If You Want Your Kid to Help Pay for College, Read This

You've been preparing your child for adult responsibilities for years. Now, in your kid's senior year of high school—college acceptances and financial aid offers in hand—you face a pivotal question about responsibility: How much money should your child raise for college, either through earnings or loans?

Your finances may make it necessary for your child to shoulder at least some of the cost—even if your student manages to land scholarship money. (Public universities average $18,000 annually after grants; private colleges, more than $30,000.) Or maybe your child's dream school is just out of your budget.

And even if you can afford it all, you may want your child to help pay; having some skin in the game will help him or her take college more seriously. About half of students from families earning more than $106,000 a year put in their own money through work or loans, according to federal data.

- Read more: Honey, Who's Going to Pay for College?

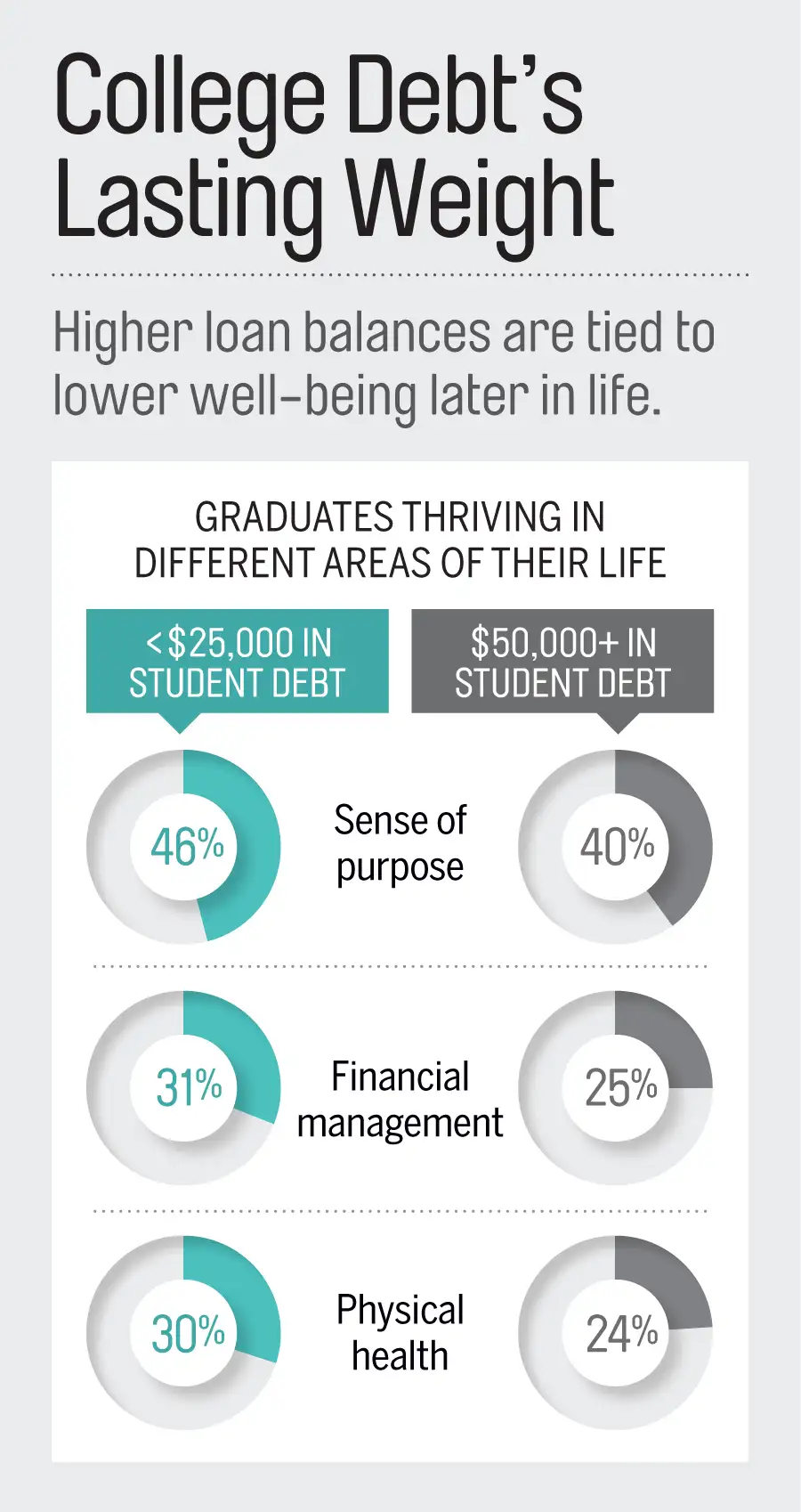

But too much financial pressure raises risks that students will drop out or that they will struggle with oppressive debts for years. Follow these guidelines to get your student's contribution just right:

Have Them Find Part-Time Work

Nearly all students can and should earn their "extras" money for items like Saturday night pizza, advises Julie Lythcott-Haims, Stanford's former dean of freshmen and the author of How to Raise an Adult. "You will be instilling in your child the idea that nothing in life is free—that stuff comes from working hard," she says.

Plus, federal education data shows that students who work up to 12 hours a week—enough, at minimum wage, to raise about $2,000 during the school year—get better grades than those who don't work at all. In part, that's because a job schedule imposes discipline, says Kalman Chany, author of Paying for College Without Going Broke.

Beware, though, of too heavy a load while classes are in session. Federal data also shows that working more than 15 hours a week during the school year raises the chances of dropping out. And watch out for earnings caps: Some schools cut need-based grants to students earning more than about $6,200 from nonschool jobs. (Co-op and work/study don't count.)

Put a Limit on Loans

Most experts have this rule of thumb for students: Limit your total borrowing to your expected first year's salary after graduation. That generally means sticking with federal loans (typically capped at $5,500 a year for freshmen and $7,500 for upperclassmen).

Only students certain to land high-paying jobs should consider private loans, says Chany, since those loans lack the income-based repayment and forgiveness options of federal loans.

If a school is so costly that your child would have to contribute more than $9,000 annually from work and loans, "you have to be a parent and say no," says Chany. After all, students should risk a little skin—not their entire future.