Mortgage Rates Just Spiked. Is It Still a Good Time to Refinance?

- The Swag Must Go On: Big Companies Are Rushing to Slap Their Logos on Face Masks and Hand Sanitizer

- How to Get Back on Track After Tapping Into Your 401(k) in a Financial Emergency

- A Mistake Caused Credit Scores to Drop for Tons of Student Loan Borrowers. Here's How to Fix Yours

- It's Not Just a $1,200 Check. Here Are All the Other Ways You Can Benefit From the Coronavirus Stimulus Package

- Life Insurance Prices Will Likely Rise Because of the Pandemic. Here's Everything to Know About Buying a Policy Right Now

For proof that the coronavirus pandemic is wreaking havoc on economic as well as public health institutions, look no further than the mortgage market: mortgage rates have been bouncing around at record or near-record low levels for a number of weeks now, with the benchmark 30-year fixed mortgage rate shooting up by roughly 30 basis points (that’s 0.3 of a percentage point) in the space of a week. “It’s the most significant jump in history,” says Thomas Forker, senior vice president at Bryn Mawr Trust.

The average rate for a 30-year mortgage was 2.78% for the week of July 22. But is it still worth it to refinance? Many homeowners seem to think so. According to the Mortgage Bankers Association (MBA), the Mortgage Refinance Index refinance loans made up 60% of all mortgage loans.

In fact, according to Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting, the organization expects to see an increase in refinance activity throughout 2020 despite the volatility in interest rates. “They might be volatile, but there are still pockets or weeks where rates have fallen and our expectation is for rates to stay low for the rest of the year,” he says. “If we see rates stay close to the current level then our forecast for that 30% growth in 2020 is looking pretty good.”

The only factor that may slow down the refinance market is the lenders’ ability to process all the applications in a timely fashion. Kan points out that both borrowers and lenders have had to adapt to a new way of processing loan applications without the benefit of in-person meetings. As lenders go working through these wrinkles in the process, lending should continue. “The benefits to refinancing extend to more than just the borrower’s finances,” said Kan. “It’s beneficial to the industry and to the broader economy. There’s definitely a lot of incentive to keep refis going.”

But according to some experts, now may not be the best time to refinance.

Is Now the Right Time to Refinance Your Mortgage?

First, some background: The sudden spike is attributable to two factors. One is simply more demand. With rates this low, homeowners thinking about refinancing have a lot of company.

“The Federal Reserve has cut rates twice in March. But spreads have widened between Federal Fund rates and 30-year fixed mortgage rates mostly because lenders are adjusting to higher volume, for refinancing as well as for new mortgage originations,” says Ken Leon, director of equity research at research firm CFRA.

Although it might be funny to think about “surge pricing” in the mortgage market, the relationship between supply and demand in the ride-share business isn’t fundamentally all that different. “Lenders were getting so busy they just couldn’t take any more business,” says Forker.

The other, overriding factor is the sheer disarray into which the COVID-19 pandemic has thrown nearly all of the world’s markets. The unprecedented uncertainty has thrown off the usual equation bond traders rely on to assess risk — and bond market activity is the foundation on which the mortgage market is built.

In the face of such extreme volatility, Forker suggests that homeowners who haven’t already locked in a rate might be better off being patient — for a bit, at least. “The interest rates have swung so far out, it’s more of a wait and see,” he says. “Stand down and keep your eye on the market.”

The Federal Reserve has been pouring resources into ensuring that markets remain liquid — that is, making sure that volatility doesn’t artificially distort the supply-and-demand balance.

“These rates should come back if markets return to normal,” Forker says — and they will, he asserts. Mortgages are important enough that the central bank will make sure of that. “We’ve been at or better than where we are now for the better of the last two years. So I would still recommend letting this settle down.”

Four Indications It’s Time to Consider Refinancing - Or Not

Refinancing a mortgage is a big step - as big as applying for a mortgage in the first place. It also takes just as much time and effort, so it’s a decision you shouldn’t take lightly. Your first step should always be to establish a goal - what you want to accomplish by refinancing, whether it be a lower monthly payment, a shorter loan term, or taking equity out of your home. You can find more detailed information on mortgage refinancing in our Best Mortgage Refinance of 2021. There are, however, certain factors that can help you determine whether or not it’s the right time to refinance.

Lower Interest Rates

The primary and best reason homeowners decide to refinance is to save money on their mortgage by reducing their monthly payments. In general, if your current interest rate is 1% higher than the average interest rates on the market, it’s time to consider refinancing.

With interest rates being so low now because of the effects of COVID-19 on the economy and bond markets, most experts will tell you that if your current interest rate is over 4.0%, you should definitely consider refinancing. A reduction in interest of even 0.50% can translate into significant savings over the life of your loan.

While the idea of lower interest rates translating into automatic savings sounds good, make sure you run all the numbers before taking this step. Consider that there are other costs involved in a refinance, such as closing costs and application, appraisal and title fees. Then calculate your break-even point. This is the amount of time that it will take for you to recover the money you spent in refinance costs and start to actually save money, and should ideally be within two years of your refinance date. If you plan on living in your home for a long period of time, you’ll be saving money in the long run. If you’re planning on selling your home before the break-even point, however, you’ll actually be losing money even though you have a lower monthly payment.

Remember to also take into consideration that by refinancing you may be extending the overall amount of time you’ll be paying off your mortgage. For example, if you are 10 years into your mortgage and refinance for another 30 years, you’ll be paying a mortgage for 40 years total, which means that in the long run, even though you may have lowered your monthly payments, you may be paying more in interest. If you refinance early in your current mortgage the difference may be small, but if you’re well into the original loan term, consider refinancing for a shorter period of time, like 15 or 20 years. The monthly payments may be slightly higher, but you’ll save on interest over time.

Increased Equity In Your Home

If you purchased your home with less than a 20% down payment, your monthly mortgage payments include Private Mortgage Insurance (PMI). If you’ve built up enough equity in your home to cover that 20%, you can eliminate PMI and reduce your monthly payment even further.

Increased equity also means you can consider a cash out refinance if you have to make emergency repairs on your home or have unexpected medical costs that you don’t have the means of paying for upfront. However, if you’re considering a cash-out refinance to pay off higher interest debt such as credit cards or personal loans, or to consolidate a number of different debts, be very careful. You may just be exchanging one form of debt for another or even adding onto it, especially if you continue to accumulate high interest debt after you’ve done a cash-out refinance. Make sure you won’t increase credit card balances or other high interest debt again once you’ve done the refinance, or you’ll just fall into a debt cycle it may be hard to break free from.

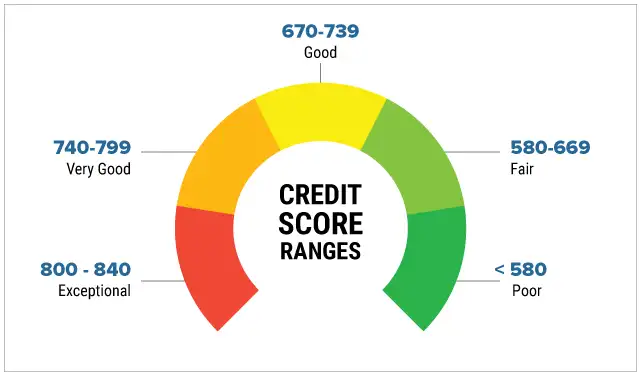

Your Credit Score Improved

Your credit score is an important factor in determining the interest rate you qualify for. If your score has improved since the time you first took out your mortgage, you may qualify for a much lower interest rate. Those who have the highest scores will get the best rates.

Your first step before considering a refinance should always be to check your credit score. FICO scores will range from Poor to Exceptional, and will take things such as your payment history, how much you owe, the length of your credit history, what kind of credit you have and new credit you’ve applied for into consideration.

Once you’ve checked your score, see if there are ways to improve it. Pay down debts like credit cards and make sure you make payments on time. Get a copy of your credit report and check it for accuracy. If you find errors, take steps to remove them from your report. Some credit reporting agencies offer to increase your score instantly, usually by including your payment history of utilities, so if you’ve been paying your electricity, gas and water bills on time, this could provide an automatic boost.

If your score doesn’t qualify you for a lower interest rate at the moment, checking your credit report will at least give you an idea of what you need to do to improve that score. You can also consider prepaying your mortgage. If you can pay more each month towards the principal of your loan, you are effectively reducing the term of your loan and saving money in the long run -- as long as there are no prepayment penalties attached to your mortgage.

You Have an Adjustable Rate Mortgage (ARM) and Interest Rates Are Rising

If you have an ARM and interest rates are starting to rise, you should look into converting it to a fixed rate mortgage so you can lock in a low rate, especially if you’re planning on staying in your home for the length of your loan.

ARMs will generally have a lower interest rate than fixed rate mortgages, which can make them very attractive, but only for a set number of years. After that time period where the rate is fixed, interest rates will either increase or decrease according to market conditions. You’re basically taking a gamble on future interest rates, so locking in a fixed rate when indications are that interest rates will rise can help reduce your monthly payments.

Although it seems like converting an ARM to a fixed rate mortgage would be the most logical step, sometimes converting a fixed rate mortgage to an ARM could make financial sense. If interest rates are falling and you’re not planning on staying in the home beyond the period where the interest rate is fixed, you could take advantage of the lower interest rates an ARM provides.

Find Low Refinance Rates

If you do decide to take advantage of today’s low rates, we recommend that you shop around and compare interest rates and loan terms from different lenders to find the deal that best suits your circumstances. We’ve reviewed some of the top refinance lenders to help you get started.

Quicken Loans/Rocket Mortgage

Quicken Loans is the largest originator of primary mortgages in the country and is one of the top mortgage refinancers as well. Its online offshoot, Rocket Mortgage, is not only a top online lender but is also quickly becoming the face of Quicken. Applying online for any Quicken financial product, including mortgage refinancing, is done through the Rocket platform.

You’ll have quite a few refinance options with Quicken/Rocket. The most popular product offered is a conventional 30 year fixed rate loan. However, you can also apply for shorter loan terms if your goal is to pay your mortgage off faster. With YOURgage you can choose the term of your loan, from a minimum of eight years up to a maximum of 30 years. You can also refinance VA loans and FHA loans, or do a cash-out refinance if you’ve built up enough equity in your home.

QuickenLoans/Rocket Mortgage is known for its low rates and customer service. As we mentioned, you can apply online at Rocket Mortgage or by phone with one of Quickens’ loan experts. You can usually get an initial estimate of how much you can save with a refinance in a matter of minutes.

Freedom Mortgage

Freedom Mortgage will offer conventional loan refinances but it specializes in government-backed loans, including FHA, USDA, and VA loans. Because of its experience in managing these types of refinances, this lender can help you navigate the intricacies of applying for government loans.

For FHA and VA refinances Freedom Mortgage offers what they call the Streamline Refinance, which requires less paperwork than traditional refinances. These streamlined loans, however, can only be used to replace an existing loan under a particular government program - a VA refinance can only be used for an existing VA loan. The same applies to FHA and USDA loans.

Refinance options include fixed-rate and adjustable-rate mortgages, and loan terms can be either 15 or 30 years. The interest rate will vary according to a number of factors. For conventional refinances, Freedom Mortgage requires a credit score of 620 or higher, a debt-to-income (DTI) ratio of no more than 45%, proof of income, and enough cash on hand to cover closing and additional costs. For government-backed loans, credit score requirements can be as low as 540 (depending on the program), with higher DTI’s, no need for cash on hand for closing and other costs, and generally lower interest rates than conventional loans.

Figure

Figure is an online lender that offers only three products - home equity lines of credit, student loan refinances, and mortgage loan refinances. According to the lender, those choosing to refinance through Figure can receive approval in as little as 10 minutes, with the actual closing on the loan occurring within 10 days in most cases.

The company uses blockchain to record, share, and exchange all the data for your loan, ensuring the accuracy and seamless review of your application, which saves time and allows Figure to process your loan much faster than a traditional lender. The online application process is easy and you can get a quote in just a few minutes.

Figure specializes in cash-out refinances, allowing you to refinance up to 80% of your home’s value, with up to a maximum of $500,000 available in cash back. The lender does limit its refinance options to single-family homes and townhouses, however.

PennyMac

Rather than specializing in just one or two products, PennyMac specializes in all types of mortgage refinancing, including conventional fixed and adjustable-rate, VA, FHA, USDA, cash-out, and Jumbo loans.

With the Flex Term mortgage, the term of your refinance loan is flexible. You can set your own pay-off date to coincide with your retirement, for example, or any other date you choose. This option is available for all loan types except USDA and Jumbo loans.

You can get an initial quote just by entering some basic information on the website. The application process itself with PennyMac is easily accomplished online and you can upload documents and keep track of your application through the Mortgage Access Center.

LendingTree

Although not a refinance lender per se, LendingTree is a marketplace that can help you compare rates and terms from different lenders in your area, making the comparison shopping part of refinancing easier.

Getting quotes from different lenders is easily done by entering the area where you live, the value of your home, the remaining balance on your current mortgage, and your credit score. The application is just as easily done online, or you can speak with a loan specialist by phone.

LendingTree also provides tools to help you decide which refinance options are best, such as their refinance payment calculator, which gives you an idea of your new monthly payment, and the refinance breakeven calculator, which tells you when the savings from your refinance will cover the cost of the refinance. If it’s the first time you’re considering refinancing, LendingTree also provides a number of educational articles on the topic and how to determine when it’s the best time to refinance.

Refinancing Now Is Still Your Best Option

Depending on the rate you’re currently paying, Leon argues that waiting for the mortgage market to give back a few fractions of a percentage point might not make economic sense. “Given that the Federal Reserve has essentially shot its bazooka, you would absolutely want to look at refinancing, especially if you’re going to save significantly,” he says.

“Rates are still much lower than 15 months ago when we were at 5%,” he points out. “For the next three to six months, it’s going to be a great time to refinance.”

More from Money:

Coronavirus Continues to Tank the Stock Market. Here's Why — and What To Do About It

Mortgage Rates Are Near Record Lows. Here's How to Figure Out If You Should Refinance