This Company Will Pay Your Private Student Loans for 6 Months If You Can't Find a Job

- How to Pay Off Student Loans Fast

- Biden Reveals New Student Loan Forgiveness Plan — Here's What Borrowers Can Expect Next

- How Student Loan Borrowers Can Prepare for Big Changes Coming in 2023

- Here's Exactly What the Student Loan Forgiveness Application Will Look Like

- Student Loan Payment Pause Extended Through End of 2022

Private student loans are one of the riskiest ways to pay for college, since they're pricier than federal loans and lack robust consumer protections. One college advising company plans to shoulder some of that risk for its customers with a new private student loan guarantee.

The company, Edmit, will cover six-months’ worth of private loan payments for eligible students who don’t find a job within a year after graduation. Edmit, which focuses on helping families make a more financially informed decision about where to go to college, is pitching its new product as a safety net for students who need more than federal student loans to be able to afford a specific school.

With this offer, the company wants to give students using its services a type of insurance, co-founders Nick Ducoff and Sabrina Manville say. Edmit's promise to cover some of students' loan payments is unique within the private student loan market. But the company is part of a growing network of startups, lenders and organizations looking for innovative and alternative ways to pay for college.

“If Edmit says it’s good and it ends up not being good for you, we should have some skin in the game,” Ducoff says.

Most experts recommend students stay within the federal system and avoid private debt altogether. But that is sometimes easier said than done, particularly in states where even in-state, public college tuition isn’t affordable if a family hasn’t saved for college or if the student or parents can’t pay some of the bills out of current income.

Take Pennsylvania, for example. Federal data show that four-year public colleges in the state charge families earning between $48,000 and $75,000 an average net price of about $20,000 a year. (The average net price for that income group at private colleges in the state is slightly more, at $22,300.) That’s the price families pay after subtracting any federal, state and institutional grants and scholarships.

Yet dependent students (typically, any student under 24 years old) can only borrow between $5,500 and $7,500 a year in federal student loans, depending on their year in school. So after maxing out federal student loans, a typical family might need to close a gap of anywhere from $12,500 to $14,500 a year. To pay that amount, there’s either parent PLUS loans, private loans, current income, savings or third-party scholarships.

Edmit’s new offering, Ducoff says, is really targeted toward people who are weighing private student loans versus parent PLUS loans to close that gap.

How the private student loan guarantee works

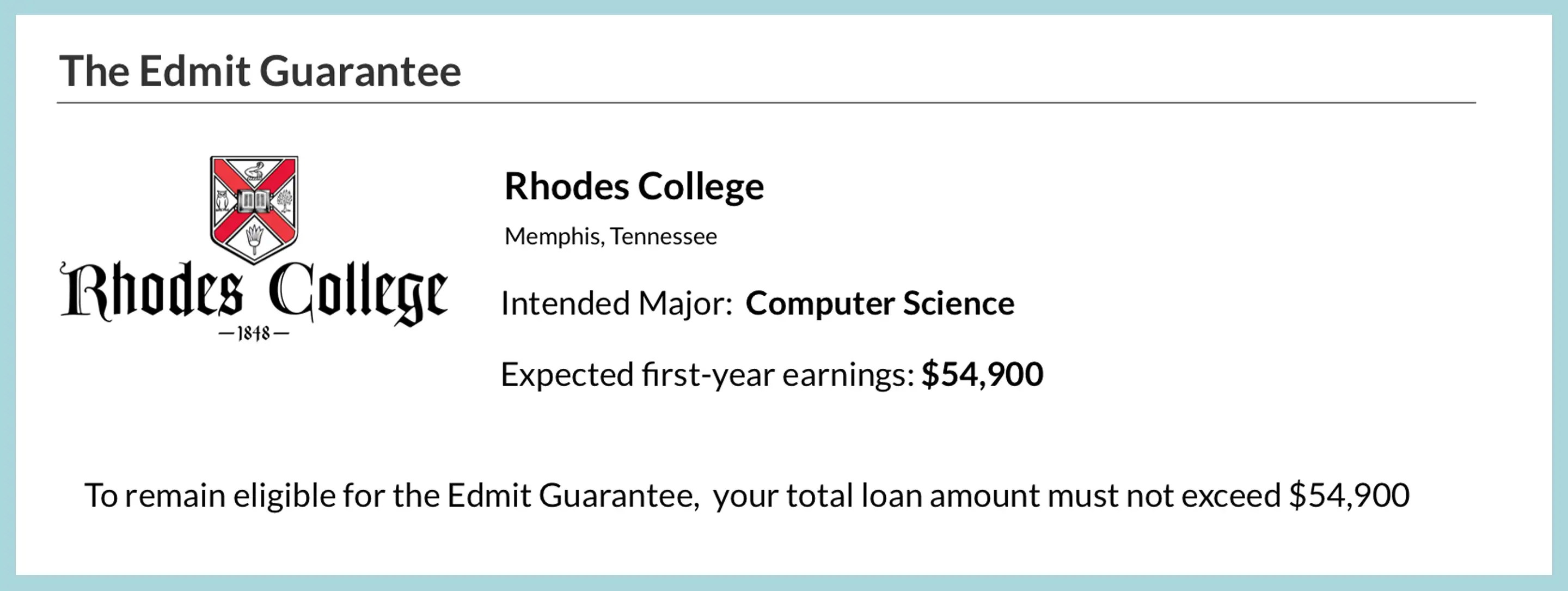

Edmit has data on about 1,500 colleges, and the eligibility for the guarantee is personalized, based on how you’re planning to pay for college and what you’re studying.

To see if you’ll qualify, you need a tuition bill that shows how much you’ll be paying out of pocket. Edmit has a calculator where users can input their scholarships, college savings and loan amounts, and it will help you tally an expected four-year borrowing total, including federal and private loans. If that total is less than what Edmit estimates the first-year salary in your major is likely to be, then you’re eligible for the guarantee.

After graduation, if you can’t find a job or are earning less than $20,000 a year, Edmit will make your private student loan payments for you for up to six months.

“It really is hyper-personalized to the student,” Ducoff says, explaining that two students at the same college, studying in the same academic area may not qualify, based on their borrowing plans compared with their predicted return on investment.

For now, the offer is only available to freshmen starting college this fall. They can check their eligibility now, and officially sign up this summer.

Edmit anticipates having six lenders students can choose from. If students end up borrowing from one of those lenders through Edmit, the company will get paid by the lender. That revenue is what will fund the guarantee. In the future, the company says it hopes to offer more borrowing choices for students.

Last month, Edmit was acquired by Vemo Education, which designs and manages income share agreements, a financing model where students agree to pay back a portion of their income as an alternative to a traditional loan. While Edmit’s guarantee offer is not an income share agreement, it does stem from the same philosophy: that students should be able to share some of the risk of financing a degree with a college, lender or third-party stakeholder.

Edmit says it sees this as just a baby step. The goal is to expand both the duration of the guarantee beyond six months, and the earnings threshold to qualify, and the company is looking for ways to fund a similar guarantee for federal loans in the future.

Yet one significant downside to a guarantee with a flat income threshold is that it’s hard to set universal parameters for what it means to struggle with debt, says Dominique Baker, an assistant professor of education policy at Southern Methodist University. If someone gets a job earning $25,000 — above the threshold for Edmit’s guarantee — will they be able to afford private student loan payments, particularly if they work in a high cost-of-living area?

“It becomes tricky to know where the line is for people who need help versus people who don’t,” she says, adding that she had more questions than answers about Edmit’s new offer.

What students (and parents) should know before using Edmit's guarantee for private loans

One of the biggest takeaways for students considering this product is to think about it as bonus if you were already going to take on private student loans, says Beth Akers, author of Making College Pay and a resident scholar at the American Enterprise Institute. It should not convince you to take on private debt if you can fill the gap in other ways. Here are some other tips to guide you:

Max out federal student loans first. Edmit stresses this, but it’s worth repeating: You should not take private student loans until you’ve borrowed the maximum amount allowed for federal student loans. At the undergraduate level, that’s up to $7,500 a year for dependent students, or $12,500 a year for independent adult students.

Consider whether your education plans might change. Many students either switch majors or transfer schools. That, on its own, doesn’t disqualify you from the guarantee, but it does complicate it since earnings can vary widely based on your area of study. When students sign up for the guarantee, they’ll get a list of approved majors or schools they can switch to and still have the agreement hold up.

The guarantee applies only to graduates. You won’t get the benefits of the guarantee unless you’ve earned a degree. That may sound obvious, and most students likely enroll with the expectation that they’ll finish, but nationally, some 40% of first-time students do not earn a bachelor's degree within 6 years.

Think about the long-term commitment of the loan. The offer only provides protection for six months, measured from when the grace period on your loan ends. (For most lenders, that’s six months after leaving school.) That’s a major difference from federal loans, where the protections last for the life of the loan, Baker says. The pandemic is a prime example. Most federal borrowers haven't had to make a payment in over a year, while private borrowers have had to fend for themselves. And while the widespread financial upheaval of the pandemic will hopefully be a once-in-a-generation occurrence, Baker says, economic shocks happen on an individual level all the time, whether it's a job loss or unexpected expenses.

"It takes a lot of money and capacity to provide that type of support for the life of the loan," she says. "That's why we rely so heavily on the federal loan system."

More from Money:

Left out of Pandemic Relief, Private Student Loan Borrowers Are Still Struggling a Year Later

Americans Are Divided About Forgiving Student Loans. These Borrowers Are No Different