60% of Americans Say Their Stimulus Check Isn't Enough, New Money Poll Finds

- Here Are Every State's Unemployment Rules for Work Search and Waiting Periods

- Most Job Search Requirements for Unemployment Benefits Are Waived. So Why Do State Websites Say Otherwise?

- Did You Apply for a Small Business Loan? Here's What to Know About the Latest Round of PPP Funding

- What Happens if Your Stimulus Check Goes to the Wrong Bank Account?

- True or False: You Won't Get a Stimulus Check if You Owe Money to the IRS

More than half of Americans say their stimulus checks won't be enough to tide them over financially during the coronavirus crisis, according to a recent Money/Morning Consult poll.

People across the country have been refreshing online bank account statements and triple checking mailboxes as they wait on a stimulus check that many expect will still fall short of their needs. Sixty percent of those surveyed said the stimulus check is going to make a difference for them — just not for as long as they need it to. Morning Consult polled the 2,200 respondents on behalf of Money earlier this week.

Congress authorized the one-time stimulus payments in late March to ease the financial strain caused by the pandemic. The first wave of checks, which range up to $1,200 per individual based on income plus an additional $500 per dependent, started hitting bank accounts last week. But will they be enough to cover costs?

In places like New York City and San Francisco, the maximum stimulus check will hardly be enough for one month’s rent. And yet most respondents say they plan on using this extra cash for basic necessities like bills (35%), groceries (23%), and rent or mortgage payments (16%). The respondents, half of whom categorize themselves as Millennials (24 to 39) or Generation X (40 to 55), work primarily in the private sector (29%). Another fifth are retired, 13% are unemployed, and 9% are self-employed.

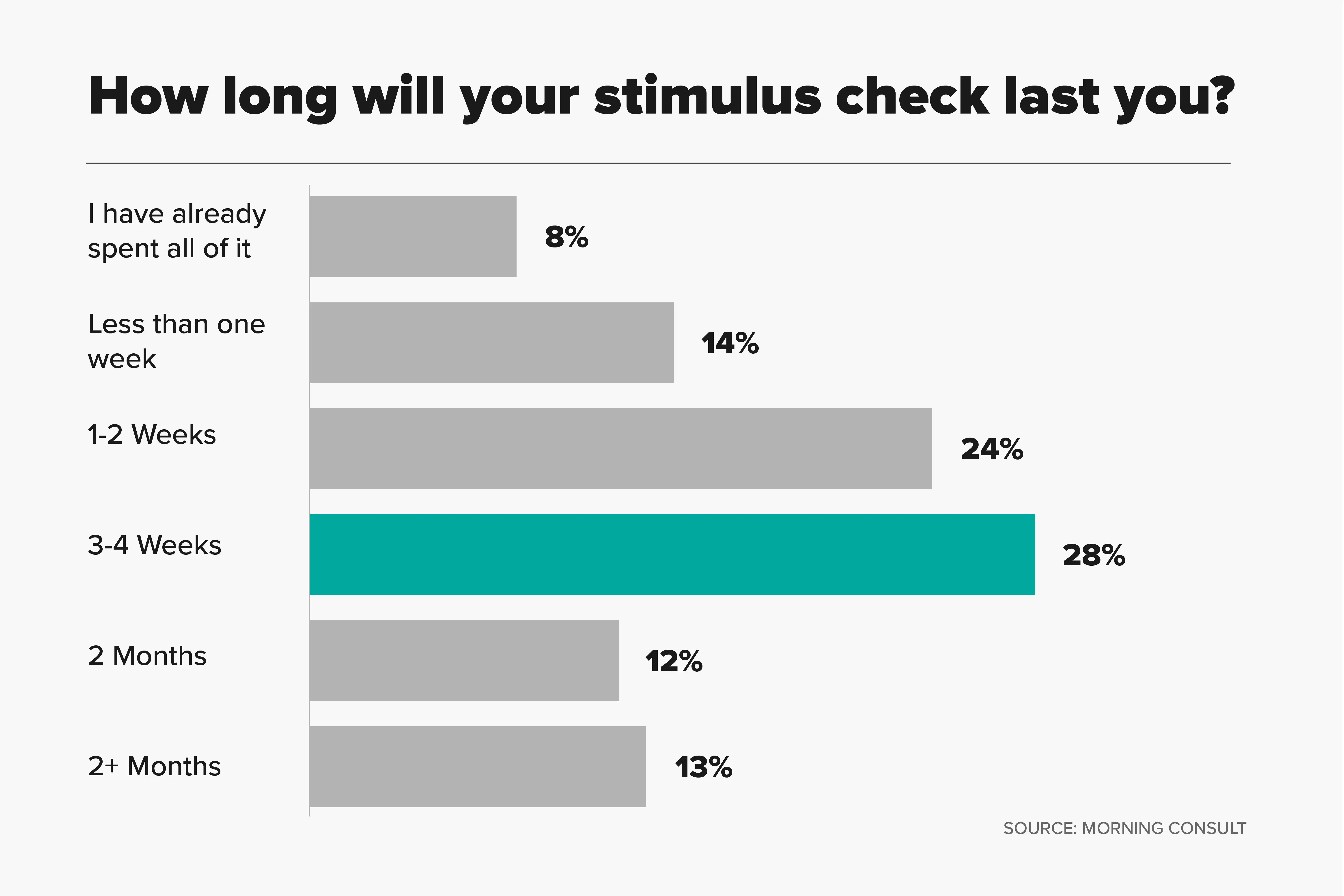

It's hard to say for sure how long Americans will need this money to last, since financial burdens will likely last past the shutdown, and the shutdown itself will end at different times depending on where you are. This week, for example, Georgia became the first state to announce it would reopen, but in other states — like New York, where the shutdown was just extended to May 15 — residents are looking at another three to four weeks of self-isolation at least.

That's about the length of time a majority of respondents said the stimulus check will cover them as it currently is, based on what they know about their current spending, bills, and income. Another half said it would be shorter than that, with about 8% claiming they already spent it all.

While the stimulus check was announced as a one-time payment, plenty of lawmakers have recognized that it falls short, and that additional (possibly monthly) payments might be necessary.

"If you live in New York City, $1,200 will get you through a week or two," said Rob Leiphart, a certified financial planner and vice president of financial planning at RB Capital Management. But Leiphart says your best bet is to stretch that check as far as possible by taking advantage of resources and leniencies during these tough times.

He suggests asking your landlord, your bank, your credit card company and your car insurance company if you can get some leeway on payments. And at the very least, you can become a more careful consumer by doing things like going through your pantry and taking inventory before you leave the house for groceries.

"If you talk about the stimulus alone in a vacuum, it doesn't have that much power," said Leiphart. "The strength is in the compounding of various programs." That certainly beats waiting for another check that may or may not come through.

For now, people who have their basic necessities met are advised to take a more proactive approach with their stimulus check to shore up their finances against a possible, prolonged recession. According to our survey, a lot of Americans are doing just that: About a third of respondents said they’re putting at least part of their stimulus money towards savings (32%) while some are using it to pay back debt (17%). Only a minuscule 3% of respondents said they’d spend the money on superfluous luxuries.

More from Money:

Here's Why You Can't Call the IRS About Your Stimulus Check

Best Balance Transfer Cards of 2020

The CARES Act Made It Easier to Withdraw From Your 401(k). Here's What to Know Before You Do