How to Avoid Paying for Your Kids Forever

- Wealthy People Are Giving Away More of Their Money

- New Metric: You Reach Adulthood When the Bills Are in Your Name

- The Classroom Exercise That Turned Fourth-Graders Into Smarter Money Managers

- How Micro-Investing Can Build a Giant Nest Egg

- It Just Got Easier to Cut College Costs with a 529 Savings Plan

This may seem like your fate, given the tough economy for young adults, but you don’t have to write a blank check. These strategies will help you launch your kids on the path to independence without risking your own financial security.

Steve and Darlene Goldstein could be on a crash course to a difficult reckoning. With a six-figure annual income, they shouldn’t have a worry in the world. But Darlene recently retired as a substitute schoolteacher, and Steve, 68, a program manager for a national security technology company in Las Vegas, wants to join her. Only he can’t—not while the couple is still supporting their daughter, Abby, 25, a yoga instructor who lives more than 1,200 miles away. To assist Abby with rent, utilities, and other living expenses, the Goldsteins have forgone home improvements, and Steve just pushed his retirement date out two more years. While he feels fortunate to be able to help, the financial drain is a real concern. He and Darlene know the outflow must stop. The sticking point, says Steve: “My wife and I don’t agree on the timeline.”

Like millions of parents with adult children who in one way or another remain on the family ticket, the Goldsteins are trapped between wanting to soften their daughter’s entry into the real world and making their own financial security the top priority. In what feels like a blink, an era of extended child dependency has taken root across the country. Psychologists have a name for it: emerging adulthood, a new and possibly permanent life phase squeezed between the teen years and, say, 28 or 30. Who cares what you call it, though? Most parents with one eye on retirement just want to know: Will we be paying for our kids forever?

Fortunately, the answer in most cases is no. Still, if you are wearying of the endless dry-cleaning, cellphone, and insurance bills that your adult children are sending your way and you want to accelerate their launch, you may have to offer tough love instead of hard cash.

For now, though, few parents seem willing to push back with any vigor. Two-thirds of people over 50 have financially supported a child 21 or older in the past five years, Bank of America Merrill Lynch found last year. “Family dynamics are evolving,” says David Tyrie, head of retirement and personal-wealth solutions at Merrill. “Adults are living longer, people are retiring later, and millennials are making life choices vastly different than their parents did.”

Studying the same phenomenon, a 2013 Pew Research Center report shows even more startling figures: Among adults ages 40 to 59 with at least one grown child, 73% said they’d helped support an adult son or daughter in the prior year. Half of those middle-aged parents said they were their grown child’s primary means of support—in some cases because their offspring were still in school but also, more than a third said, for reasons other than education. In another study, Pew found that nearly a quarter of 25- to 34-year-olds are now living with parents or grandparents, up from 11% in 1980. “It’s not at the margins,” says Ken Dychtwald, CEO of Age Wave, a consultant on the aging population. “It’s kind of everybody.”

The statistics raise many questions. Not least: Why are so many young adults failing to launch? The financial crisis and weak recovery, and the overhang of soaring student loans, explain a lot. Only about half of adults ages 23 to 26 and at least one year out of college have a full-time job, according to a five-year longitudinal study from the University of Arizona. Meanwhile, outstanding student debt has risen threefold, to $1.2 trillion over the past decade, according to the Consumer Financial Protection Bureau.

As a result, there is no longer a stigma to living at home while you pay down your debts and explore your passions. “We’re seeing kids choose to live at home for a while to build an emergency fund and get a cushion for when they are on their own,” says Alexa von Tobel, CEO of the financial website LearnVest.com. To some, that may look like mooching. Yet building savings while looking for the right career can improve the odds of kids remaining independent when they finally move out.

In some ways this is as much a demographic story as it is a financial one. Little more than a century ago there was no such thing as adolescence. You were a child to 13, and then you went to work. As human life stretched out, we made room for the teen years, when kids could experiment and go to school longer. Now we’re expanding that life phase once again to where twentysomethings can go to graduate school or try a few personal pursuits before settling into a long career. You could argue we institutionalized this life phase in 2010, when the Affordable Care Act required employers to cover children’s health care to age 26.

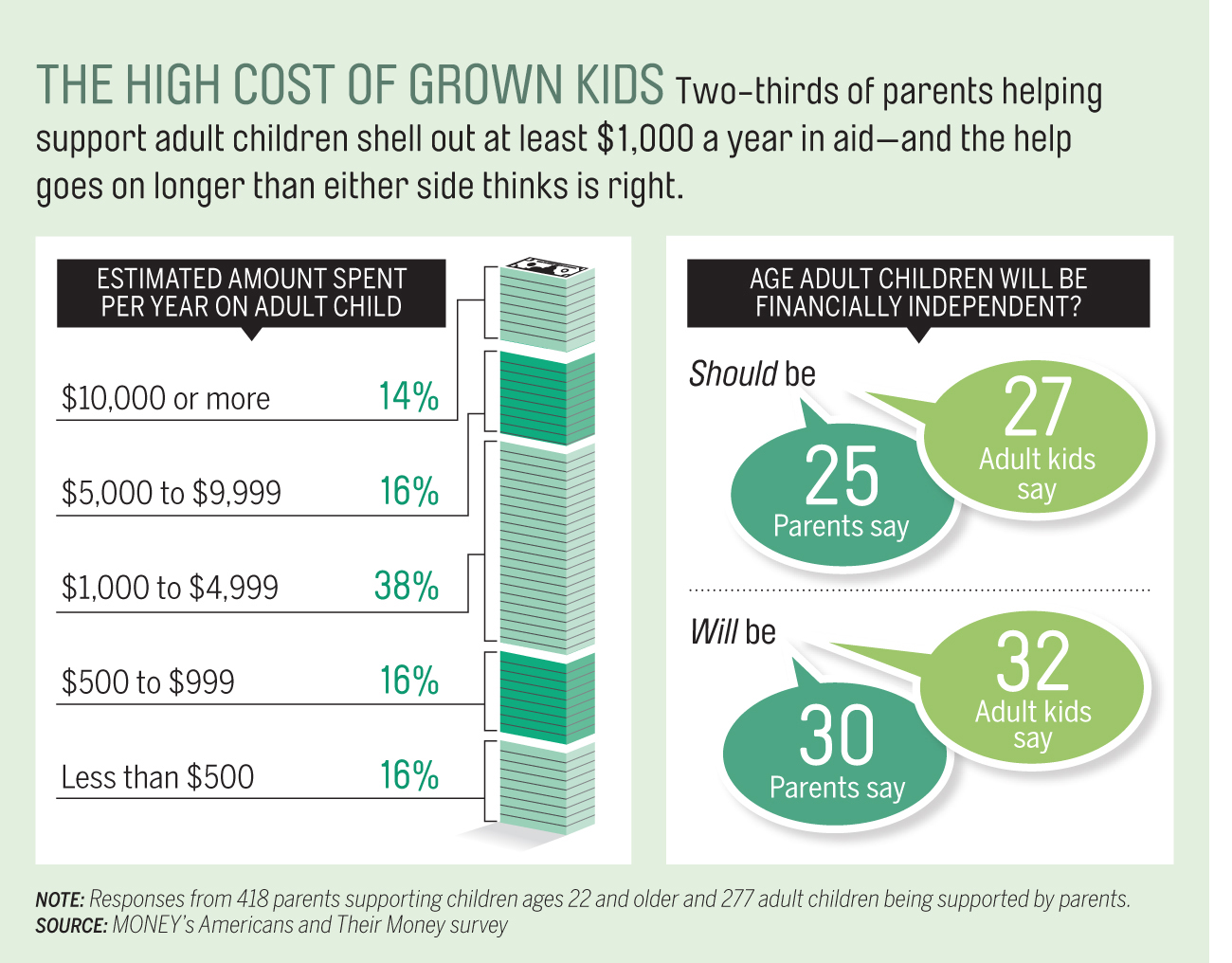

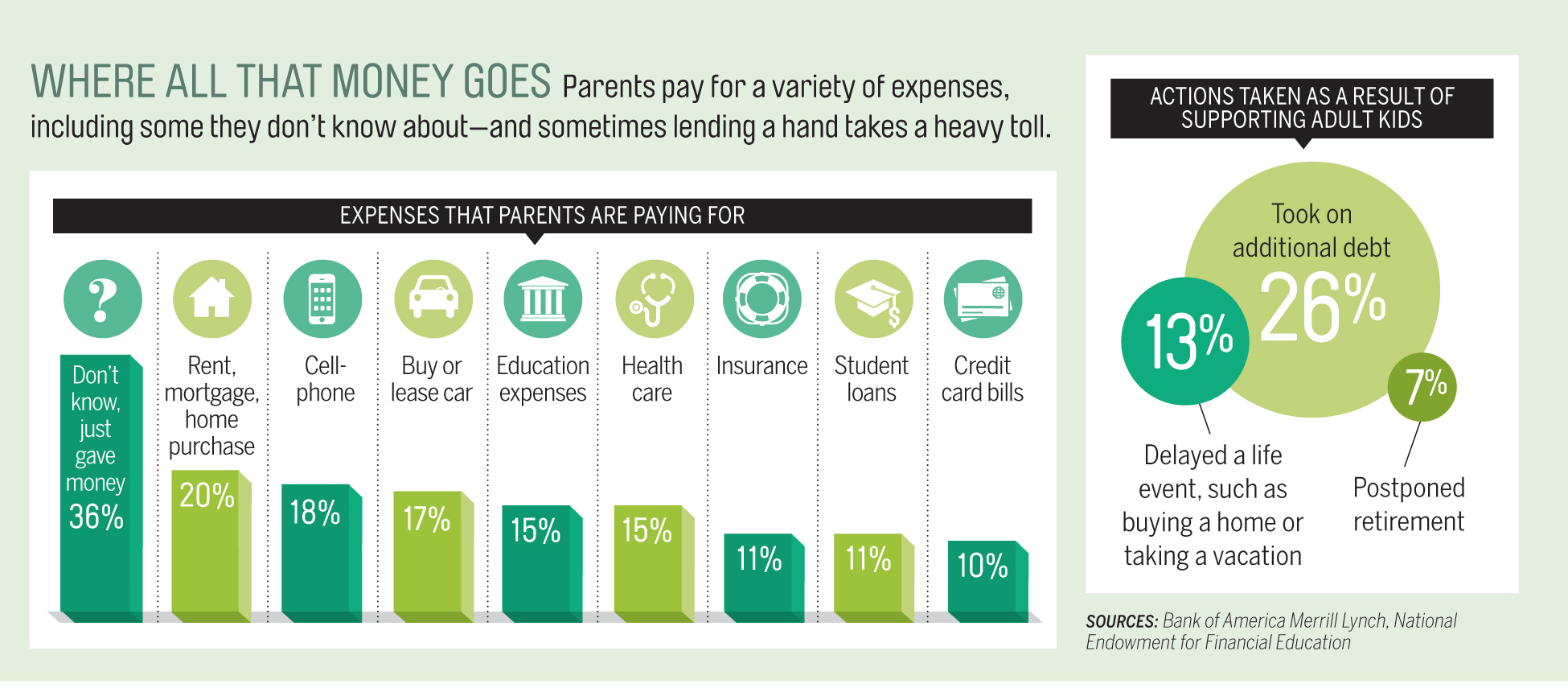

Whatever the reasons, the fact is that these young adults are costing their parents a lot of money. A Money survey earlier this year found that 30% of parents helping to support grown children spend at least $5,000 a year on their kids. Most are willing to make big sacrifices to do so, if necessary. Six in 10 parents in the Merrill Lynch study said they are willing to work longer, 40% to go back to work, and 36% to live with less if that’s what it takes to help their kids. Meanwhile, the National Endowment for Financial Education found that more than a quarter of helping parents say they have taken on additional debt as a result (see the graphic on page 70). And many more parents may have to settle for a less comfortable retirement than they had planned.

It’s also unclear what effect this extended support will have on the long-term well-being of the kids. Do grown children really benefit from another five to 10 years of nurturing? Or are we coddling them beyond reason, creating a generation of lifelong dependents?

What you want is to strike a balance—to provide just enough support to help set your child up to be happy, productive, and self-sufficient without undermining yourself. The following moves point the way.

[time-anchor title="1. Foster Their Independence"]

The fundamental question to ask yourself when deciding whether to give or continue assistance to your adult child, suggest family wealth consultants Eileen and Jon Gallo, co-authors of The Financially Independent Parent: Will providing money help your son or daughter become self-sufficient or instead prolong his or her dependence?

That’s exactly the kind of thinking that prompted Michael Golden, 67, of Clovis, Calif., and his late wife to give their 30-year-old daughter $26,000 toward the down payment on her first home two years ago. And Golden, a retired state criminal investigator, plans to do the same for his son, 33. Golden has enough income from his pension to get by and has long planned to provide this help from savings. “The kids will eventually inherit it anyway,” he says. “Why not give it to them when they can really use it?” His parents did the same for him, and he believes early homeownership gave him an invaluable leg up to building financial security. “Both kids have been saving the best they can,” Golden says, “but it’s hard with entry-level jobs. I know, because my wife and I went through it too.”

Golden is doing at least a couple of things right. First, he has run the numbers and is confident the gifts won’t set back his own plans. Second, he has chosen to bestow a one-time bounty meant to jump-start a fruitful life. Similar types of financial support include anything you might call a startup cost—a security deposit, a new wardrobe for work, furniture, a reliable (not necessarily new) car, a finite amount of small-business seed money, or picking up the cost of relocating for a job—in other words, payments that will help your children help themselves.

Steve Goldstein, for instance, recently picked up the $5,000 tab for daughter Abby’s move from Chicago to Dallas, where she’s landed a job as the assistant manager of a yoga studio. The position pays $33,000 a year—a big jump from the $14,000 she made last year as an instructor. For the first time since Abby graduated from college in 2011, Steve and his wife will no longer be paying their daughter’s rent, though they’ll continue to cover groceries, insurance, and her cellphone bill. “Do I feel guilty that my father isn’t retiring when he expected to because he’s supporting me? Yes, of course,” Abby says. “But the more settled I get in my new job, the more they can bow out.”

Continuing education and vocational training also come under the heading of expenses the Gallos believe are worth chipping in for—if you can afford it or the sacrifices you make to pay them don’t seriously undermine your long-term security. They point out that many young people change focus several times before settling on a career. Helping them figure out what they really want to do and get trained for it can be money well spent.

Consider Tatung Chow, 54, a software engineer in San Jose, who had just finished paying for his daughter’s undergraduate degree in visual arts when she decided she wanted to be a fashion designer. Sylvia is now pursuing an MFA at a fashion design school in San Francisco, and Chow and his wife, a sales administrator, are looking at three more years of tuition and living expenses that will run $90,000 to $120,000. “Since we’re spending part of our retirement money for her education, my wife and I need to work an extra year each,” Chow says. Still, he has no qualms. “I don’t want my daughter to look back 40 years from now and have this regret that she didn’t get to see if she could be a designer,” he says. “We are doing whatever we can to help her fulfill her dream.”

[time-anchor title="Set Clear Parameters"]

The majority of parents shell out a lot less than the Goldsteins and Chows. According to the Money survey earlier this year, parents who are helping an adult child most commonly spend $1,000 to $5,000 a year, often for everyday expenses such as cellphones, utilities, Internet and cable bills, and car and health insurance. The Merrill Lynch study found a similar breakdown, except for this top answer: More than a third of the parents polled said they didn’t know what expense they were covering; they just gave money.

Ongoing support for living expenses isn’t necessarily a bad thing, but, says Ted Beck, CEO of NEFE, you should “understand what you are paying for and exactly how it will help.” Reserve your assistance primarily or exclusively for needs, not wants—let Junior sign up at a fancy gym, buy the latest tech gadget, or go away for the weekend with friends on his own dime or not at all. Be frank in outlining the limits of your support, says Beck, so that your child is motivated to work for a better lifestyle.

You’ll feel better about lending a hand if you know your kid is working hard to be self-sufficient and that there are solid reasons that he can’t fly solo yet. In Jon Boisselle’s case, for instance, the obstacle standing between him and financial independence is the $400 a month he pays toward his student debt. Boisselle, 25, has a degree in biology and a full-time customer-service job for a biotech company in Portland, Maine. He mostly scrapes by on his salary, but relies on his mom and dad for help with heating, vet, and medical bills and one-time expenses like car registration.

To save money, Boisselle also does his laundry at his parents’ house, and his mom always sends him home with bags of groceries filled with frozen meat and fresh produce. “I feel irresponsible taking money from my parents,” he says, but his student debt makes it impossible to break free yet. “They’re completely supportive, but I know they’ve sacrificed a lot for me.”

[time-anchor title="2. Provide Tough Love, If Needed"]

Sometimes it takes stronger action to push an adult child toward independence. Maureen Kolb, an executive coach who lives in Milwaukee and is part of a blended family with six adult children, knew enough was enough three years ago when the family was at the college graduation of her son, Danny Kerns, and noticed his name wasn’t in the program. He’d fallen three credits short and had to stay on campus over the summer, at family expense, to finish. He didn’t complete the coursework then either, and moved home to take yet another class at a local college in the fall. “He was sitting around, taking one class, and had nothing else to do while I was paying his bills,” recalls Kolb, 53. “I told him to get out and come back when he had a job.”

A few days later Danny came home in a blue Best Buy uniform. “I put her through so much,” he says. “I see that now.” Danny finished school that semester and now has a good job in business-to-business sales, which his Best Buy experience helped him land. “I grew up a lot between 23 and 25,” he says. Adds Kolb: “So much of this you don’t even realize until you are staring at it. I had to get angry before I did something.”

Ask yourself: How hard is your child looking for work or applying herself at the job she has? Opportunities and promotions don’t just happen, and the adult child who isn’t held accountable may never step up her game, says psychologist Jeffrey Bernstein, author of 10 Days to a Less Defiant Child. Plus, allowing adult children to live beyond their means thanks to Mom and Dad’s blank check inadvertently sends the wrong signal, Bernstein warns: that they aren’t able to make it on their own and you will always take care of them.

[time-anchor title="3. Get Something in Return"]

The upside to extended support: Especially when kids are living at home, many parents enjoy the extra time together and develop a closer connection, Pew found. And those adult children often pitch in: The NEFE study found that 42% contribute in nonfinancial ways such as cooking and cleaning, while 75% contribute with dollars, commonly by chipping in for rent or the mortgage, groceries, utilities, and gas.

With kids who are living at home, it’s especially important to insist on contributions to the household if they haven’t stepped up. The message is simple and will serve them well: You don’t get something for nothing.

So charge rent—even if all you do is set the cash aside for them so that they have a little savings when they finally launch, suggests von Tobel at LearnVest. Or invest the money in a Roth IRA in their name. And it’s only fair that they do their share of the laundry, cleaning, and shopping.

Your children don’t have to live at home for you to gently suggest that they make some kind of contribution to the family to “earn” your financial help. For instance, Courtney Gibson, 24, who moved to New York City from Orlando two years ago, relies on her family to pay for her cellphone, health insurance, and utilities—about $500 a month. Otherwise, Courtney, a sales associate at an upscale department store, couldn’t afford her dream of living in the city. Her parents are supportive, but mom Lori, 53, who owns a boutique and a wine bar, says, “I try to make her work for it.” Courtney maintains the websites for her mother’s businesses, sends out promotional emails to customers, and manages social media. Still, Courtney says, “it’s embarrassing to be getting help from my parents when I’m 24 with a full-time job, but my mom tells me not to feel bad.” Says Lori: “Everyone needs help when they’re starting out.”

[time-anchor title="4. Give According to Your Means"]

One thing’s for sure: As much as you love your kids, you should think hard before sending them money that takes a meaningful toll on your own lifestyle—and it’s unfair for the kids to expect that from you, says financial planner Stephen Tally, CEO of the BFT Financial Group in Fort Worth. They are young; they have options. Borrowing isn’t perfect, but at least they have time to pay it back. On the other hand, you have only so many years left, and you have worked hard to be able to enjoy them.

Sometimes Tally says he comes across clients who plan on helping their kids financially to the day they die—until he lays out for them what that might look like. Tally does a quick net-worth calculation, then translates that into a monthly income stream based on the purchase of an immediate annuity. He adds any income from a pension and Social Security. When he puts that figure next to the clients’ expected expenses, they are usually ready to make some changes.

Consider an affluent parent offering grown kids annual support of $10,000. It may not seem like much when you take it apart: maybe $300 a month for rent, $50 a month for a cellphone, $150 for insurance, $200 to $250 for a car lease or loan, and maybe $100 toward college debt. Say you do this for five years. Had you banked that $50,000 instead and earned a 7% annual rate of return from ages 52 to 67, you would have an additional $121,045. Even at today’s low rates, that’s enough to buy about $720 of monthly income guaranteed for life. If you rolled that savings into a deferred fixed longevity annuity, it would buy about $3,000 of guaranteed monthly income beginning at age 85—a cushion that might keep you from ever needing to worry about outliving your savings.

“Psychologically it’s really hard to tell someone if they stop paying for their kids everything will be okay,” says Tally. “But they don’t see what the amounts may look like 15 years from now. You have to show them.”

[time-anchor title="5. Come Up With an Exit Strategy"]

Once you have decided the gravy train must stop, clear communication with your children is key. Most kids don’t realize how much the support they receive is costing you because, well, you’ve probably never told them. Here are some guidelines for at long last cutting the financial cord:

Be honest about the impact. “Let them know there is no trust fund,” says Beck. “You are making real tradeoffs to support them. That usually accelerates the time frame.”

Abby Goldstein, for instance, does not realize the extent of her parents’ support. “I don’t have any idea,” she says. “You have to ask my dad.” Steve, on the other hand, has the amounts down pat, ranging from a high of $46,400 in 2012 to a projected

$23,600 this year; next year, he’s hoping that will drop to $12,000. By continuing to work, he’s managed to cover Abby’s needs and his and his wife’s (they also give some help to an older son). Steve says, “The catalytic event will be my retirement.” Those are facts his daughter should know.

Create a concrete plan to end aid. Kids and parents often have different ideas about when support should stop. In the Money poll, parents helping adult children generally believed kids should be independent by age 25, but acknowledged that in their own situation, 30 was more likely. Young adults put those ages at 27 and 32, respectively.

Don’t make it a guessing game. First, assess the monthly support you’re providing now, then decide on a time frame for tapering off (say, three to six months from now), and map out the path to zero outlay in perhaps a year or two, says Lisa Heffernan, who blogs about adult children at grownandflown.com. Then—and this, of course, is the hard part—stick to it. “The things they ask for in many cases are things that we did without, and it did us no disservice,” Heffernan says.

Stay on as their financial coach. One of the benefits of supporting adult kids is that parents and offspring often end up talking more about money than might otherwise be the case—what it takes to run a household, how to stay out of debt, how to advance in your career. Keep those discussions going even after you’ve shut down the Bank of Mom & Dad. You might also treat them to a session with a financial adviser or introduce them to tools that can help them manage their money at sites like mint.com, budgettracker.com, budgetpulse.com, and learnvest.com. Notes Beck: “Parents are still the No. 1 source of information about money.”

Steve Goldstein plans on having such a conversation with his daughter before his retirement. He’s also given both his kids personal finance books and offered to send them to a money-management course—though neither has taken him up on it yet. “If I don’t work with my daughter to help her move forward to a career rather than a job, then even with the dollars I’m giving her, I’m not parenting successfully,” he says. “I need to be accountable for raising a person who contributes to society.”

Additional reporting by Kerri Anne Renzulli.