual states can enact stricter regulations on consumer reporting agencies.

“All of these [actions] are really intended to protect consumers from being blocked from opportunity with housing, with employment, et cetera because of these sloppy practices,” Sahaf says.

It’s impossible to tell how effective the changes will be. What is clear, though, is that mistakes in our consumer files are rampant right now.

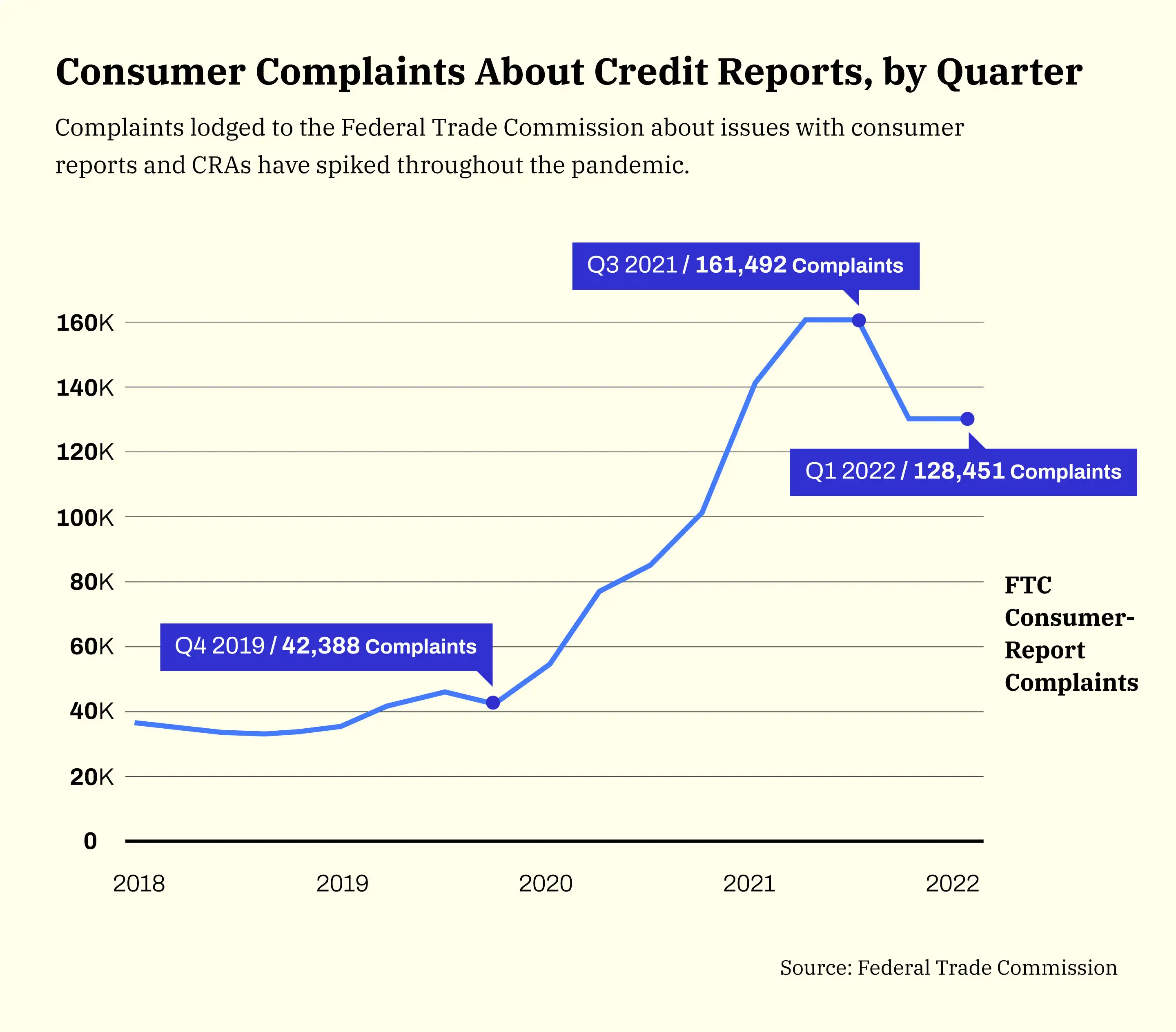

Folks are lodging more complaints about consumer reporting agencies than ever before, according to data from the Federal Trade Commission. In 2021, Americans filed nearly 600,000 complaints about their consumer reports. That’s an increase of more than 250% compared to recent pre-pandemic years.

Getting information removed from these reports is an option only if it’s incorrect or outdated. If the information checks out, the credit reporting agencies logging and scoring every aspect of our lives aren’t obligated to do much. Even if it’s unclear why anybody would want the information they’re peddling in the first place (see: my schedule at a decade-old restaurant job).

We are essentially forced to live with any negative information until it ages off our reports. That can take years, or perhaps a decade, depending on the financial folly.

Back in Florida, Lynn is still in the thick of her fight to find a place to rent. Her eviction won’t age off her report for another five years. In the meantime, she’s praying for a break — maybe a landlord will look beyond the eviction and decide that she deserves a place to call home.

Downey, for his part, recently got some good news. In early June, he returned to the lone bank in his tiny Colorado town, this time “loaded for bear” with his ChexSystems report, latest tax return and bank statements dating back to 2005.

When he arrived, trove of documents in hand, the same teller from his first visit told him the paperwork wasn’t necessary. She was going to override any issues. When she pulled Downey’s ChexSystems report as a formality, to their surprise, it came back in good standing — despite Downey not having changed a thing. Maybe whatever was keeping his score down aged off his report in the months following his first visit. The report doesn’t specify, so there’s no way of knowing for sure.

“At any rate,” Downey says, “I now have a local account, and the bank was willing to take a risk by treating me like a human being and a community member, and not simply a metric on a report.”

More on Credit & Credit Repair

Money’s Top Selection Guides for Improving Your Credit

Money’s Credit Repair Companies Reviews |