What Millennials Want That Their Boomer Parents Hate

Inflation. We really want some inflation. Now, if possible.

Macroeconomic forces are not top of my mind all the time. A couple of weekends ago, for instance, my wife and I played poker and drank beer on our friend’s rooftop patio. Our son Luke, clad in his new miniature gondolier outfit, crawled between our legs as one person after another told us how cute he was. That night Luke held onto one of my fingers while I gave him his midnight feeding. Later my wife and I slipped into his room for a few moments to watch him sleep.

I can tell you that at no point during our perfect summer day did the word inflation pop into our heads. We went to sleep thinking just how lucky we were to have such a beautiful son, rather than dwelling on the fact that we face an inflationary climate that is hostile to the economics of our new family.

We aren’t strangers to what economists call “headwinds.” Mrs. Tepper and I graduated from the same really expensive private college in 2008, just as the nation was mired in the worst recession in 80 years. We attended college (and later graduate school) as state governments across the country drastically cut higher education spending, which meant higher costs, which meant that we incurred a combined six-figures student loan marker. And entering the job market in the teeth of negative economic growth means we'll be playing catch-up for years and years.

Given all that we (and Americans, generally) have endured since 2008, it might seem strange that I would ask for higher inflation. When the prices of goods rise quickly, the Federal Reserve is apt to raise interest rates. Higher interest rates make it more expensive to purchase a house, or borrow for anything. Don’t I want to own a house? What’s wrong with me?

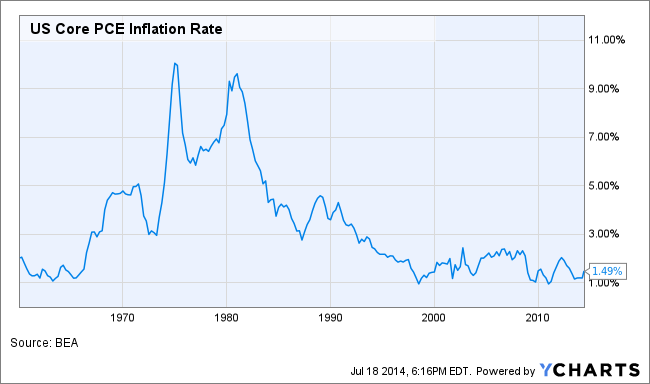

For a little bit of context, let’s back up and look at where inflation has been over the past six years. If you look at the core price index for personal consumption expenditures (or core PCE), inflation is rising at an annual rate of 1.5%. In fact ever since Lehman Brothers declared bankruptcy it has barely budged over 2%.

Even if you look at a broader inflation metric, like the consumer price index, prices have risen at 2.1% or lower for almost two years.

What does this mean?

For one thing, wage growth has stagnated at around 2% since we left school, and job growth, while picking up lately, has been relatively slow. Weak job creation and small pay increases means that people have less money to spend, which means fewer jobs and the cycle goes round and round.

So more economic growth (spurred on by more borrowing and spending) would help alleviate low wage growth, and help us ramp up our weekly paychecks. But it would also do something else. It would help us pay down our student loan debts.

Super low inflation is bad for people who have debt. Right now Americans owe more than $1.1 trillion in student loan debt. That means people our age are receiving raises that aren't that high and have to confront a record level of debt before their careers really get going. With so much of our take-home pay earmarked for debt service, no wonder housing isn’t a priority, or affordable, for millennials (or the Teppers).

Of course, this kind of talk scares our parents (and rich people), who own bonds and other assets designed to preserve wealth instead of create it. Having already endured years of low interest rates, they really don’t want their bond portfolio to be hit by an inflation jump.

To which I say, tough. Many boomers entered the job market as the economy was expanding and college was affordable. Their children did not.

Luke has this one toy that he loves. It’s a sort-of picture book for infants consisting of a crinkly material, and he loves nothing more than smashing the thing between his hands and feet. In 17 years, he’ll want a car—and then four years of college.

I realize that the costs of these things will rise—prices always rise. It would just be nice if our salaries rose enough to pay for them.

Taylor Tepper is a reporter at Money. His column on being a new dad, a millennial, and (pretty) broke appears weekly. More First-Time Dad:

- What Adam Smith Taught Me About Child Care

- Why a Maid is a Better Investment than a Divorce Lawyer

- Why You Should Get Up for Your Desk and Go Home