Where to Find Bargains in the Biotech Bust

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

For much of this bull market, biotechnology stocks were like anabolic steroids for your portfolio. They soared nearly 600% from March 2009 to last summer—almost three times the gains for the broad market. More recently, though, this risky but fast-growing segment of the health care sector has been afflicted with a number of ailments, sinking about 30% since July.

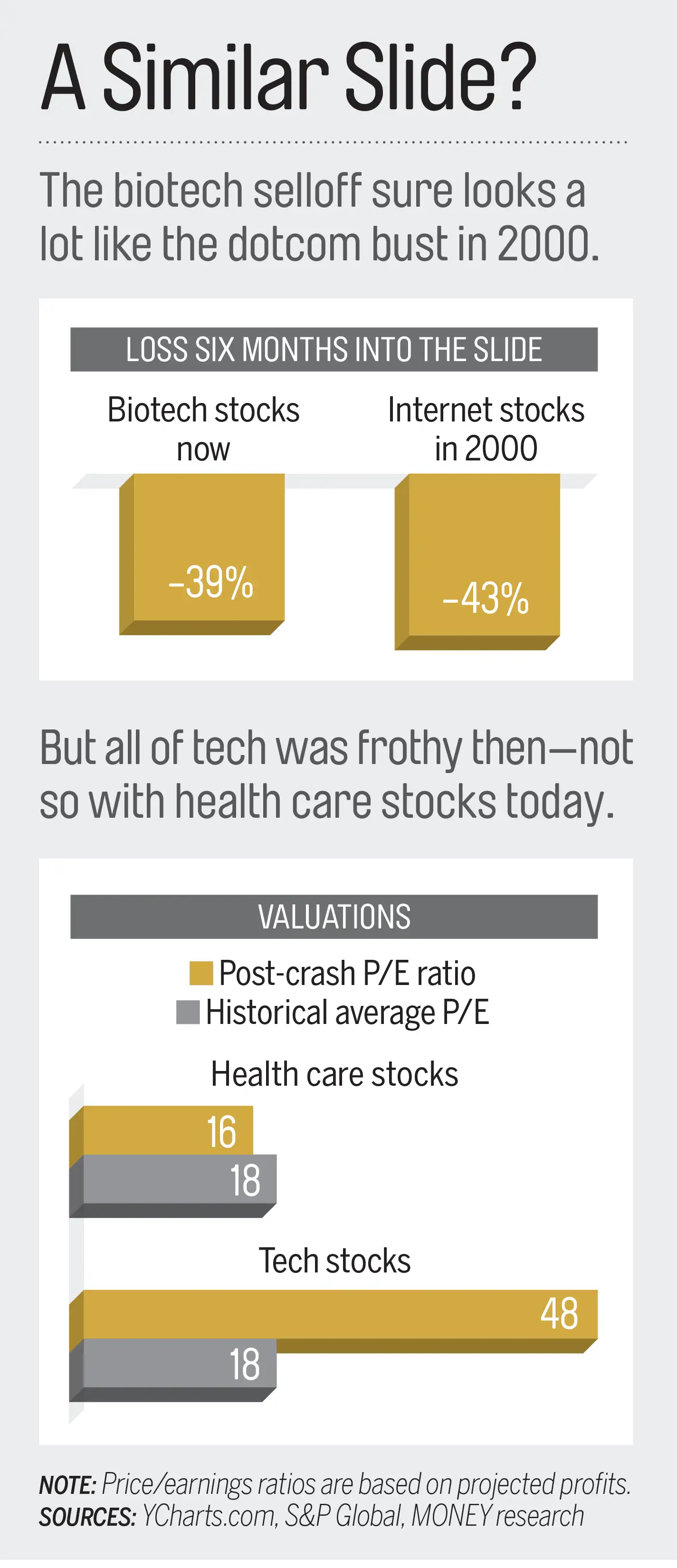

A sharp decline in a sexy part of the market that had skyrocketed to stratospheric levels. Sound familiar? Biotechs share several genetic markers with dotcom stocks from more than 15 years ago. Many biotech companies, which use biological materials to create drugs (pharmaceutical firms, by contrast, use plant and chemical compounds), have yet to turn a profit. Their shares have risen on the promise of treatments in development that could be blockbusters one day—or busts.

Moreover, this group was bid up to dizzying heights. Shares of small biotech companies were trading at a price/earnings ratio of over 300 last summer before the collapse. Even now the S&P 600 small biotech stock index sports a P/E of 32, based on projected profits.

Still, there are differences. In the late 1990s there were no "cheap" Internet stocks to be had. On the other hand "there are a lot of very profitable biotech companies and other health care segments that are trading at reasonable and sometimes low valuations," says Jeffrey Loo, director of health care equity research at S&P Global Market Intelligence.

The key to investing in the wake of this burst bubble, then, is knowing where those values are.

Broaden your horizons

In the dotcom era, euphoria for unproven startups seeped into nearly every nook and cranny of the whole tech sector. Valuations got so frothy that some tech giants such as Cisco Systems still aren't back to their inflated highs.

The biotech craze, by contrast, never infected the broader health care sector that has only modestly outpaced the S&P 500 since March 2009. Blue-chip health stocks trade at 16.1 times projected profits. Not only is that lower than the 17.9 P/E for the S&P 500, it's below the historical average (see chart).

Health care is attractive for another reason. In the long run, the aging population continues to be a demographic tailwind, says Brian Lazorishak, senior portfolio manager at Stack Financial Management. A bonus given this bull market's advanced age: When bear markets strike, big, profitable health care stocks have tended to fall half as much as the market.

Lazorishak recommends a diversified approach to health care, ranging from defensive drugmakers such as Johnson & Johnson to pharmaceutical distributors like AmerisourceBergen to medical suppliers such as Becton Dickinson that are positioned to benefit from growing health spending. Alternatively, you can go with Health Care Select Sector SPDR a low-cost ETF (expense ratio: 0.14%) that owns all three stocks.

Shop in the discount bin

Several years after the dotcom crash, tech went from the realm of speculators to bargain hunters. Biotechs—at least shares of the bigger, established companies that generate real products and profits—have already reached that point. "Large-cap biotechs are at the best valuation we've seen" since tracking the group in 1985, says Greg Swenson at Leuthold Weeden Capital Management.

Take Gilead Sciences . The company, which earned more than $18 billion last year, is suddenly getting a cool reception from gung ho growth investors. They worry that the explosive growth in Gilead's blockbuster HIV and hepatitis C drugs—which have been on the market for a few years—may be slowing. Gilead is also enmeshed in the recent public ire over sharply rising drug prices that has been the focus of congressional hearings.

Yet even if growth slows to a trickle, the shares trade at a mere eight times Gilead's expected 2016 earnings. And the stock pays a decent dividend yield of 1.8%.

Gilead and fellow giants Biogen and Amgen are in the Market Vectors Morningstar Wide Moat ETF . The fund owns only firms with competitive advantages trading at the widest discounts to their true value, according to Morningstar analysts.